Oak View Bankshares, Inc. Announces 2024 Earnings and Annual Dividend

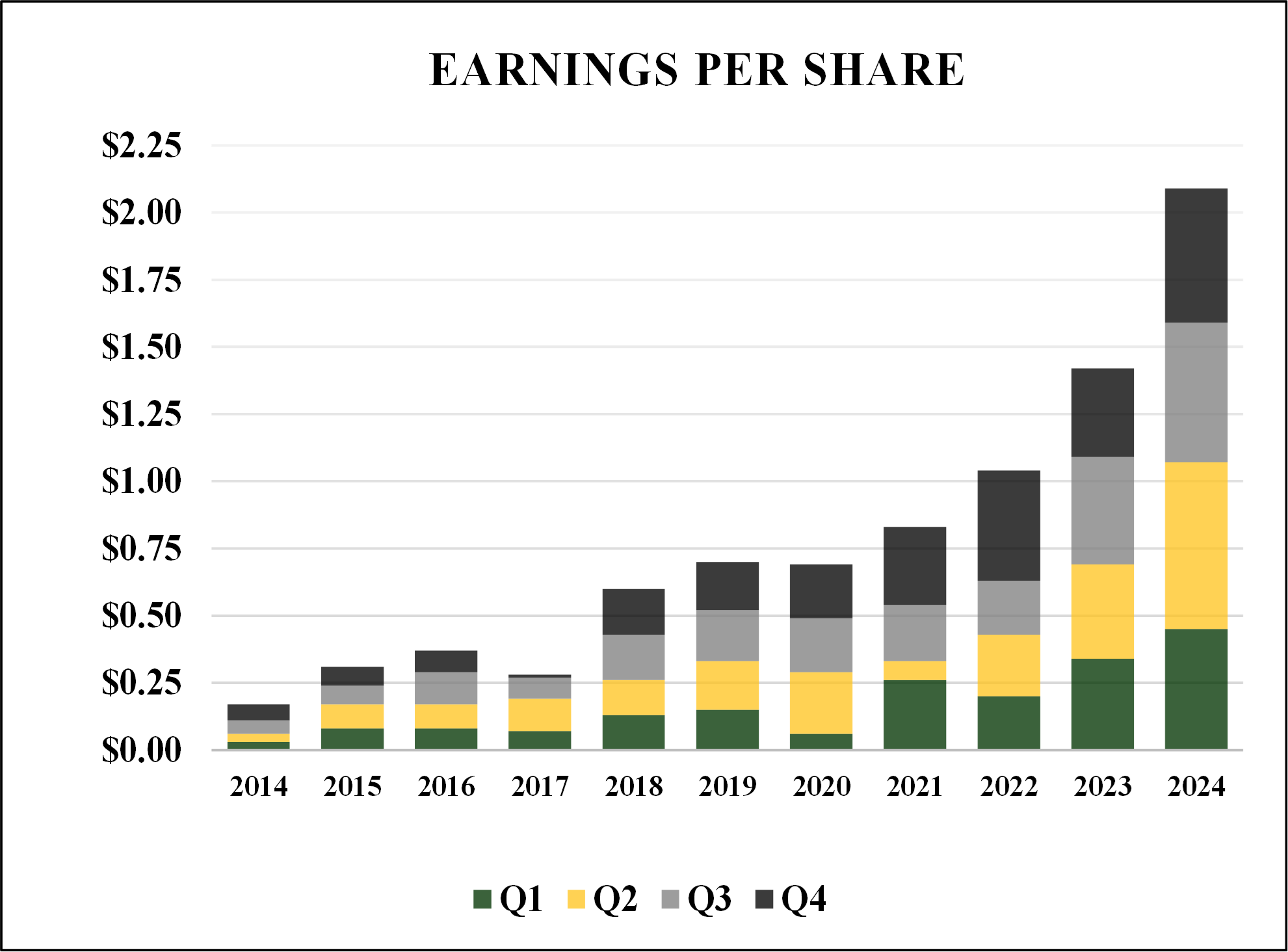

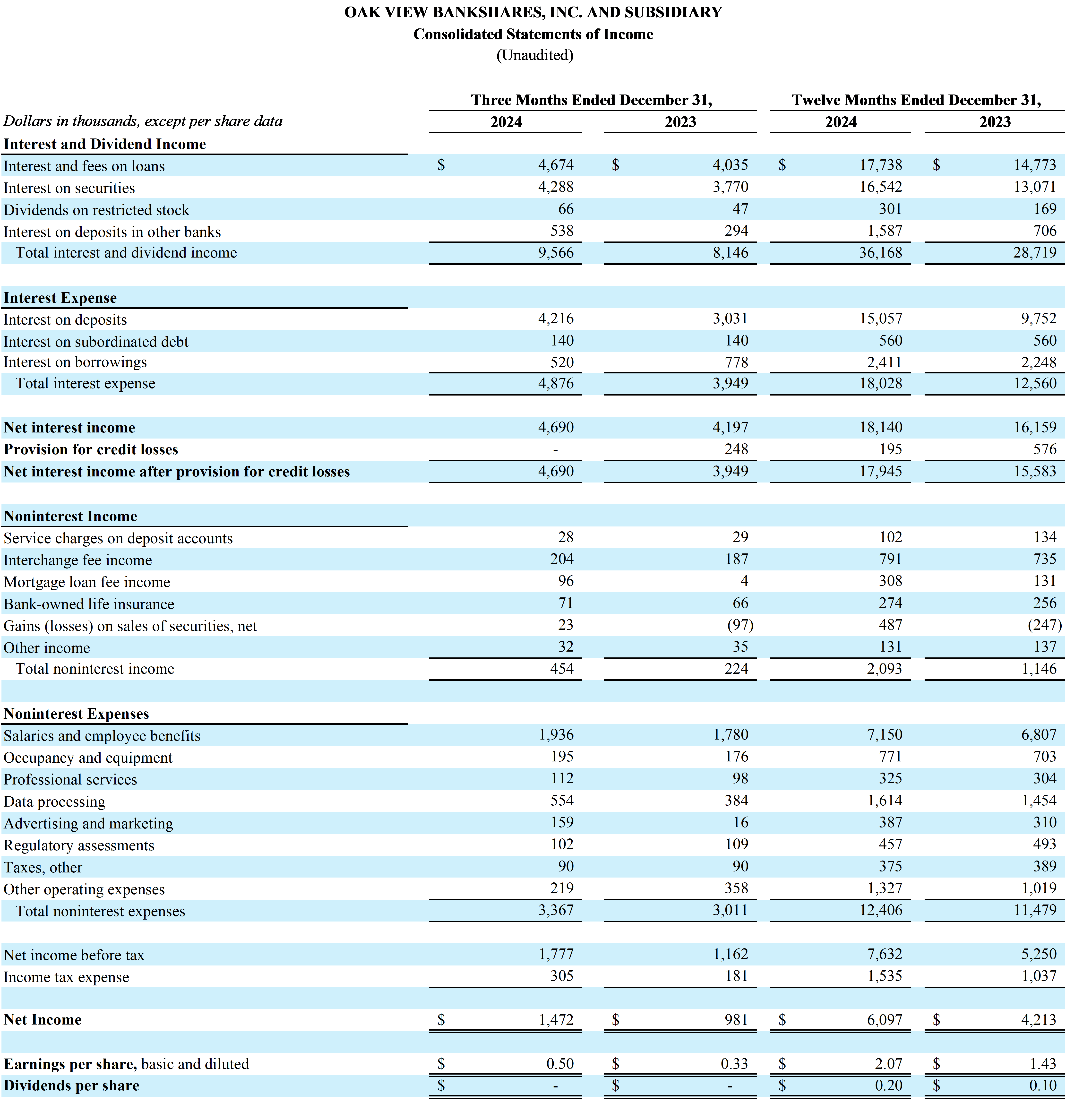

Oak View Bankshares (OAKV) reported strong financial results for 2024, with net income reaching $6.10 million, a 44.72% increase from $4.21 million in 2023. The company's earnings per share grew to $2.07 from $1.43 year-over-year. The Board declared an annual dividend of $0.27 per share, payable on February 6, 2025.

