Orange County Bancorp (Nasdaq: OBT) reported Q2 2024 net income of $8.2 million, or $1.46 per share, down from $9.1 million in Q2 2023. Key highlights include:

- Net interest income increased 6.7% to $24.1 million - Net interest margin grew 29 basis points to 4.10% - Total deposits rose 7.9% to $2.2 billion - Book value per share increased 7.1% to $31.35 - Trust and investment advisory income rose 15.9% to $3.0 million

The decrease in earnings was primarily due to increases in provision for credit losses and non-interest expenses. The bank reported strong deposit growth and improved net interest margin, while reducing high-cost borrowings.

Orange County Bancorp (Nasdaq: OBT) ha riportato un reddito netto nel secondo trimestre 2024 di 8,2 milioni di dollari, ovvero 1,46 dollari per azione, in calo rispetto ai 9,1 milioni di dollari del secondo trimestre 2023. I punti principali includono:

- Il reddito da interessi netti è aumentato del 6,7% a 24,1 milioni di dollari - Il margine di interesse netto è cresciuto di 29 punti base a 4,10% - Il totale dei depositi è salito del 7,9% a 2,2 miliardi di dollari - Il valore contabile per azione è aumentato del 7,1% a 31,35 dollari - Il reddito da trust e consulenza sugli investimenti è aumentato del 15,9% a 3,0 milioni di dollari

La diminuzione degli utili è stata principalmente causata da un aumento della provvigione per perdite su crediti e delle spese non di interesse. La banca ha registrato una solida crescita dei depositi e un miglioramento del margine di interesse netto, riducendo al contempo i prestiti ad alto costo.

Orange County Bancorp (Nasdaq: OBT) informó de un ingreso neto en el segundo trimestre de 2024 de 8,2 millones de dólares, o 1,46 dólares por acción, una disminución respecto a los 9,1 millones de dólares en el segundo trimestre de 2023. Los puntos clave incluyen:

- Los ingresos netos por intereses aumentaron un 6,7% a 24,1 millones de dólares - El margen de interés neto creció 29 puntos básicos al 4,10% - Los depósitos totales aumentaron un 7,9% a 2,2 mil millones de dólares - El valor contable por acción subió un 7,1% a 31,35 dólares - Los ingresos por fideicomiso y asesoría de inversiones aumentaron un 15,9% a 3,0 millones de dólares

La disminución en las ganancias se debió principalmente a los incrementos en la provisión para pérdidas crediticias y gastos no relacionados con intereses. El banco reportó un sólido crecimiento de los depósitos y mejoró el margen de interés neto, mientras reducían los préstamos de alto costo.

오렌지 카운티 뱅콥(나스닥: OBT)은 2024년 2분기 순이익이 820만 달러, 즉 주당 1.46달러라고 보고했으며, 2023년 2분기 910만 달러에서 감소했습니다. 주요 하이라이트는 다음과 같습니다:

- 순이자수익이 6.7% 증가하여 2410만 달러 - 순이자마진이 29 베이시스 포인트 증가하여 4.10% - 총예금이 7.9% 증가하여 22억 달러 - 주당 장부가치가 7.1% 증가하여 31.35달러 - 신탁 및 투자자문 수익이 15.9% 증가하여 300만 달러

수익 감소는 주로 신용손실에 대한 충당금 증가와 비이자 비용 증가에 기인했습니다. 은행은 강력한 예금 성장을 보고하고 순이자 마진을 개선했으며, 고비용 차입을 줄였습니다.

Orange County Bancorp (Nasdaq: OBT) a annoncé un revenu net au deuxième trimestre 2024 de 8,2 millions de dollars, soit 1,46 dollar par action, en baisse par rapport à 9,1 millions de dollars au deuxième trimestre 2023. Les points forts incluent :

- Le revenu net d'intérêts a augmenté de 6,7 % à 24,1 millions de dollars - La marge d'intérêt net a crû de 29 points de base à 4,10 % - Le montant total des dépôts a augmenté de 7,9 % pour atteindre 2,2 milliards de dollars - La valeur comptable par action a augmenté de 7,1 % à 31,35 dollars - Les revenus des fiducies et du conseil en investissement ont augmenté de 15,9 % à 3,0 millions de dollars

La baisse des bénéfices est principalement due à des augmentations des provisions pour créances douteuses et des dépenses non liées aux intérêts. La banque a rapporté une forte croissance des dépôts et une amélioration de la marge d'intérêt nette, tout en réduisant les emprunts à coût élevé.

Orange County Bancorp (Nasdaq: OBT) berichtete über einen Nettogewinn im zweiten Quartal 2024 von 8,2 Millionen US-Dollar, was 1,46 US-Dollar pro Aktie entspricht, ein Rückgang gegenüber 9,1 Millionen US-Dollar im zweiten Quartal 2023. Zu den wichtigsten Highlights gehören:

- Der Nettzinsüberschuss stieg um 6,7% auf 24,1 Millionen US-Dollar - Die Nettzinsmarge wuchs um 29 Basispunkte auf 4,10% - Die Gesamtguthaben stiegen um 7,9% auf 2,2 Milliarden US-Dollar - Buchwert pro Aktie erhöhte sich um 7,1% auf 31,35 US-Dollar - Einnahmen aus Treuhand- und Anlageberatung stiegen um 15,9% auf 3,0 Millionen US-Dollar

Der Rückgang des Gewinns war hauptsächlich auf Anstiege in der Rückstellungen für Kreditausfälle und nicht-zinsbezogene Ausgaben zurückzuführen. Die Bank meldete ein starkes Einlagenwachstum und verbesserte die Nettzinsmarge, während sie teure Kredite reduzierte.

