S&P Global Platts Analytics Releases its 2021 Energy Outlook

On December 14, 2020, S&P Global Platts released its 2021 energy outlook, projecting a recovery in global GDP and oil demand. Despite optimism from vaccine developments, short-term challenges persist due to renewed lockdowns in the US and Europe, which will suppress gasoline demand. Oil demand is expected to rebound by over 6 million barrels per day, yet remain below 2019 levels. Key highlights include OPEC+'s influence on oil supply, refining challenges, and the potential for volatility in petrochemicals and natural gas markets. Renewables are anticipated to grow, putting further pressure on fossil fuel demand.

- Oil demand projected to rebound over 6 million barrels per day in 2021.

- Increase in renewable energy capacity expected, contributing to long-term sustainability.

- Short-term oil demand likely to remain over 2 million barrels per day below 2019 levels due to COVID-19 impacts.

- Refinery margins under pressure, leading to potential closures.

- Political risks affecting OPEC+ supply management may lead to market volatility.

NEW YORK, Dec. 14, 2020 /PRNewswire/ -- Analysts at S&P Global Platts, the leading independent provider of information, analysis and benchmark prices for the commodities and energy markets, today released their 2021 energy outlook. The outlook presumes a recovery in global gross domestic product (GDP), highlighted by an acceleration of growth in the second half of 2021.

Chris Midgley, Global Head of Analytics, S&P Global Platts, said: "The positive news over the emergence of an effective Covid-19 vaccine has created a wave of optimism across commodity markets despite the fundamentals extensively being unchanged. While in the long-term we are more optimistic about a rebound of oil demand, causing us to upwardly revise our 2021 demand outlook, in the short term, we expect things to worsen, with increased second-wave lockdowns in US and Europe resulting in much weaker gasoline demand across the holiday season."

HIGHLIGHTS OF THE 2021 FORECASTS OF S&P GLOBAL PLATTS ANALYTICS:

OIL

- COVID-19 & bumpy ride for oil demand: Oil demand will rebound by more than 6 million barrels per day (b/d) in 2021, but consumption is still expected to be more than 2 million b/d below that of 2019's 101.9 million b/d. Why? The global middle class - the real engine of oil demand - faces continued pressures from wealth inequality and the ongoing COVID-19 cloud. Widespread vaccine deployment is unlikely to occur until H2 2021, which won't prevent periodic lockdowns for several months. Complicating matters is the reality that initial distribution of any vaccine will skew toward the elderly and frontline workers – important groups to be sure – but not ones that will drive the recovery in oil demand. Jet Fuel: Due to the sharp reduction in air travel, kerosene/jet fuel demand represented more than a third of the overall demand decline in 2020, falling by 3.1 million b/d. Jet fuel will remain the laggard going forward, keeping distillate supply more in surplus through the first half and refineries operating more in gasoline-production mode.

- OPEC+ will be the dominant factor for 2021 oil supply: Political risk: Libyan supply will continue to defy expectations, rising to 1.2 million barrels per day (b/d), subject to the tenuous ceasefire. With a new US Administration, supply upside could come from Iran and Venezuela, though progress promises to be slow. Policy/cohesion: It will be increasingly difficult for OPEC+ to walk the tightrope between volume and price, with the organization looking to both increase revenues and prevent a sizeable rebound in US market share. Shale impact: US oil production is set to decline another one-million b/d in 2021 on a year-over-year basis due to steep declines in the shale base, with slow pick up in rigs/frack crews.

- Oil prices: Overall, fundamentals will resume the ascendancy over sentiment, which should see Dated Brent oil prices soften in the short-term to the low

$40 s-per-barrel area, but should prompt a price move toward$50 per barrel by the end of 2021, with WTI to recover to just under$50 /b. However, caution is warranted, given the uncertainties regarding robust OPEC spare capacity and Covid-19 vaccine deployment.

REFINING AND NGLS

- Squeezed refiners need a demand outlet or face closure: Even assuming a rebound in refined product demand in 2021, growth in refining capacity, largely in the Middle East and Asia, will be far larger. A continued influx of biofuels and NGLs supply will continue to weigh on crude run rates in 2021. This will squeeze margins of existing refineries, particularly if demand recovery for transportation fuels remains sluggish. Refinery closures are inevitable. Refineries well placed to survive will have a focus on costs, local markets, and integration with petrochemicals or transformation into bio-refineries.

PETROCHEMICALS

- Petrochemicals feedstock volatility to surge as plastics take the lead: As the only sector with positive oil demand growth in 2020, the petrochemical sector's growth will accelerate in 2021 by

4% , driven by a recovery in durable goods (propylene derived products) and further growth in demand for packaging (ethylene derivative products). The relative strength in petrochemicals demand compared to the weakness in gasoline demand will cause regional competition and volatility in feedstocks, specifically ethane and naphtha. In general, petrochemicals producers have painted themselves into a corner - with high inventories in Asia, just as a massive build-out of capacity occurs. Polyethylene terephthalate (PET) bottle demand growth will be satisfied by higher recycled content as beverage companies triple the global recycled content toward25% over the next few years.

