Understanding the Broad Relationship Between the Rating Scales of S&P Global (China) Ratings and S&P Global Ratings

S&P Global (China) Ratings has unveiled a report detailing the relationship between its rating scales and those of S&P Global Ratings. This report aims to enhance transparency and improve understanding among market participants about rating differentiations. The analysis encompasses 143 Chinese corporates, revealing that the credit quality results from S&P Global (China) Ratings are more widely distributed compared to S&P Global Ratings, as it removes sovereign credit constraints. This comprehensive overview is crucial for investors navigating the Chinese market.

- S&P Global (China) Ratings' methodology is tailored for local application in China, providing greater granularity on ratings.

- The analysis of 143 Chinese corporates shows a broader distribution of credit quality compared to S&P Global Ratings.

- No one-to-one mapping exists between S&P Global (China) Ratings and S&P Global Ratings, which may confuse investors.

BEIJING, Feb. 1, 2021 /PRNewswire/ -- S&P Global (China) Ratings has observed great interest in our approach to ratings and our differentiated credit opinions. To help market participants better understand our rating differentiation and improve transparency, S&P Global (China) Ratings today published a report presenting an overview of the broad relationship between the rating scales of S&P Global (China) Ratings and S&P Global Ratings.

Despite the broad relationship between the two scales, they are different and there is no mapping between the two. The two scales have the same purpose: providing better credit differentiations and greater granularity on rating outcomes. Our desktop analysis of indicative credit quality, further details of which can be found below, shows the results of S&P Global (China) Ratings are more widely distributed, due to the removal of any sovereign credit rating related constraints which may be applicable in S&P Global Ratings' methodology.

S&P Global (China) Ratings' rating methodologies are broadly based on S&P Global Ratings' frameworks but have been modified and tailored for local application in China. To help investors better understand the broad relationship between the two scales, we conducted a desktop analysis of 143 Chinese corporates, applying S&P Global (China) Ratings' methodology to public information.

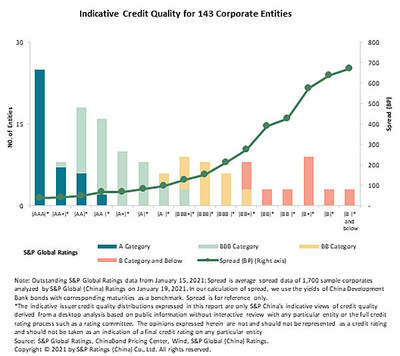

The chart below presents S&P Global (China) Ratings' view of the indicative credit quality distribution of the 143 corporates. This sample covers almost all corporate sectors, with the entities selected from a pool of more than 200 companies on which S&P Global Ratings has ratings outstanding. We chose to exclude certain entities from this desktop analysis, including Hong Kong-based subsidiaries of Chinese companies or offshore financing platforms which are less likely to be issuers in the domestic market. The chart also includes the spread of a wider pool of 1,700 corporates to show how this aligns with our view of differentiated credit quality.

From the chart we can observe a broad relationship between the two rating scales, with the indicative credit quality distribution by S&P Global China Ratings of the 143 corporates covering the entire spectrum from [AAAspc] to [Bspc-] and below. For companies rated in the A category by S&P Global Ratings, their indicative credit quality on S&P Global (China) Ratings' scale may fall somewhere between [AAAspc] and [AAspc-], across four different notches. Companies rated in the BBB category by S&P Global Ratings may have indicative credit quality ranging from [AAspc+] to [BBBspc+] on the S&P Global (China) Ratings' scale.

This broader distribution can be attributed to differences in core analytical approaches used in our respective corporate methodologies, sovereign credit quality constraints which may be applicable to the S&P Global credit ratings, as well as differences in analytical approaches associated with any group or government support uplift benefit potentially applicable to a given issuer.