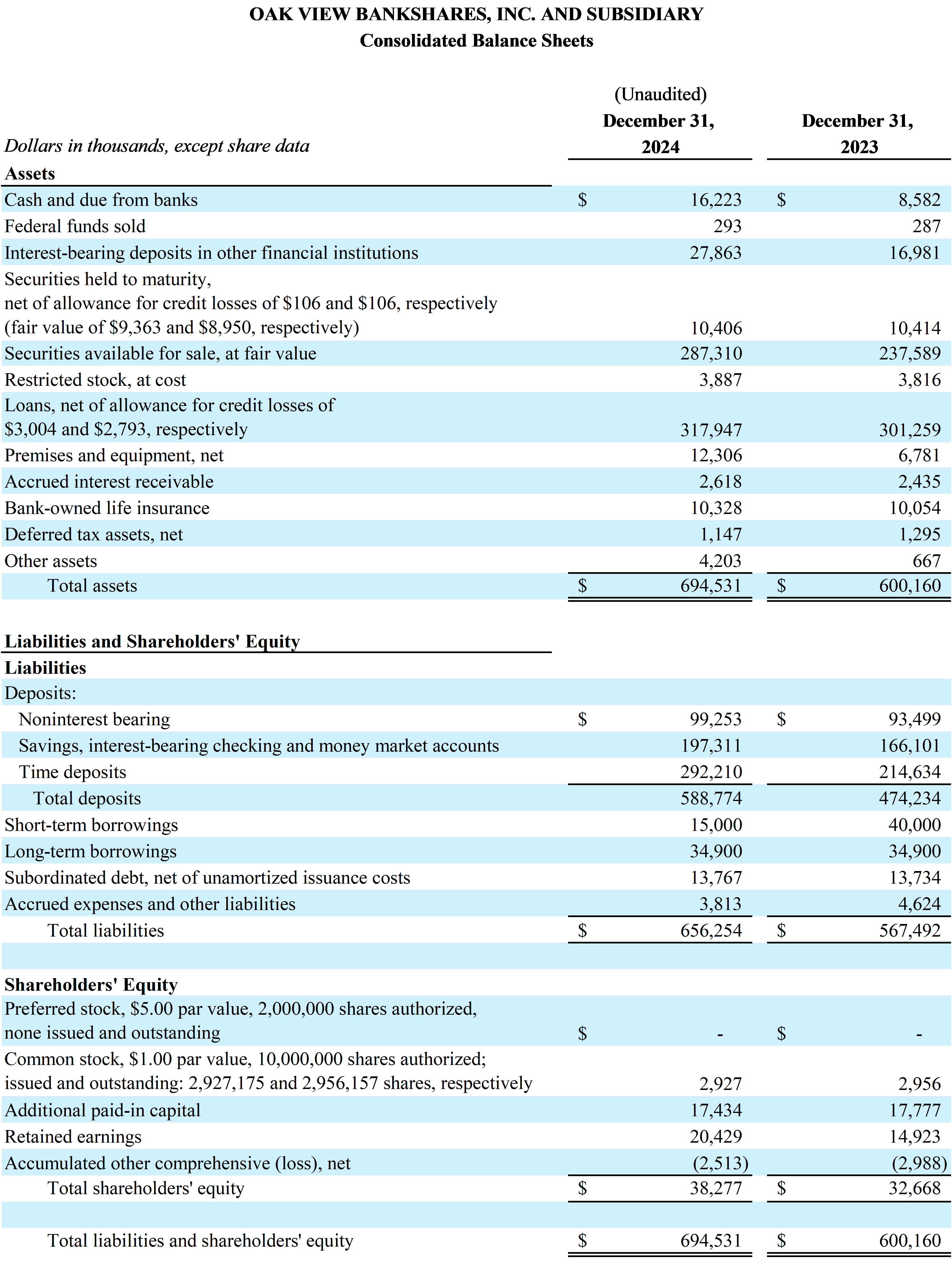

Key performance metrics showed significant improvement, with return on average assets at 0.94% and return on average equity at 17.45%. Total assets increased to $694.53 million, up from $600.16 million in 2023. The bank maintained strong asset quality with minimal charged-off loans and robust regulatory capital ratios, including a total capital ratio of 16.56%. Total deposits grew to $588.77 million, while maintaining a healthy liquidity position of $505.31 million in available liquid assets.

