Primerica Releases Inaugural Household Budget Index™ (HBI™) to Illustrate Purchasing Power of Middle-Income Families

Rhea-AI Impact

(Low)

Rhea-AI Sentiment

(Very Positive)

Tags

Rhea-AI Summary

Middle-income households experienced increased spending power but are still recovering from high inflation in the past 18 months.

Positive

Middle-income households had a peak purchasing power of 102.8% in November 2020 compared to January 2019.

The Primerica HBI™ rose slightly to 97.5% in July 2023 from 97.0% in June 2023.

Negative

Middle-income households have cumulatively spent around $3,150 more than budget on basic necessities since January 2019.

Rising credit card debt is currently observed due to the impact of the last 18 months of inflation.

Insights

Analyzing...

New monthly index shows middle-income families are seeing increased spending power, yet still recovering from previous 18-months of high inflation

DULUTH, Ga.--(BUSINESS WIRE)--

Primerica, Inc. (NYSE: PRI), a leading provider of financial services in the United States and Canada, announced today the release of its inaugural Primerica Household Budget Index™ (HBI™), a monthly index illustrating the purchasing power of middle-income households with incomes between $30,000 and $130,000. The HBI™ looks at the difference between the growth in earned income and the change in the costs for necessities like food, utilities, health care, and gasoline to understand how the current economy is impacting middle-income households’ ability to maintain a budget. It also evaluates whether there are opportunities for middle-income families to save money or pay down debt versus use savings or increase debt.

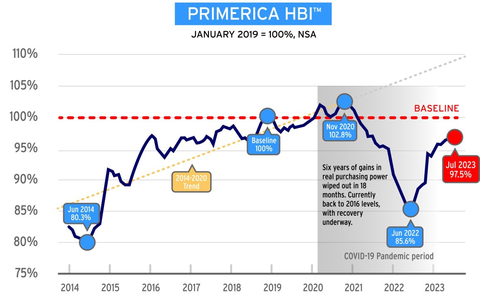

Chart 1: Primerica HBI™ (Graphic: Business Wire)

The HBI™ data is presented as a percentage. When the index is above 100%, this means middle-income households may have extra money left over at the end of the month that can be applied to things like entertainment, extra savings, or debt reduction. If it is under 100%, households may have to reduce overall spending to levels below budget, reduce their savings, or increase debt to cover expenses. The index uses January 2019 as its baseline. This point in time reflects a recent “normal” economic time prior to the COVID-19 pandemic.

Between 2014 and 2020, the HBI™ results recorded steady gains in purchasing power for middle-income families, with a peak of 102.8% in November 2020. This means that compared to January 2019, households were in a stronger financial position to pay their monthly bills because wage growth outpaced the cost of everyday goods. Increasing inflation then caused the index to plummet. In June 2022, it reached a low of 85.6%.

In July 2023, the index rose slightly to 97.5% from 97.0% in June 2023. See “Chart 1: Primerica HBI™.”

“Understanding the purchasing power of middle-income households from month-to-month will make our guidance even more precise as we serve the financial needs of middle-income families,” said Glenn J. Williams, CEO of Primerica. “The principles we teach, coupled with this ongoing research, will help families in their efforts to achieve financial security.”

“The July index illustrates how deeply middle-income households were affected by the recent period of high inflation in which their income gains fell behind the rising cost of living expenses,” said Amy Crews Cutts, Ph.D., CBE®, economic consultant to Primerica.

Since the baseline of January 2019, the average middle-income household has cumulatively spent around $3,150 more than budget on basic necessities. In line with this, if the pandemic and ensuing inflation would not have been a factor, the HBI™ today would be closer to 110%. See “Chart 2: Inflation versus Growth in Earned Income for Middle-Income Households.”

“Middle-income households finally are pulling ahead, but the last 18-months of inflation has caused many to fall behind which accounts for the rising credit card debt we are currently seeing,” said Cutts.

There is not currently a consistent measure to track middle-income households’ purchasing power. While the Consumer Price Index (CPI) provides a comprehensive measure of inflation, it does not offer a clear picture of how the change in prices of necessities impacts middle-income households because it is weighted to include all income levels and aggregates expenses for rarely purchased items, as well as expenses for which households can plan. See “Chart 3: Comparison of Measures of Inflation: Consumer Price Index versus HBI-weighted CPI for Middle-Income Households.”

The HBI™ removes infrequently purchased or predictable expense items and focuses solely on the purchasing patterns of middle-income households, defined as those with incomes of $30,000-$130,000.

About the Primerica Household Budget Index™ (HBI™)

The Primerica Household Budget Index™ (HBI™) is constructed monthly on behalf of Primerica by its chief economic consultant Amy Crews Cutts, PhD, CBE®. The index measures the purchasing power of middle-income families with household incomes from $30,000 to $130,000 and is developed using data from the U.S. Bureau of Labor and the Federal Reserve. The index looks at the cost of necessities including food, gas, utilities and health care and earned income to track differences in inflation and wage growth.

The HBI™ is presented as a percentage. If the index above 100%, the purchasing power of middle-income families is stronger and may have extra money left over at the end of the month that can be applied to things like entertainment, extra savings, or debt reduction. If it is under 100%, households may have to reduce overall spending to levels below budget, reduce their savings or increase debt to cover expenses. The HBI™ uses January 2019 as its baseline. This point in time reflects a recent “normal” economic time prior to the COVID-19 pandemic.

About Primerica, Inc.

Primerica, Inc., is a leading provider of financial services to middle-income households in North America. Independent licensed representatives educate Primerica clients about how to better prepare for a more secure financial future by assessing their needs and providing appropriate solutions through term life insurance, which we underwrite, and mutual funds, annuities and other financial products, which we distribute primarily on behalf of third parties. We insured over 5.7 million lives and had over 2.8 million client investment accounts on December 31, 2022. Primerica, through its insurance company subsidiaries, was the #3 issuer of Term Life insurance coverage in the United States and Canada in 2022. Primerica stock is included in the S&P MidCap 400 and the Russell 1000 stock indices and is traded on The New York Stock Exchange under the symbol “PRI.”

An email has been sent to your address with instructions for changing your password.

There is no user registered with this email.

Sign Up

To create a free account, please fill out the form below.

Thank you for signing up!

A confirmation email has been sent to your email address. Please check your email and follow the instructions in the message to complete the registration process. If you do not receive the email, please check your spam folder or contact us for assistance.

Welcome to our platform!

Oops!

Something went wrong while trying to create your new account. Please try again and if the problem persist, Email Us to receive support.