In general, ratings on companies with stronger credit quality may vary more widely on the two scales, while any difference in ratings on entities with weaker credit quality is generally smaller. It should be emphasized that this is based on our observation and is not absolute, and there is no one-to-one mapping between the results of S&P Global (China) Ratings and S&P Global Ratings.

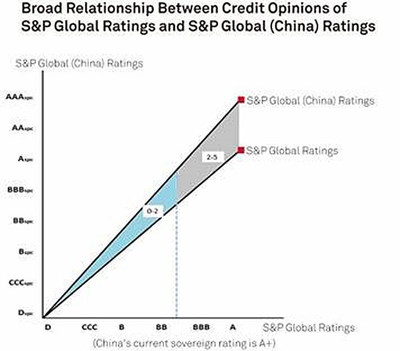

A look at how we approach RMB bonds issued by foreign institutions in China (Panda Bonds) offers another perspective on the relationship between the two scales. The S&P Global (China) Ratings Panda Bond rating methodology is a separate framework. Under this framework, for foreign issuers that conduct the majority of their business overseas, we usually refer to S&P Global Ratings' credit opinion on the entity and use this as a starting point to arrive at S&P Global (China) Ratings' rating determination.

Source: S&P Global (China) Ratings.

Copyright © 2021 by S&P Ratings (China) Co., Ltd. All rights reserved.

As the above chart shows, when S&P Global Ratings views a foreign issuer as having relatively lower credit quality (typically below BBB category), S&P Global (China) Ratings may assign a similar view of credit quality with adjustments typically of up to 2 notches. When S&P Global Ratings views a foreign issuer as having stronger credit quality, S&P Global (China) Ratings may assign a view of credit quality typically in a range of 2-5 notches higher than the credit quality opinion of S&P Global Ratings.

Under our Panda Bond rating methodology, the indicative credit quality of foreign issuers follows similar trends as that of domestic issuers under S&P Global (China) Ratings' other rating methodologies, with some correlation with the credit opinions of S&P Global Ratings. However, in both cases there is no one-to-one mapping relationship with S&P Global Ratings.

This report does not constitute a rating action.

(Note: This document is prepared in both English and Chinese. The English translation is for reference only, and the Chinese version will prevail in the event of any inconsistency between the English version and the Chinese version.)

S&P Global (China) Ratings is the first wholly foreign-owned Credit Rating Agency to provide independent credit ratings in the domestic Chinese market. Its ratings and insights are built on the principles and objectivity of S&P Global Ratings, the world's leading provider of credit ratings. We provide our opinions and research about relative credit risk; market participants gain independent information to help support the growth of transparent, liquid debt markets within China and around the world. For more information, visit www.spgchinaratings.cn.

Copyright © 2021 by S&P Ratings (China) Co., Ltd. All rights reserved.

S&P Ratings (China) Co., Ltd. ("S&P Ratings") owns the copyright and/or other related intellectual property rights of the abovementioned content (including ratings, credit-related analyses and data, valuations, model, software or other application or output therefrom) or any part thereof (Content). No Content may be modified, reverse engineered, reproduced or distributed in any form by any means, or stored in a database or retrieval system, without the prior written permission of S&P Ratings. The Content shall not be used for any unlawful or unauthorized purposes. S&P Ratings and any third-party providers, as well as their directors, officers, shareholders, employees or agents (collectively "S&P Parties") do not guarantee the accuracy, completeness, timeliness or availability of the Content. S&P Parties are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, for the results obtained from the use of the Content, or for the security or maintenance of any data input by the user. The Content is provided on an "as is" basis. S&P PARTIES DISCLAIM ANY AND ALL EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, ANY WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE, FREEDOM FROM BUGS, SOFTWARE ERRORS OR DEFECTS, THAT THE CONTENT'S FUNCTIONING WILL BE UNINTERRUPTED OR THAT THE CONTENT WILL OPERATE WITH ANY SOFTWARE OR HARDWARE CONFIGURATION. In no event shall S&P Parties be liable to any party for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including, without limitation, lost income or lost profits and opportunity costs or losses caused by negligence) in connection with any use of the Content even if advised of the possibility of such damages.