Positive

Net interest income increased 6.7% to $24.1 million

Net interest margin grew 29 basis points to 4.10%

Total deposits rose 7.9% to $2.2 billion

Book value per share increased 7.1% to $31.35

Trust and investment advisory income rose 15.9% to $3.0 million

Reduced high-cost borrowings from $234.5 million to $60 million

Assets under management in Wealth Management division increased 8.6% to $1.7 billion

Negative

Net income decreased 9.6% to $8.2 million compared to Q2 2023

Provision for credit losses increased to $2.2 million from $214,000 in Q2 2023

Non-interest expense increased 7.2% to $15.5 million

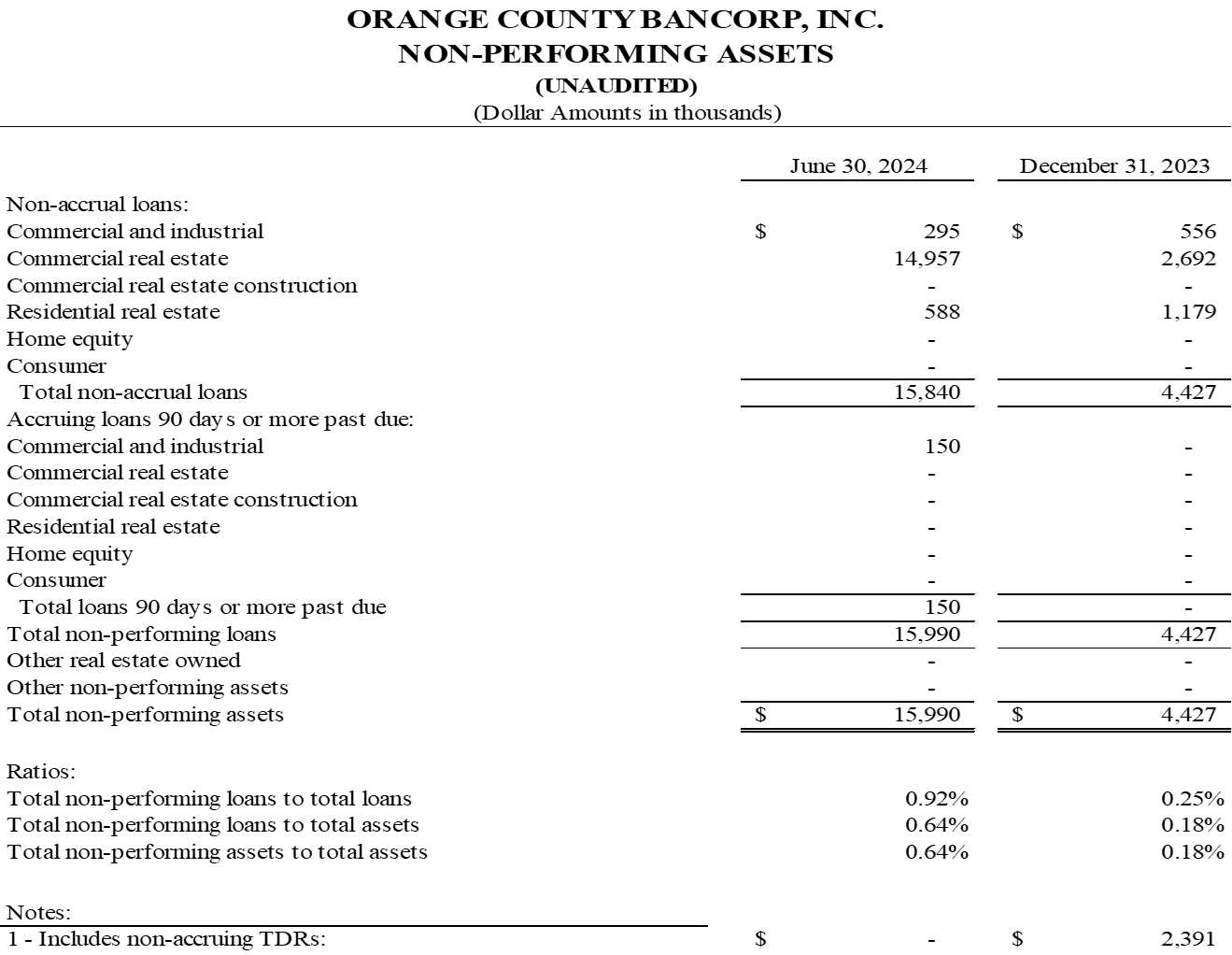

Non-performing loans increased to $16.0 million, or 0.92% of total loans

Total loans decreased 0.8% to $1.7 billion

Insights

Orange County Bancorp's Q2 2024 results present a mixed picture with some positive developments offset by challenges. The 6.7% increase in Net Interest Income to $24.1 million and the 29 basis point growth in Net Interest Margin to 4.10% are encouraging signs. These improvements, coupled with the 7.9% rise in Total Deposits to $2.2 billion, demonstrate the bank's ability to navigate the challenging rate environment effectively.

However, the decrease in net income from $9.1 million in Q2 2023 to $8.2 million in Q2 2024 is a concern. This decline was primarily due to an increased provision for credit losses and higher non-interest expenses. The jump in provision for credit losses from $214,000 in Q2 2023 to $2.2 million in Q2 2024 is particularly noteworthy and warrants close monitoring.

On a positive note, the bank's efforts to reduce external borrowings have been successful, with a significant decrease from $234.5 million at year-end 2023 to $60 million at the end of Q2 2024. This reduction, combined with deposit growth and improved loan yields, has contributed to the healthy expansion of the net interest margin.

The Wealth Management division continues to be a strong performer, with trust and investment advisory income rising 15.9% year-over-year. This diversification of revenue streams is a strategic advantage for the bank.

Overall, while the bank faces some challenges, particularly in credit quality, its core operations show resilience and strategic adaptability in a complex economic environment.

