“WITH YOU AND FOR YOU, CHANGING ORPEA!” THE REFOUNDATION PLAN

ORPEA has announced plans to restore its financial balance by engaging in discussions with unsecured debt holders. The company aims for a 9% annual revenue growth by 2025 and an EBITDAR margin exceeding 20%. The transformation plan, 'WITH YOU AND FOR YOU', emphasizes care quality, employee welfare, and operational improvements. However, ORPEA faces challenges, including a risk of liquidity shortfall in Q1 2023 and significant potential shareholder dilution due to a proposed rights issue. The management aims to rebuild trust and refocus on its core mission of caring for vulnerable populations.

- Targeting 9% annual revenue growth by 2025.

- Planning for EBITDAR margin above 20% by 2025.

- Focus on employee well-being and quality of care through the new transformation plan.

- Risk of liquidity shortfall projected for Q1 2023.

- Potential massive dilution for existing shareholders due to new equity measures.

- The Group's ambition: to recover its status as the leading player in the sector by refocusing on the quality of care and support and the development of its employees

-

In order to achieve this,

ORPEA has to CHANGE!- Change the method: "With You and For You" to involve all its stakeholders in reshaping the Group;

- Change the approach to care and support with continuous improvement in medical and ethical practices and in the safety and well-being of employees;

-

Rebalancing the financing strategy:

-

Improve operational performance:

9% annual revenue growth by 2025, EBITDAR margin above20% in 20251, for an estimated EBITDA excluding IFRS 16 of€745m (12.2% ) in 2025 2 ; - Redefine our property holding strategy (with the potential to dispose of assets as soon as conditions allow) and our geographical scope (restructuring or disposing of countries where the Group does not have an attractive position);

- Restoring a sustainable financial structure.

-

Improve operational performance:

(Graphic: Business Wire)

Faced with this unprecedented situation, with the new management and the unanimous support of the Faced with this unprecedented situation, I am proud to present, with the new management, an ambitious plan for reorganizations in the service of our main mission: to care for the most fragile people.

Today,

We want to give our employees the means and conditions to accomplish the mission that motivates them all: to take care of our patients and residents. To do this, we must build the foundations of renewed trust with all our stakeholders: families, the authorities, the financial markets and shareholders. We will:

- Take care of those who provide care, and give them the desire and the means to do their jobs better and better by redesigning a human resources policy that is equal to the challenges;

- Aim relentlessly for excellence in care and support with a new Medical Director;

- To have a positive social and economic impact, with strong local roots;

- Rebuild a transparent and efficient business model.

In a context that has deteriorated significantly, we must also put in place a new, adapted and sustainable financial structure. This is the essential condition for

We have solid assets to accomplish this reorganization in a growing sector. Our plan "ORPEA CHANGE! WITH YOU AND FOR YOU" sets a target of

In countries where the Group considers that it does not have a sufficiently attractive position,

With a highly committed and motivated management team, and the expertise and support of our 72,000 employees, I am confident in the implementation of our transformation. Together we will successfully reshape ORPEA.”

■ Concrete and rapid actions undertaken from July

Actions were immediately initiated, particularly in

Remedying: getting the company "back on track". This means zero tolerance for unethical practices, transparent review when an institution is challenged, a revised policy for reporting Serious Adverse Events (SAEs), increased attention to recruitment and retention of staff, and a strengthened training system on ethics and good treatment.

Organizing: bring the Group up to the best standards in the sector, structure a Human Resources and salary policy, create an

Remobilizing: regaining our position as a major player in tomorrow's "ageing well" means broadening the dialogue with stakeholders (begun with the Etats Généraux), defining a raison d'être, engaging in a reflection on the company's mission (mission-driven status), inventing tomorrow's care and services, while promoting synergies between our businesses

■ A broader reflection to respond to the challenges of our businesses, to the situation of the Group and to initiate the plan for the re-foundation of

In all our markets, the growth in needs and the increased complexity of care is a major challenge. Between 2021 and 2030, the European population aged over 75 will increase from 66 to 81 million people and the average age of entry into long-term care facilities will rise from 87 to 90, which means that care will be more complex. The need for mental health care is also increasing, with, for example, the prevalence of depressive syndromes rising from

Faced with these needs, the difficulties in recruiting care staff are increasing and the view of staff on their profession is ambivalent: while pride in their profession remains very high, at over

- 72,000 employees worldwide are committed and proud of their mission;

- Proven care protocols;

- More than 1,000 facilities, diversified in their activities and locations.