Credit-related and other analyses, including ratings, and statements in the Content are statements of opinion as of the date they are expressed and not statements of fact. S&P Ratings' opinions, analyses, forecasts and rating acknowledgment decisions (described below) are not and should not be viewed as recommendations to purchase, hold, or sell any securities or to make any investment decisions, and do not address the suitability of any security. S&P Ratings assumes no obligation to update the Content following publication in any form or format. The Content should not be relied on and is not a substitute for the skill, judgment and experience of the user, its management, employees, advisors and / or clients when making investment and other business decisions. S&P Ratings does not act as a fiduciary or an investment advisor except where registered as such. While S&P Ratings has obtained information from sources it believes to be reliable, S&P Ratings does not perform an audit and undertakes no duty of due diligence or independent verification of any information it receives. Rating-related publications may be published for a variety of reasons that are not necessarily dependent on action by rating committees, including, but not limited to, the publication of a periodic update on a credit rating and related analyses.

S&P RATINGS IS NOT PART OF THE NRSRO. A RATING ISSUED BY S&P RATINGS IS ASSIGNED ON A RATING SCALE SPECIFICALLY FOR USE IN CHINA, AND IS S&P RATINGS' OPINION OF AN OBLIGOR'S OVERALL CREDITWORTHINESS OR CAPACITY TO MEET SPECIFIC FINANCIAL OBLIGATIONS, RELATIVE TO THAT OF OTHER ISSUERS AND ISSUSES WITHIN CHINA ONLY AND PROVIDES A RANK ORDERING OF CREDIT RISK WITHIN CHINA. AN S&P RATINGS' RATING IS NOT A GLOBAL SCALE RATING, AND IS NOT AND SHOULD NOT BE VIEWED, RELIED UPON, OR REPRESENTED AS SUCH. S&P PARTIES ARE NOT RESPONSIBLE FOR ANY LOSSES CAUSED BY USES OF S&P RATINGS' RATINGS IN MANNERS CONTRARY TO THIS PARAGRAPH.

To the extent that regulatory authorities allow a rating agency to acknowledge in one jurisdiction a rating issued in another jurisdiction for certain regulatory purposes, S&P Ratings reserves the right to assign, withdraw or suspend such acknowledgement at any time and in its sole discretion. S&P Ratings disclaims any duty whatsoever arising out of the assignment, withdrawal or suspension of an acknowledgment as well as any liability for any damage alleged to have been suffered on account thereof.

S&P Ratings keeps certain activities of its business units separate from each other in order to preserve the independence and objectivity of their respective activities. As a result, certain business units of S&P Ratings may have information that is not available to other S&P Ratings business units. S&P Ratings has established policies and procedures to maintain the confidentiality of certain non-public information received in connection with each analytical process.

S&P Ratings may receive compensation for its ratings and certain analyses, normally from issuers or underwriters of securities or from obligors. S&P Ratings reserves the right to disseminate its opinions and analyses. S&P Ratings' public ratings and analyses are made available on its Web site www.spgchinaratings.cn, and may be distributed through other means, including via S&P Ratings' publications and third-party redistributors.

![]() View original content to download multimedia:http://www.prnewswire.com/news-releases/understanding-the-broad-relationship-between-the-rating-scales-of-sp-global-china-ratings-and-sp-global-ratings-301219320.html

View original content to download multimedia:http://www.prnewswire.com/news-releases/understanding-the-broad-relationship-between-the-rating-scales-of-sp-global-china-ratings-and-sp-global-ratings-301219320.html

SOURCE S&P Global Ratings

FAQ

What does the recent report from S&P Global (China) Ratings reveal about credit ratings?

How many corporates were analyzed in the S&P Global (China) Ratings report?

What is the significance of S&P Global (China) Ratings' approach to local application?

How does the credit quality distribution in S&P Global (China) Ratings compare to S&P Global Ratings?