GAS-TO-COAL SWITCHING

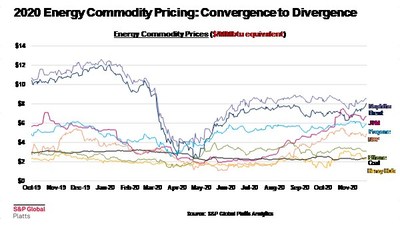

- Gas-to-coal switching may not be enough to prevent Henry Hub (HH) prices from hitting seven-year highs and LNG shut-ins. For natural gas, we see mixed fortunes ahead, with HH in the US set to recover all of its losses to test

$3 /MMBtu. In Europe, TTF and Platts JKM, the benchmark LNG delivered into North Asia, will both see fundamentals weaken. The US natural gas supply faces a loss of associated gas production from weaker shale oil drilling and higher ethane recovery in 2021. To ensure adequate natural gas storage for 2021/2022, it will be necessary on the demand side to see gas-to-coal switching and continued growth in renewables generation. On the supply side, the responsiveness of higher-cost dry gas production will be key to how high prices go, and how much US LNG will be shut in. - 2021 may be coal's "last hurrah" of demand: Gas-to-coal switching and recovering power demand in the US will increase the call on coal supply in 2021, but financially distressed US coal producers will find it challenging to adequately ramp up supply. Despite an expected recovery in consumption, China's imports may decline again in 2021, as the world's largest coal producer and consumer strives for self-sufficiency. Demand growth in the rest of the world may not be enough to compensate for the loss in Chinese import demand.

LIQUEFIED NATURAL GAS (LNG)

- New (super-chilled) cold war between US and Russia LNG/gas in Europe: The delayed completion of the Nord Stream 2 pipeline in 2Q 2021 will join the recently-completed Trans Adriatic Pipeline (TAP) and rebounding Algerian gas flows as incremental gas supply flowing into Europe. With too much supply chasing too little European demand amid record high storage, US LNG exporters could be on the outside looking in during 2021.

- Asian LNG buyers remain in the driver's seat despite demand surge: Asian LNG demand will rebound sharply in 2021, but weak European LNG demand, a

3.5% expansion of global new liquefaction capacity, and low oil-linked LNG contracts, will keep buyers flush with options for supply over the next year. Expect demand and price seasonality to intensify in 2021, with both winter tightness and summer cargo cancellations occurring over the year. The Platts JKM forward curve is showing strong backwardation, implying the market views the current tightness as short-lived. Prices are expected to trend lower moving into first quarter 2021, particularly if the Asia-Pacific region experiences another mild winter. Assuming no further large supply disruptions, Platts JKM in Q1-21 should outturn below$6.75 /MMBtu and average just over$4 /MMBtu during summer 2021.

RENEWABLES, ENERGY TRANSITION

- Renewables, nuclear, and renewable fuel growth to accelerate and further challenge fossil fuels: New wind and solar capacity build will increase in 2021, driven by a host of grid-parity solar projects in China, a rebound in Indian installations, and deferred US installations from 2020 into 2021. We have upgraded our global solar PV additions forecast for 2020 by some

7% or about 8 gigawatts, while keeping 2021 capacity additions forecasts unchanged. Coupled with a recovery in nuclear generation, growth in renewable electricity supply will weight on the recovery of fossil fuel demand in the power sector. Biofuels demand will grow faster than fossil fuels next year, driven by a higher blending rate and a ramp-up in renewable diesel capacity. - Can environmental policies shift from rhetoric to action? Perhaps the biggest impact of the US election on energy markets could be a change of course on US environmental policy. However, with control of the US Senate to be undecided until January, it is unclear how much ability the incoming Biden administration will have to change policy. Recent pledges to hold emissions growth to net zero by China (2060) and Japan and South Korea (2050) and Europe's greater climate-control ambitions were headline grabbers in 2020. However, they are not all yet enshrined into law and announced pathways to achieving those ambitious goals are nebulous at best. The climate-favorable news: several of the world's largest economies now have some form of net-zero target and greater global ambition could emerge at the UN Climate Change Conference (COP26) in November 2021. Despite this greater focus on long-term carbon reductions, the economic recovery, gas-to-coal switching, and low fossil fuels prices will drive energy sector CO2 emissions 1.4 gigatons (

4.4% ) higher year on year in 2021.

AGRICULTURE

- Market drivers for grains: Uncertainty over continuing Chinese purchases of corn, soybeans and wheat, along with the impacts of a La Nina on already dry areas globally, will be market drivers in early 2021. With a new administration, expected to be more trade-friendly, to take office in the United States, exporters are hoping to gain a larger markets share of Chinese import demand in all three major grains and oilseeds.

Dan Klein, Head of Energy Pathways, Analytics, S&P Global Platts, said: "2020 was a year that proves that there is no such thing as 20/20 vision when it comes to forecasting energy markets and pricing. There will undoubtedly be unforeseeable twists and turns over 2021 that will bring rise to even more risks to the forecasts. But fundamentals will continue to matter more than they ever have, requiring a steady, holistic perspective across the breadth of the energy market."

Media Contacts:

Americas: Kathleen Tanzy, + 1 917-331-4607, kathleen.tanzy@spglobal.com

About S&P Global Platts

At S&P Global Platts, we provide the insights; you make better informed trading and business decisions with confidence. We're the leading independent provider of information and benchmark prices for the commodities and energy markets. Customers in over 150 countries look to our expertise in news, pricing and analytics to deliver greater transparency and efficiency to markets. S&P Global Platts coverage includes oil and gas, power, petrochemicals, metals, agriculture and shipping.

S&P Global Platts is a division of S&P Global (NYSE: SPGI), which provides essential intelligence for companies, governments and individuals to make decisions with confidence. For more information, visit http://spglobal.com/platts.

![]() View original content to download multimedia:http://www.prnewswire.com/news-releases/sp-global-platts-analytics-releases-its-2021-energy-outlook-301192052.html

View original content to download multimedia:http://www.prnewswire.com/news-releases/sp-global-platts-analytics-releases-its-2021-energy-outlook-301192052.html

SOURCE S&P Global Platts

FAQ

What is the oil demand forecast for 2021 according to SPGI?

How will COVID-19 affect oil demand in the short term for SPGI?

What key factors will influence oil supply in 2021 for SPGI?

What are the challenges faced by refiners in 2021 according to SPGI?