The Q2 2024 results for Orange County Bancorp highlight several risk factors that warrant attention. The most significant concern is the sharp increase in non-performing loans, which rose to $16.0 million, or 0.92% of total loans, up from $4.4 million at the end of 2023. This surge was primarily due to a single commercial real estate participation loan, indicating potential vulnerabilities in the bank's loan portfolio.

The provision for credit losses jumped to $2.2 million in Q2 2024, a substantial increase from $214,000 in Q2 2023. This rise suggests growing concerns about loan quality and could impact future earnings if the trend continues. The allowance for credit losses to total loans ratio increased to 1.60%, up from 1.44% at year-end 2023, reflecting the bank's more cautious stance on potential loan losses.

On a positive note, the bank has made significant progress in reducing its reliance on external borrowings, which could help mitigate liquidity risks. The decrease in FHLBNY short-term borrowings from $224.5 million to zero is a notable achievement. However, the bank still maintains $122.5 million in brokered deposits, which can be a less stable funding source compared to core deposits.

The bank's capital ratios remain strong, with the Tier 1 capital to average assets ratio at 10.04%, well above regulatory standards for well-capitalized institutions. This provides a buffer against potential losses and supports the bank's ability to navigate challenging economic conditions.

Overall, while the bank demonstrates resilience in many areas, the deterioration in loan quality and the significant increase in credit loss provisions are red flags that require close monitoring and proactive risk management strategies.

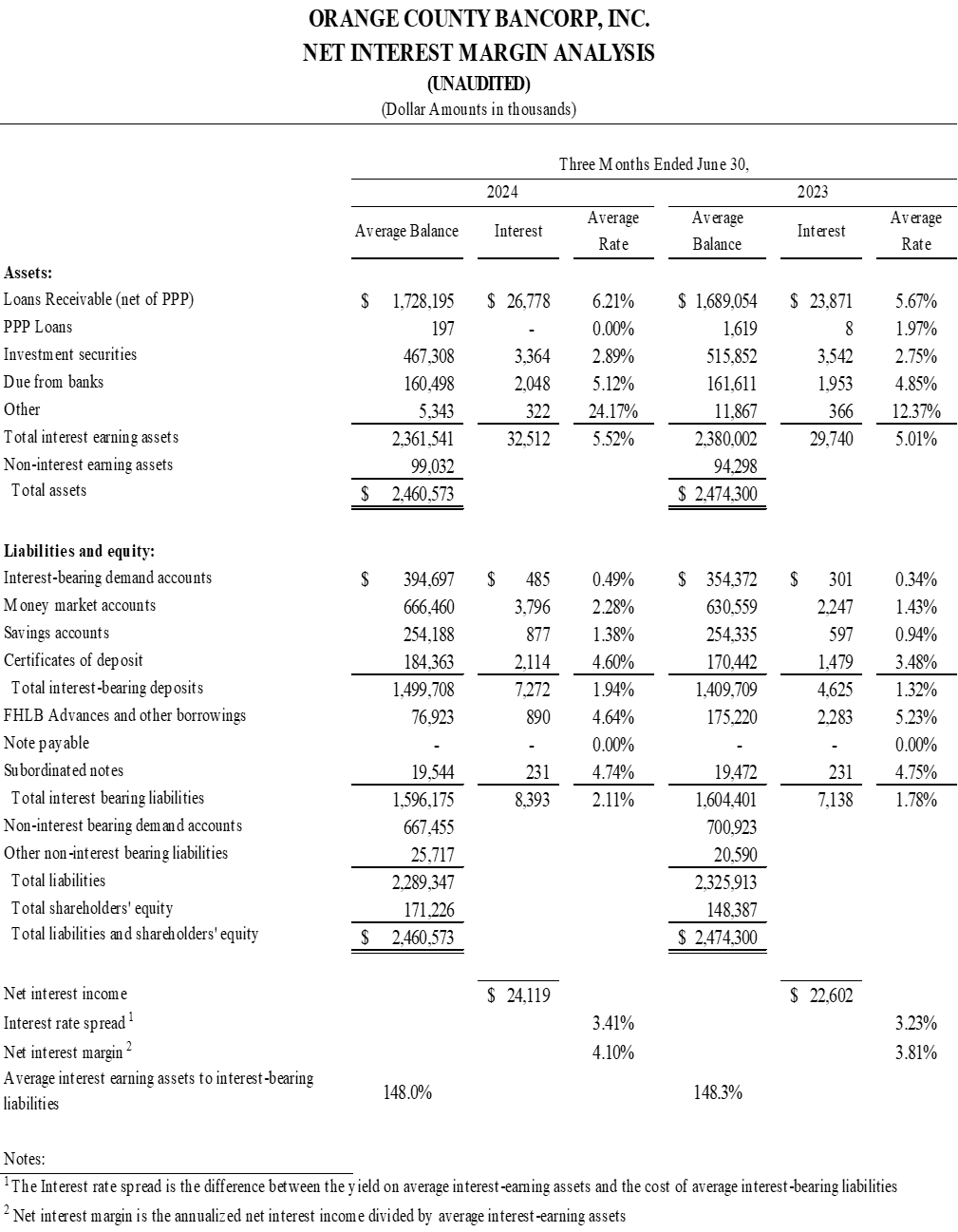

Net Interest Income increased $1.5 million, or 6.7%, to $24.1 million for the quarter ended June 30, 2024 from $22.6 million for the quarter ended June 30, 2023