Oak View Bankshares (OAKV) ha riportato risultati finanziari solidi per il 2024, con un reddito netto che ha raggiunto 6,10 milioni di dollari, un aumento del 44,72% rispetto ai 4,21 milioni di dollari del 2023. Gli utili per azione dell’azienda sono cresciuti a 2,07 dollari rispetto all’1,43 dollari dell’anno precedente. Il Consiglio ha dichiarato un dividendo annuale di 0,27 dollari per azione, pagabile il 6 febbraio 2025.

I principali indicatori di performance hanno mostrato un miglioramento significativo, con un ritorno medio sugli attivi pari allo 0,94% e un ritorno medio sul capitale proprio del 17,45%. Gli attivi totali sono aumentati a 694,53 milioni di dollari, rispetto ai 600,16 milioni di dollari del 2023. La banca ha mantenuto una qualità degli attivi solida con prestiti in sofferenza minimi e robuste ratio di capitale regolamentari, compresa una ratio di capitale totale del 16,56%. I depositi totali sono cresciuti a 588,77 milioni di dollari, mantenendo una posizione di liquidità sana di 505,31 milioni di dollari in attivi liquidi disponibili.

Oak View Bankshares (OAKV) informó resultados financieros sólidos para 2024, con un ingreso neto que alcanzó 6.10 millones de dólares, un aumento del 44.72% respecto a 4.21 millones de dólares en 2023. Las ganancias por acción de la empresa crecieron a 2.07 dólares desde 1.43 dólares en comparación con el año anterior. La Junta declaró un dividendo anual de 0.27 dólares por acción, pagadero el 6 de febrero de 2025.

Los principales indicadores de rendimiento mostraron una mejora significativa, con un retorno sobre activos promedio del 0.94% y un retorno sobre capital promedio del 17.45%. Los activos totales aumentaron a 694.53 millones de dólares, frente a los 600.16 millones de dólares de 2023. El banco mantuvo una sólida calidad de activos con préstamos incobrables mínimos y robustas ratios de capital regulatorio, incluida una ratio de capital total del 16.56%. Los depósitos totales crecieron a 588.77 millones de dólares, al tiempo que mantuvieron una posición de liquidez saludable de 505.31 millones de dólares en activos líquidos disponibles.

Oak View Bankshares (OAKV)는 2024년 강력한 재무 성과를 보고했으며, 순이익은 610만 달러에 달해 2023년의 421만 달러보다 44.72% 증가했습니다. 회사의 주당순이익(EPS)은 전년 대비 2.07달러로 증가했습니다. 이사회는 주당 0.27달러의 연배당금을 선언했으며, 이는 2025년 2월 6일에 지급될 예정입니다.

주요 성과 지표는 상당한 개선을 보여주었으며, 평균자산수익률은 0.94%, 자기자본이익률은 17.45%에 달했습니다. 총 자산은 6억 9천 453만 달러로 2023년의 6억 16만 달러에서 증가했습니다. 은행은 최소한의 대손상각 대출과 강력한 규제 자본 비율을 유지하며 자산 품질을 유지했습니다. 총 자본 비율은 16.56%입니다. 총 예금은 5억 8천 877만 달러로 증가했으며, 가용 유동 자산으로 5억 5천 31만 달러의 건전한 유동성 위치를 유지하고 있습니다.

Oak View Bankshares (OAKV) a annoncé des résultats financiers solides pour 2024, avec un revenu net atteignant 6,10 millions de dollars, soit une augmentation de 44,72 % par rapport à 4,21 millions de dollars en 2023. Les bénéfices par action de l’entreprise ont augmenté à 2,07 dollars contre 1,43 dollar l'année précédente. Le Conseil a déclaré un dividende annuel de 0,27 dollar par action, payable le 6 février 2025.