■ In view of these observations and the Group's situation, the ambition is clear

■

- Priority 1 - With employees, especially caregivers

We must take care of those who provide care and give them the desire and the means to do their job well.

-

To create, together with the employees, the conditions to guarantee their health, safety and well-being at work. In terms of objectives, the Group is aiming for a

20% reduction in work-related accidents by 2025; - Re-design the salary and social policy by fully integrating the social partners;

- To succeed in retaining employees in order to reduce turnover and temporary contracts by investing in continuous training and internal promotion;

- Engage by 2024, all "acting" staff in an active training process leading to qualifications;

-

Anticipate the need for resources by increasing the number of apprenticeship contracts fivefold, i.e. from 200 to 1,000 contracts by 2024 in

France ; - Restore more autonomy and initiative to school directors, with the reduction of administrative tasks and a local Human Resources function;

- Aligning incentives from top management to facility managers on the basis of a new balance: Safety / Health - Quality - Performance;

-

Breaking down silos and providing transparency to establishments to compare their performance and, more broadly, making

ORPEA a collaborative and learning company. - Priority 2 - With patients and residents

In order to meet the new expectations and to develop together the answers to the care and support challenges of tomorrow, Professor

-

To set up a medical project, relying on three key pillars. The facilities’ Medical Commissions, keystone of the system. Scientific council in charge of spreading and implementing state-of-the-art medical and care. And a

Ethics Steering Committee , chaired byEmmanuel Hirsch , that will provide concrete and operational responses to our colleagues, patients, residents, families and all of our stakeholders; - To guarantee the best quality and safety of care at all times with reviewed KPI and Develop a benevolent, non-stigmatising and learning quality culture;

- To promote innovations that benefit patients, residents, families and professionals;

- Playing our part fully in all aspects of care, and in particular providing excellent accommodation with local and enjoyable catering, and offering personalized activities;

- Nurture a more fluid communication between our teams, our patients and residents and their families;

- Personalizing the support of our patients and residents by working on local care and life paths across the Group activities and services offered.

- Priority 3 – with Society as a whole

The Group must have a positive economic and social impact, which means:

- Enhance the ethics and good treatment training system by training over 300 people by the end of 2024;

- Increase employee awareness of the declaration of conflicts of interest;

-

Train

100% of the workforce inFrance by the end of 2023, i.e. a total of 26,000 employees, in the new Code of Ethical Conduct and Corporate Social Responsibility; - Strengthen local roots: with local communities (associations, universities, etc.) and with local healthcare providers.

-

In terms of environmental objectives, the Group aims to: reduce carbon emissions, in kg of Co² per m² per year, by -

17% by 2025 and -32% by 2030; reduce water consumption; recover70% of waste from our construction sites; implement certification for100% of new buildings.

■ Priority 4 – With our various partners

In this respect, the proper management of the real estate portfolio is an essential point. Géry Robert-Ambroix, the Group's new Real Estate Director, will have the main task of putting real estate in its rightful place: a business line serving operations. The medium-term objective is to hold a limited number of proprietary assets (20 to

■ The Group has identified a portfolio of real estate assets estimated at more than

■ In the medium term, creation of a real estate company dedicated to

The Group's future real estate development will be based on very selective criteria, focusing on markets where the Group has a leading position, aiming for a double-digit operating EBITDA margin and a development margin close to

At the same time, the Group has launched a strategic review of its portfolio to focus on the most attractive countries and identify restructuring or disposal plans if necessary.

■ Financial implications of the plan

The Group aims for a gradual turnaround in performance over the period 2022-2025, with:

-

An average increase in the number of facilities of

4% per year, to reach 1,173 sites, and in the number of beds of3.3% per year, to reach 96,806 beds in 2025; -

An average growth in turnover of

9% per year, to reach6.1 billion Euros in 2025; -

EBITDAR margin growth of 340 basis points to

20.4% . This represents an average increase of16% over the period and an EBITDAR ofEUR 1.25 billion in 2025; -

An EBITDA margin excluding IFRS 16 of

12.2% , i.e. an EBITDA excluding IFRS 16 ofEUR 745 million in 2025, up28% over the period 2022-2025.