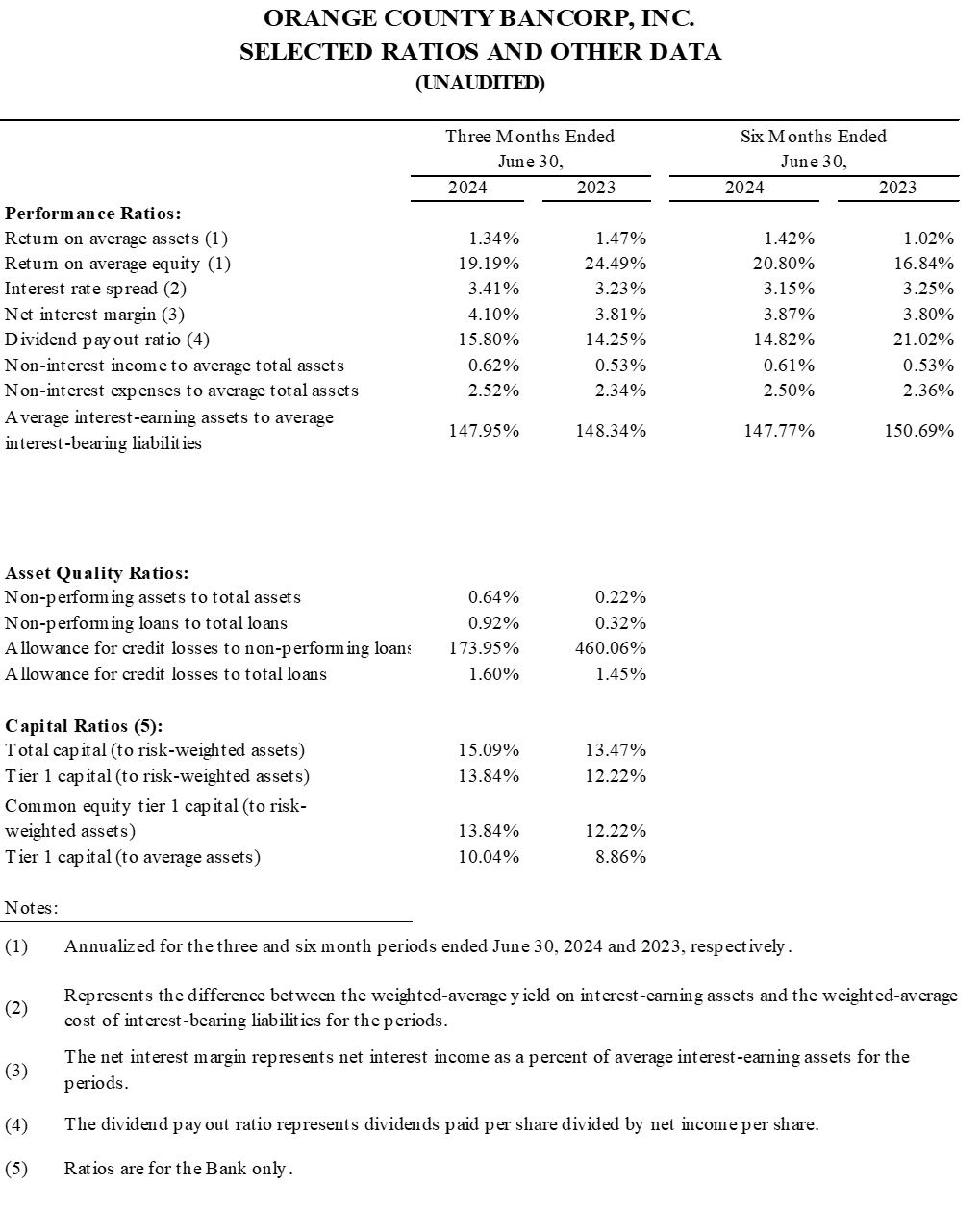

Net Interest Margin grew 29 basis points, or 7.6%, to 4.10% for the quarter ended June 30, 2024, as compared to 3.81% for the quarter ended June 30, 2023

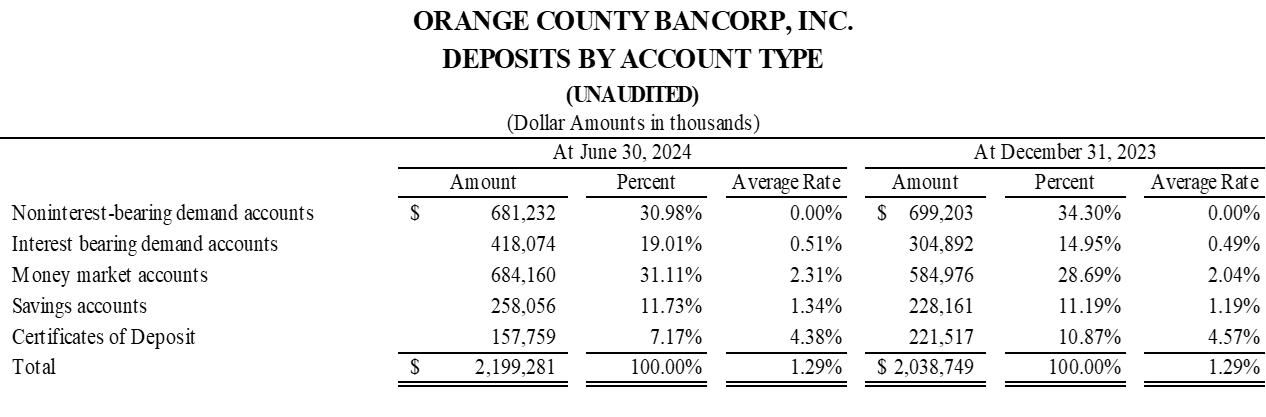

Total Deposits rose $160.5 million, or 7.9%, to $2.2 billion at June 30, 2024 from $2.0 billion at year-end 2023

Book value per share increased $2.09, or 7.1%, to $31.35 at June 30, 2024 from $29.26 at December 31, 2023

Trust and investment advisory income rose 15.9%, to approximately $3.0 million for the quarter ended June 30, 2024, from $2.6 million for Q2 2023