Les principaux indicateurs de performance ont montré une amélioration significative, avec un retour sur actifs moyen de 0,94 % et un retour sur capitaux propres moyen de 17,45 %. Les actifs totaux ont augmenté à 694,53 millions de dollars, contre 600,16 millions de dollars en 2023. La banque a maintenu une qualité d’actifs solide avec des prêts à risque minimaux et des ratios de capital réglementaire robustes, y compris un ratio de capital total de 16,56 %. Les dépôts totaux ont atteint 588,77 millions de dollars, tout en maintenant une position de liquidité saine de 505,31 millions de dollars d’actifs liquides disponibles.

Oak View Bankshares (OAKV) meldete für 2024 starke finanzielle Ergebnisse, mit einem Nettogewinn von 6,10 Millionen Dollar, einem Anstieg um 44,72% im Vergleich zu 4,21 Millionen Dollar im Jahr 2023. Der Gewinn pro Aktie des Unternehmens stieg von 1,43 Dollar auf 2,07 Dollar im Jahresvergleich. Der Vorstand erklärte eine jährliche Dividende von 0,27 Dollar pro Aktie, die am 6. Februar 2025 zahlbar ist.

Wichtige Leistungskennzahlen zeigten erhebliche Verbesserungen, wobei die durchschnittliche Vermögensrendite bei 0,94% und die durchschnittliche Eigenkapitalrendite bei 17,45% lag. Die Gesamtaktiva stiegen auf 694,53 Millionen Dollar, gegenüber 600,16 Millionen Dollar im Jahr 2023. Die Bank hielt eine starke Vermögensqualität aufrecht, mit minimalen abgeschriebenen Darlehen und robusten regulatorischen Kapitalquoten, einschließlich einer Gesamt- Kapitalquote von 16,56%. Die Gesamteinlagen wuchsen auf 588,77 Millionen Dollar, während eine gesunde Liquiditätsposition von 505,31 Millionen Dollar an verfügbaren liquiden Mitteln aufrechterhalten wurde.

- Net income increased 44.72% to $6.10 million

- EPS grew 44.75% to $2.07

- Total assets increased by $94.28 million to $694.53 million

- Total deposits grew by $114.54 million to $588.77 million

- Strong asset quality with only 0.004% net charged-off loans

- Robust capital ratios with total capital ratio at 16.56%

- Noninterest income increased 82.64% to $2.09 million

- Net interest margin declined to 2.90% from 2.96% YoY

- Cost of funds increased to 2.97% from 2.38% YoY

- Noninterest expenses increased 8.08% to $12.41 million

WARRENTON, VA / ACCESS Newswire / January 21, 2025 / Oak View Bankshares, Inc. (the "Company") (OTC PINK:OAKV), parent company of Oak View National Bank (the "Bank"), reported net income of

Basic and diluted earnings per share for the year ended December 31, 2024, were

On January 16, 2025, the Board of Directors of the Company declared an annual dividend of

"Despite industry headwinds and persistent market volatility, our exceptional team delivered

Selected Highlights:

Return on average assets was

0.94% and return on average equity was17.45% for the year ended December 31, 2024, compared to0.75% and14.38% , respectively, for the year ended December 31, 2023.Total assets were

$694.53 million on December 31, 2024, compared to$600.16 million on December 31, 2023, an increase of$94.28 million .Total loans were

$320.95 million on December 31, 2024, compared to$304.05 million on December 31, 2023, an increase of$16.90 million . Much of this increase was within the commercial owner-occupied real estate portfolio.The total amortized cost of debt securities was

$297.82 million on December 31, 2024, compared to$248.11 million on December 31, 2023, an increase of$49.71 million .Total deposits were

$588.77 million on December 31, 2024, compared to$474.23 million on December 31, 2023, an increase of$114.54 million . Brokered deposits, all with call options, represent the majority of this growth, while interest bearing demand, money market and time deposits also contributed to the increases within the deposit portfolio.Regulatory capital remains strong with the Bank's ratios exceeding the "well capitalized" thresholds in all categories, with total capital ratio at