The evolution of the main financial aggregates is detailed in the table below:

In €m |

2021A |

2022E |

2023E |

2024E |

2025E |

Revenue |

4,299 |

4,688 |

5,326 |

5,737 |

6,102 |

EBITDAR |

1,070 |

797 |

911 |

1,083 |

1,246 |

% EBITDAR |

|

|

|

|

|

EBITDA excl. IFRS 16 |

682 |

358 |

433 |

593 |

745 |

% EBITDAR excl. IFRS 16 |

|

|

|

|

|

The increase in EBITDAR represents an improvement of approximately

The increase in margin is mainly due to the implementation of the WITH YOU AND FOR YOU, CHANGING ORPEA! Plan. For example, the structuring of a Human Resources function will make it possible to reopen beds that are currently closed due to a lack of staff or to bring temporary staff in-house. The plan also includes a section dedicated to patients, residents and their families. It will enable a return to the pre-COVID occupancy rate. The work carried out on the structuring of support functions and in particular the purchasing function will contribute to increasing the margin rate.

The opening of new establishments and the restructuring of existing establishments represents more than

For the period 2022-2025, the Group has an investment plan totaling

In conclusion,

Financial Objectives, liquidity update and update on the Group’s restructuring process

Financial Objectives

The information regarding the Group’s 2023, 2024 and 2025 financial objectives and estimated financial information for the financial year ending

Liquidity update

Since the publication of its Q3 2022 revenue on

All the information on the liquidity situation of the Group, in the short term and in the medium term, is included in annex 1.

Update on the Group’s restructuring process

In accordance with the announcements made in the press release dated

-

An equity conversion of

ORPEA S.A.'s unsecured debt, amounting to€3 ,8 million, by way of a rights issue opened to existing shareholders and backstopped by unsecured lenders; -

1.9-2.1 billion of new money, in the form of (a) new secured debt on assets of the group for a target amount of

€600 million (in order to cover ORPEA S.A.’s funding needs until early summer) and (b) a second share capital increase.

It is important to highlight that the implementation of these transactions would result in a massive dilution for existing shareholders who would decide not to participate.

The objective of the Conciliation process that has been initiated is to find a solution to the capital structure and attract new capital to fund ORPEA’s business plan and cover the risk of a liquidity shortfall as detailed in annex 1 hereto. While the Group has not concluded on the implementation mechanism, this could entail, inter alia, an accelerated safeguard to facilitate closure of the process in the event that unanimity cannot be obtained.

If the company is not able to successfully find a solution in the context of the conciliation,

More information about the Group’s restructuring process is set out in annex 1 hereto.

About

ORPEA ANNOUNCES ITS FINANCIAL OBJECTIVES AND PROVIDE AN UPDATE ON ITS LIQUIDITY POSITION AND PROPOSED RESTRUCTURING

1. Financial Objectives

Main assumptions

The build-up of the Group’s plan and the financial objectives and estimated financial information set out below are based on the following main assumptions:

- A recovery in the occupancy rates and new revenue management policies;

- A ramp-up of the greenfield contribution over time given significant investment over the period;

- A relative stability in the fixed cost base, following strong recruitments and inflationary impacts in 2022 and 2023, allowing the Group to fully benefit from the recovery of its occupancy rates over time and in particular in 2025.

A more disciplined approach to development projects, recognising that significant initiatives have been undertaken to halt or reduce the capex commitments previously initiated, but there are still ongoing commitments that require funding until completion.

In parallel, the Group is constantly identifying, monitoring and updating its pipeline of potential real estate asset sales depending on market conditions and the Group’s ability to execute sizeable sale & lease-back while undertaking in the meantime a comprehensive financial restructuring. The Group contemplates, in the long term, to own 20

Main financial objectives

Financial objectives for 2023, 2024 and 2025

Revenue expected to increase from

- occupancy recovery post covid 19 crisis,

- price increases in line with costs inflation, supported by new revenue management policies, and

-

significant developments already engaged in

France , Benelux,Iberian Peninsula , and Latam as 120 new facilities (net of closing) are expected to open and total number of installed beds3 from 93k in 2023 to 97k in 2025.

-

Group EBITDAR expected to increase from

€0.9 billion in 2023 to€1.1 billion in 2024 and€1.25 billion in 2025 (vs.€1.1 billion in 2021A and€0.8 billion in 2022), mainly through:

- revenue increase, driven by the factors described in the above paragraph,

-

improved margin as a result of a relative stability in the fixed costs base as (a) personnel costs4 and food and energy expenses5, as a % of revenue are projected to normalise over time, and (b) HQ costs, as a % of revenue, are expected to reduce from

6.8% in 2022 to5.8% in 2025, as investments will start yielding a significant payback. - positive impact of the ramp up of greenfield projects in 2024 and 2025.