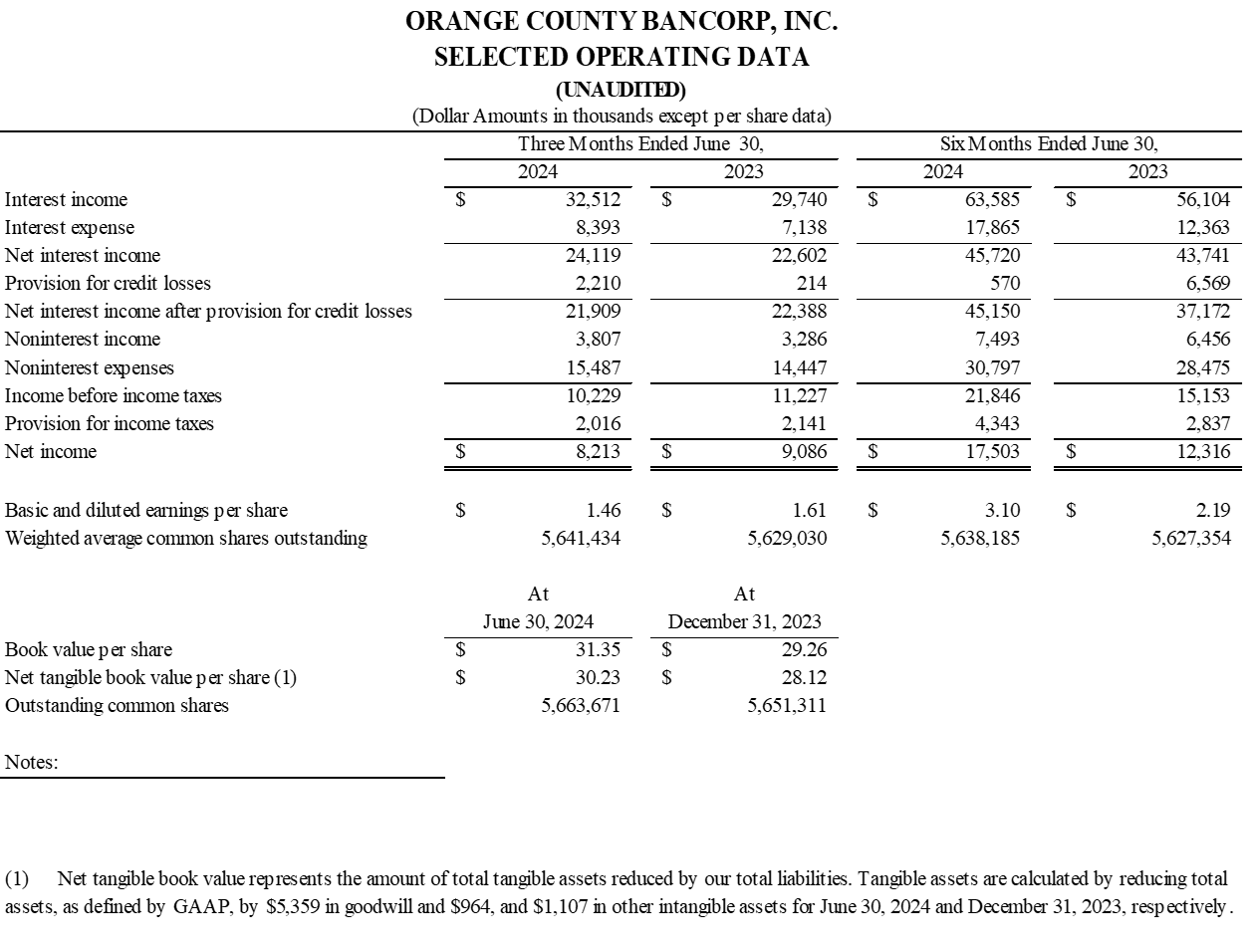

MIDDLETOWN, KY / ACCESSWIRE / July 31, 2024 / Orange County Bancorp, Inc. (the "Company") (Nasdaq:OBT), parent company of Orange Bank & Trust Co. (the "Bank") and Hudson Valley Investment Advisors, Inc. ("HVIA"), today announced net income of $8.2 million, or $1.46 per basic and diluted share, for the three months ended June 30, 2024. This compares with net income of $9.1 million, or $1.61 per basic and diluted share, for the three months ended June 30, 2023. The decrease in earnings per share, basic and diluted, was due primarily to increases in the provision for credit losses and non-interest expense offset by increases in net interest income and non-interest income during the current period. For the six months ended June 30, 2024, net income reached $17.5 million, or $3.10 per basic and diluted share, as compared to $12.3 million, or $2.19 per basic and diluted share, for the six months ended June 30, 2023.