16.56% , common equity tier 1 capital ratio at15.63% , tier 1 capital ratio at15.63% and leverage ratio at7.87% .Asset quality continues to be outstanding. Net charged-off loans were

0.004% of total loans, there were no nonaccrual loans, accruing loans past due 30-89 days were0.015% of total loans, and one accruing loan past due 90 days or more was0.005% of total loans.Liquidity remains strong with cash, unencumbered securities available for sale, and available secured and unsecured borrowing capacity totaling

$505.31 million as of December 31, 2024, compared to$453.94 million as of December 31, 2023.

Net Interest Income

The net interest margin was

Noninterest Income

Noninterest income was

Noninterest Expense

Noninterest expenses were

Liquidity

Liquidity remains exceptionally strong with

The Company's deposits proved to be stable with core deposits, which are defined as total deposits excluding brokered deposits, of

Asset Quality

The allowance for credit losses related to the loan portfolio was

Net charged-off loans were

Shareholders' Equity and Regulatory Capital

Shareholders' equity was

About Oak View Bankshares, Inc. and Oak View National Bank

Oak View Bankshares, Inc. is the parent bank holding company for Oak View National Bank, a locally owned and managed community bank serving Fauquier, Culpeper, Rappahannock, and surrounding Counties. For more information about Oak View Bankshares, Inc. and Oak View National Bank, please visit our website at www.oakviewbank.com. Member FDIC.

For additional information, contact Tammy Frazier, Executive Vice President & Chief Financial Officer, Oak View Bankshares, Inc., at 540-359-7155.

Cautionary Note Regarding Forward-Looking Statements

Any statements in this release about expectations, beliefs, plans, objectives, assumptions or future events or performance are not historical facts and are forward-looking statements. These statements are often, but not always, made through the use of words or phrases such as "may," "should," "could," "would," "predict," "potential," "believe," "likely," "expect," "anticipate," "seek," "estimate," "intend," "plan," "project" and similar expressions. Accordingly, these statements involve estimates, assumptions, and uncertainties, and actual results may differ materially from those expressed in such statements. The following factors could cause the Company's actual results to differ materially from those projected in the forward-looking statements made in this document: changes in assumptions underlying the establishment of allowances for credit losses, and other estimates; the risks of changes in interest rates on levels, composition and costs of deposits, loan demand, and the values and liquidity of loan collateral, securities, and interest sensitive assets and liabilities; the effects of future economic, business and market conditions; legislative and regulatory changes, including changes in banking, securities, and tax laws and regulations and their application by our regulators; the Company's ability to maintain adequate liquidity by retaining deposit customers and secondary funding sources, especially if the Company's or banking industry's reputation becomes damaged; computer systems and infrastructure may be vulnerable to attacks by hackers or breached due to employee error, malfeasance, or other disruptions despite security measures implemented by the Company; risks inherent in making loans, such as repayment risks and fluctuating collateral values; governmental monetary and fiscal policies; changes in accounting policies, rules and practices; competition with other banks and financial institutions, and companies outside of the banking industry, including companies that have substantially greater access to capital and other resources; demand, development and acceptance of new products and services; problems with technology utilized by the Company; changing trends in customer profiles and behavior; success of acquisitions and operating initiatives, changes in business strategy or development of plans, and management of growth; reliance on senior management, including the ability to attract and retain key personnel; and inadequate design or circumvention of disclosure controls and procedures or internal controls. These factors could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements made by the Company, and you should not place undue reliance on any such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made and the Company does not undertake any obligation to update any forward-looking statement or statements to reflect events or circumstances after the date on which such statement is made or to reflect the occurrence of unanticipated events. New factors emerge from time to time, and it is not possible for the Company to predict which will arise. In addition, the Company cannot assess the impact of each factor on the Company's business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements.

SOURCE: Oak View Bankshares, Inc.

View the original press release on ACCESS Newswire