From 2022-2025, approximately

-

Group EBITDA pre IFRS 16 (after external real estate rental charges) expected to increase from

€0.4 billion in 2023 to€0.6 billion in 2024 and€0.75 billion in 2025 vs.€0.7 billion in 2021A and€0.4 billion 2022E, mainly driven by the factors described above regarding EBITDAR. -

Group operating cash-flows6 expected to increase from

€132 million generated in 2023 to€295 million in 2024 and€471 million in 2025 vs.€59 million in 2022. For the avoidance of doubt, the Group operating cash flows take into account€0.7 billion in cumulative maintenance and IT CAPEX mentioned below.

The Group also plans to finance

Estimated financial information for the financial year ending

The current adverse evolution of the Group’s operating environment and the high level of uncertainty resulting therefrom (in particular with regards to volatility in energy costs and potentially lower than expected recovery on the occupancy rates due to the adverse backdrop relating to the financial restructuring) could affect the Group’s visibility on its performance, which could be lower than expected.

In this context, for the current financial year ending

-

Revenue to be around

€4.7 billion (vs€4.3 billion in 2021); -

EBITDAR to be around

€0.8 billion (i.e. an EBITDAR margin of c.17% ) (vs€1.1 billion in 2021, i.e. an EBITDAR margin of25% ); EBITDA pre IFRS 16 to be around€0.35 billion (vs€0.7 billion in 2021); -

Operating cash-flows to be around

€59 million ; -

Cash Balance expected to be around

€350 million by year-end.

The Group therefore expects its profitability to deteriorate for the financial year ending

2. Liquidity and Debt Update

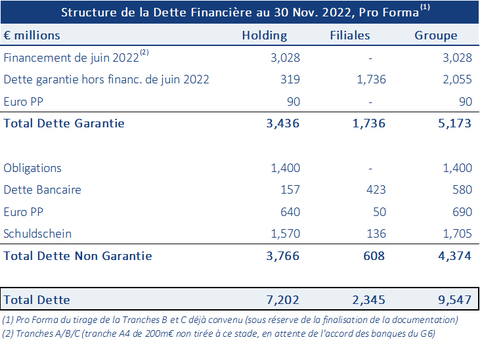

Debt structure and contractual repayment structure

The debt structure of the Group as of

The debt principal schedule of the Group from

Short-term Liquidity Update

Since the publication of its Q3 2022 revenue on

Excluding any new financing and the drawing of the

From

The conciliator will request the voluntary suspension by

Medium-Term Liquidity Shortfall

Over the 2022-2025 period, the cumulated operating cash flow would not allow the Group to fund its committed development capex and contractual debt repayments (details of which are provided in the above table). Based on its existing projections, assuming the existing debt contractual arrangement fall due and without taking into account any interests on cash shortfall, the Group is expected to incur a funding shortfall of

3. Update on the Group’s restructuring process

Difficulties in implementing the real assets disposals program and situation of financial covenants

The financing plan, agreed with the main banking partners in May this year and formalized in

As mentioned in the press release dated

Real estate disposals planned as part of the financing plan announced in

In addition, as mentioned in the press release dated

Immediate actions required

In light of the above, it appears that the Group needs to implement immediate actions, which include the following:

- Reducing significantly the net leverage ratio8 (expected to be at 25x at the end of 2022) and financial expenses, in order to have a sustainable financial structure, to restore ORPEA’s credibility as a counterparty and its capacity to pursue its assets disposals plan

- Raising new money, with the Group’s liquidity being at high risk (see above) in the absence of any asset disposals of a significant size

- Adjustment of the R1 and R2 ratios for all debt having these covenants

Proposed solution

In accordance with the announcements made in the press release dated

To date, the Group confirms the following main elements are being considered:

-

An equity conversion of

ORPEA S.A.'s unsecured debt, amounting to€3.8 billion , by way of a rights issue opened to existing shareholders and which would be backstopped by unsecured lenders which would subscribe to unsubscribed shares by way of set-off against their financial claims, -

€1.9 -2.1 billion of new money, in the form of (a) new secured debt on assets of the group free of any security interests, for a target amount of€600 million (in order to cover ORPEA S.A.’s funding needs until early summer) and (b) a share capital increase which will be offered first to unsecured creditors and shareholders having participated to the first capital increase and then to third party investors, the features of which are not yet determined.