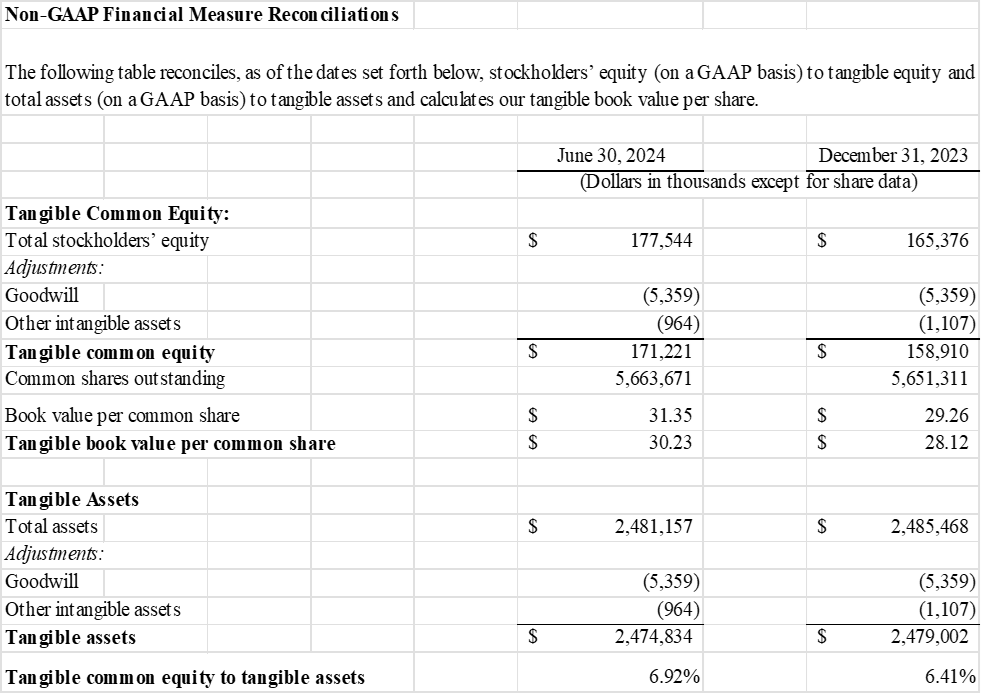

Book value per share rose $2.09, or 7.1%, from $29.26 at December 31, 2023 to $31.35 at June 30, 2024. Tangible book value per share increased $2.11, or 7.5%, from $28.12 at December 31, 2023 to $30.23 at June 30, 2024 (see "Non-GAAP Financial Measure Reconciliation" below for additional detail). These increases were due primarily to increased earnings during the six months ended June 30, 2024.

"Though it wasn't without challenges, I am pleased to report another excellent quarter of financial performance," announced Company President and CEO Mike Gilfeather, "For the second quarter of 2024 we recorded net income of $8.2 million versus $9.1 million the same period last year. Strong earnings during the quarter were negatively impacted by a credit impairment charge on one of our participation loans, which resulted in a net increase in our provision for credit losses.

Our total loan portfolio at quarter end stood at $1.7 billion. The Bank funded $29.2 million in new loans during the quarter, which were offset by loan repayment. As I've mentioned previously, regional loan demand remains strong, but uncertainty surrounding the Federal Reserve rate policy and overall industry volatility have caused us to slow loan origination in favor of maintaining and modestly improving rates in our loan portfolio. These actions helped push the average yield on our loan portfolio to 6.21% during Q2 2024 from 5.91% for Q1 2024.

This quarter also saw the results of our ongoing effort to increase deposits, despite today's challenging rate environment. Total deposits rose $160.5 million, or 7.9%, during the quarter to $2.2 billion at June 30, 2024, from $2.0 billion at year-end 2023. The bulk of these were relationship driven and, as such, carry a lower cost than broker originated deposits. The average cost of deposits stood at 1.34% for the second quarter, which is flat from last quarter, and up 46 basis points from 0.88% a year ago. While I am confident in the Bank's ability to gather deposits across rate environments, this result was particularly noteworthy.

This quarter also saw a continuation of our efforts to pay down external borrowings, which we secured last year in response to broad industry concerns stemming from the rapid rise in interest rates. We are fortunate our financial results continue to provide the opportunity to replace these expensive liquidity sources with more reasonably priced ones generated through deposit gathering. This year alone, we have reduced these borrowings from $234.5 million at year end 2023 to just $60 million at the end of Q2 2024.

The increased yield on our loan portfolio, growth in low cost deposits, and significant reduction of high-cost borrowings have all led to healthy expansion of our net interest margin. During the quarter, NIM rose 29 basis points, or 7.6%, to 4.10%, as compared to 3.81% for the quarter ended June 30, 2023.

Our Wealth Management division also remained a strong performer during the quarter. Trust and investment advisory income rose $405 thousand, or 15.9%, to $3.0 million for Q2 2024 from $2.6 million for the same period last year. Additionally, while year-over-year performance has been strong, HVIA's continued growth in the context of more volatile and uncertain fixed-income market performance is all the more impressive. I would add that these results aren't dependent upon or correlated with our traditional banking business, making Wealth Management an increasingly important source of diversified revenue for the Bank

In many ways, this quarter highlights the results of our very focused business strategy. Our performance resulted from an intentional effort to moderate loan growth in favor of higher rates, a bank wide, multi-year effort to grow core deposits, and a specific plan to replace expensive borrowings with lower cost funding. And though we executed on all of these to great effect, we remain subject to the traditional risks of lending which, unfortunately, resulted in the recognition of a participation loan impairment which impacted an otherwise outstanding quarter. I want to thank our employees once again for their tireless effort, flexibility and commitment to our work. Their ability to respond to challenges and consistently deliver these types of results reflects the knowledge and experience that makes our approach to business banking successful. Thanks as well to our shareholders for their continued support."

