Commercial Real Estate in a Post-Pandemic World: Five Years Later

Cushman & Wakefield releases report examining current trends and behavioral changes

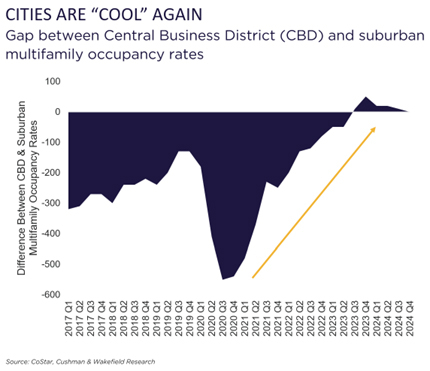

Cities are "cool" again

“The pandemic forced a dramatic reevaluation of how we use and value the built environment and commercial spaces,” said David Smith, Head of Americas Insights. “While some changes have reverted to pre-2020 norms, others have become permanent fixtures in how we live, work and play.”

Key Trends Shaping the Future

Cities Are Rebounding

After an initial exodus, cities are experiencing a resurgence, particularly among younger demographics. Multifamily occupancy rates returned to and even exceeded pre-pandemic levels by late 2021.

The Commute Remains a Challenge

Remote and hybrid work models continue to impact office attendance, with proximity playing a major role in workplace participation. Employees living within a mile of their workplace are returning to the office at over

Consumer Behavior is Normalizing

Many pandemic-driven changes in consumer habits—such as the surge in e-commerce and the decline in restaurant and travel spending—have stabilized. While online shopping spiked by

A Slowdown in New Construction

Higher interest rates, material inflation, and labor costs have curbed new development across all sectors. Industrial and multifamily construction pipelines have dropped below Q1 2020 levels by

The Experience Economy is Expanding

A key takeaway from the report is the increasing importance of experiential spaces in urban environments. Two-thirds of foot traffic in walkable urban centers now comes from visitors rather than residents or employees. However, only 12–

Looking Ahead: Reimagining Cities for the Future

The findings emphasize the need for cities and real estate developers to create more balanced portfolios that integrate living, working and experiential spaces. Mixed-use developments that prioritize convenience, social engagement and entertainment will be key to urban success moving forward.

“As cities continue to evolve, the commercial real estate sector must adapt by designing spaces that foster community and experience,” added Smith. “Investors and developers who embrace these changes will be best positioned for long-term success.”

About Cushman & Wakefield

Cushman & Wakefield (NYSE: CWK) is a leading global commercial real estate services firm for property owners and occupiers with approximately 52,000 employees in nearly 400 offices and 60 countries. In 2024, the firm reported revenue of

View source version on businesswire.com: https://www.businesswire.com/news/home/20250402988846/en/

Media Contact:

Mike Boonshoft

212-841-7505

michael.boonshoft@cushwake.com

Source: Cushman & Wakefield