ORPEA S.A. expects that pro forma these equity transactions, at least20% of its share capital will be held by long-term French institutional investors,

- Adjustment of the "R1" and "R2" financial covenants contained in multiple financing agreements not impacted by the conversion of debt into equity,

-

Maturity extension and margin reduction of the secured debt at

ORPEA S.A. , and - Necessary modifications to existing debt to facilitate the implementation of the contemplated restructuring.

The financial restructuring plan as proposed by the Group is expected to significantly reduce its net leverage ratio9, from 25x in 2022E to 6.5x by 2025E (for an estimated net debt of respectively

As indicated above, the Group will solicit interests for the new money debt and equity from all interested parties, including existing stakeholders. The financial restructuring plan as proposed by the Group will include a rights issue opened to all existing shareholders and backstopped by the unsecured creditors through the equity conversion of their unsecured claims.

However, the implementation of such a transaction would result in a massive dilution for existing shareholders who would decide not to participate. Moreover, further dilution is to be expected as a consequence of the new money capital increase, which conditions are not known at the moment.

The implementation of this financial restructuring remains subject to the negotiation of its terms as well as of the necessary documents and agreements. It also remains subject to usual conditions precedent, which include obtaining the favourable support of affected stakeholders (in particular lenders and shareholders), agreed documentation as well as judicial authorizations and approvals.

While the Group has not concluded on the implementation mechanism of the plan, this could entail, inter alia, an accelerated safeguard to facilitate closure of the process in the event that unanimity cannot be obtained.

The Group is confident it is following the right course of actions to secure its long-term future and find a consensual solution with its stakeholders towards addressing its capital structure as there is no other available alternative. There are clear benefits to reposition

Key Next Dates

The next meeting under the Conciliation process with unsecured creditors of

In parallel,

With regards to the equity raise process, binding offers will also be sought for the middle of

Forward-looking information

This press release contains forward-looking statements that involve risks and uncertainties, including references, concerning the Group's expected growth and profitability in the future which may significantly impact the expected performance indicated in the forward-looking statements. These risks and uncertainties are linked to factors out of the control of the Company and not precisely estimated, such as market conditions. Any forward-looking statements made in this press release are statements about the Company’s beliefs and expectations and should be evaluated as such. Actual events or results may differ from those described in this press release due to a number of risks and uncertainties that are described in the Company’s Universal Registration Document available on the company’s website and on the French financial markets regulator, AMF’s website (www.amf-france.org), and in the Half-Year 2022 financial report which is available on the company’s website.

About

1 In the financial year 2021, the EBITDAR margin was

2 EBITDA excluding IFRS 16 for 2022 is estimated at

3 Including nursing homes and clinic beds only

4 Assumed to be back at historical normative levels after the 2022 strong recruitment policy, progressively reducing from

5 With energy assumed to return to a normative level in 2025, but the impact of energy costs is expected to weigh on the Group’s profitability for the first years of the plan, with energy, water and heating costs going from

6 Defined as EBITDA pre-IFRS 16 (-) non-cash items (-) Change in WC (-) Operating Capex (-) Income Taxes Paid

7 Tranche A4 of

8 Net leverage ratio defined as Net Financial Debt / EBITDA Pre-IFRS 16

9 Net leverage ratio defined as Net Financial Debt / EBITDA Pre-IFRS 16

View source version on businesswire.com: https://www.businesswire.com/news/home/20221114006155/en/

Investor Relations

Investor Relations Director

b.lesieur@orpea.net

Investor Relations

NewCap

Dusan Oresansky

Tel.: +33 (0)1 44 71 94 94

ORPEA@newcap.eu

Media Relations

Isabelle Herrier-Naufle

Media Relations Director

Tel.: +33 (0)7 70 29 53 74

i.herrier-naufle@orpea.net

Image 7

Tel.: +33 (0)6 78 37 27 60

clebarbier@image7.fr

Toll free tel. nb for shareholders:

+33 (0) 805 480 480

Source:

FAQ

What are ORPEA's financial targets for 2025?

What is the transformation plan announced by ORPEA?

Is ORPEA facing any financial challenges?

How will ORPEA's restructuring affect shareholders?