Second Quarter 2024 Financial Review

Net Income

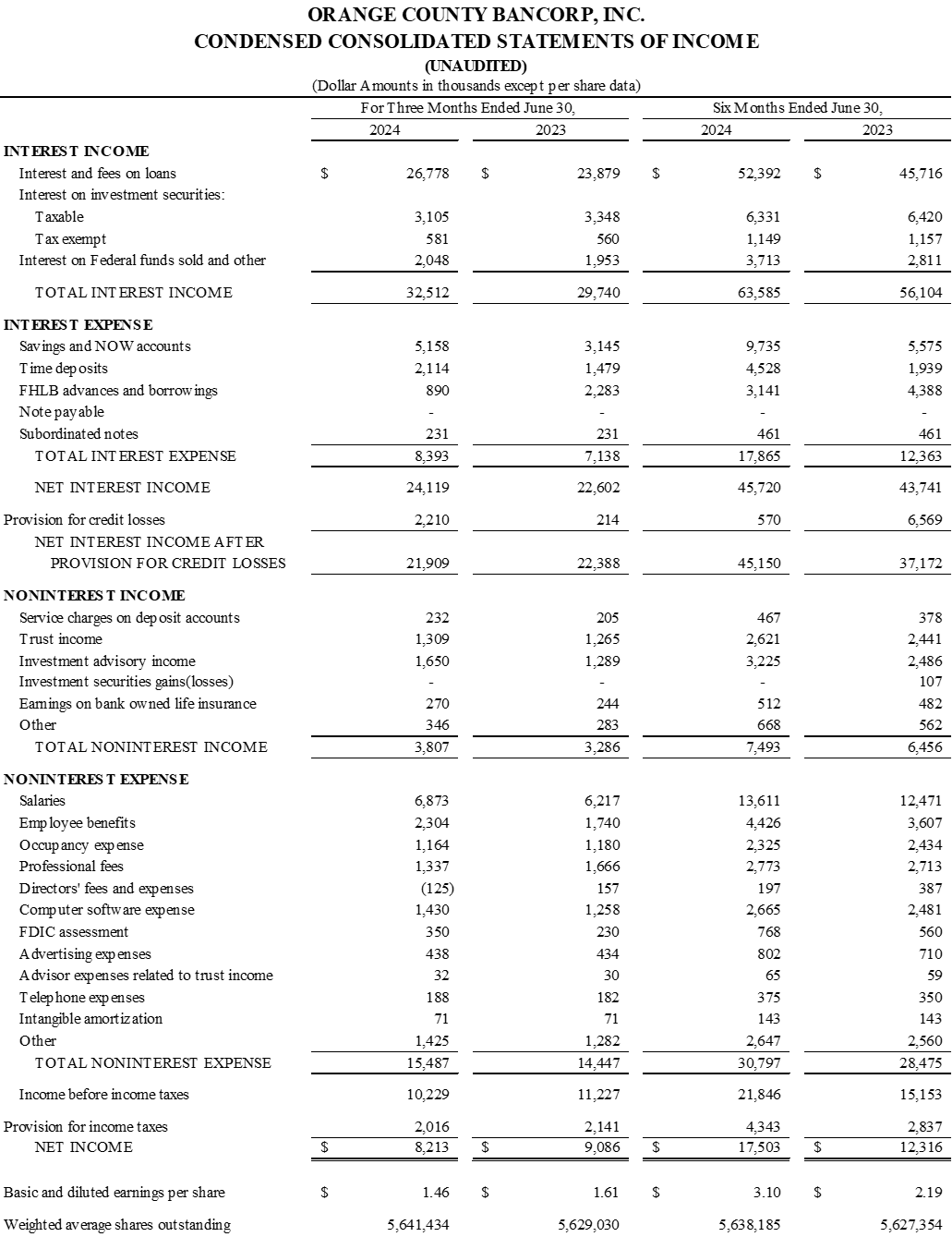

Net income for the second quarter of 2024 was $8.2 million, a decrease of $873 thousand, or 9.6%, from net income of $9.1 million for the second quarter of 2023. The decrease represents a combination of an increased provision for credit losses and increased interest and non-interest expense over the same quarter last year. Net income for the six months ended June 30, 2024 was $17.5 million, as compared to $12.3 million for the same period in 2023. The increase reflects the effect of net interest income growth combined with reduced provision for credit losses during the first six months of 2024 as compared to the prior period. The reduced provision includes the positive impact of a recovery in 2024 associated with the write-off of Signature Bank subordinated debt during the first quarter of 2023.

Net Interest Income

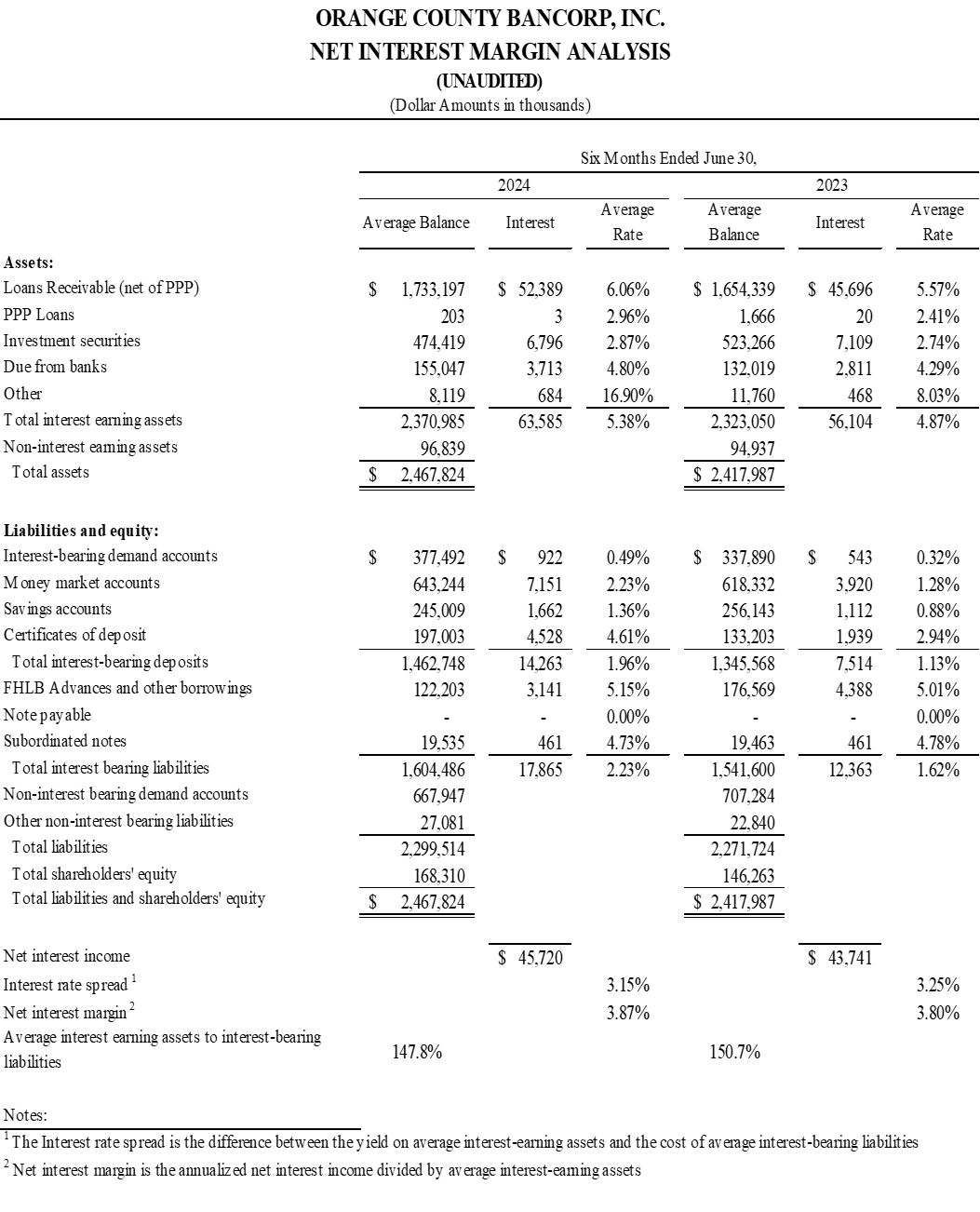

For the three months ended June 30, 2024, net interest income rose $1.5 million, or 6.7%, to $24.1 million, versus $22.6 million during the same period last year. The increase was driven primarily by a $2.9 million increase in interest and fees on loans during the current period. For the six months ended June 30, 2024, net interest income reached $45.7 million representing an increase of $2.0 million, or 4.5%, over the first half of 2023.

Total interest income rose $2.8 million, or 9.3%, to $32.5 million for the three months ended June 30, 2024, compared to $29.7 million for the three months ended June 30, 2023. The increase reflected 12.1% growth in interest and fees associated with loans, a 3.8% increase in interest income from tax-exempt investment securities, and a 4.9% increase in interest income related to fed funds interest and balances held at correspondent banks. For the six months ended June 30, 2024, total interest income rose $7.5 million, or 13.3%, to $63.6 million as compared to $56.1 million for the six months ended June 30, 2023.

Total interest expense increased $1.3 million during the second quarter of 2024, to $8.4 million, as compared to $7.1 million in the second quarter of 2023. The increase represented the continued combined effect of rising interest rates on customer deposits as well as higher costs associated with brokered deposits as alternate sources of funding. Interest expense associated with savings and NOW accounts totaled $5.2 million during the second quarter of 2024 as compared to $3.2 million during the second quarter of 2023. Interest expense associated with FHLB advances drawn and other borrowings during the current quarter totaled $890 thousand as compared to $2.3 million during the second quarter of 2023. During the six months ended June 30, 2024, total interest expense rose $5.5 million, to $17.9 million, as compared to $12.4 million for the same period last year.

Provision for Credit Losses

As of January 1, 2023, the Company adopted the current expected credit losses methodology ("CECL") accounting standard, which includes loans individually evaluated, as well as loans evaluated on a pooled basis to assess the adequacy of the allowance for credit losses. The Bank seeks to estimate lifetime losses in its loan and investment portfolio by using expected discounted cash flows and supplemental qualitative considerations, including relevant economic considerations, portfolio concentrations, and other external factors, as well as evaluating investment securities held by the Bank.

The Company recognized a provision for credit losses of $2.2 million for the three months ended June 30, 2024, as compared to $214 thousand for the three months ended June 30, 2023. This increase was primarily driven by a reserve associated with a specific non-accrual loan as well as the impact of the methodology associated with estimated lifetime losses and the types of loans closed during the quarter. The allowance for credit losses to total loans was 1.60% as of June 30, 2024 versus 1.44% as of December 31, 2023. For the six months ended June 30, 2024, the provision for credit losses totaled $570 thousand as compared to $6.6 million for the six months ended June 30, 2023. No reserves for investment securities were recorded during 2024.

Non-Interest Income

Non-interest income rose $521 thousand, or 15.9%, to $3.8 million for the three months ended June 30, 2024 as compared to $3.3 million for the three months ended June 30, 2023. This growth was related to continued increased fee income within each of the Company's fee income categories, including investment advisory income, trust income, and service charges on deposit accounts. For the six months ended June 30, 2024, non-interest income increased approximately $1.0 million, to $7.5 million, as compared to $6.5 million for the six months ended June 30, 2023.

Non-Interest Expense

Non-interest expense was $15.5 million for the second quarter of 2024, reflecting an increase of $1.0 million, or 7.2%, as compared to $14.5 million for the same period in 2023. The increase in non-interest expense for the three-month period continues to reflect the Company's commitment to growth. This investment consists primarily of increases in compensation, information technology, and deposit insurance costs. Our efficiency ratio improved to 55.5% for the three months ended June 30, 2024, from 55.8% for the same period in 2023. For the six months ended June 30, 2024, our efficiency ratio increased to 57.9% from 56.7% for the same period in 2023. Non-interest expense for the six months ended June 30, 2024 reached $30.8 million, reflecting a $2.3 million increase over non-interest expense of $28.5 million for the six months ended June 30, 2023.

Income Tax Expense

Provision for income taxes for the three months ended June 30, 2024 was $2.0 million, compared to $2.1 million for the same period in 2023. The decrease was directly related to lower income before income taxes. For the six months ended June 30, 2024, the provision for income taxes was $4.3 million as compared to $2.8 million for the six months ended June 30, 2023. Our effective tax rate for the three-month period ended June 30, 2024 was 19.7% as compared to 19.1% for the same period in 2023. Our effective tax rate for the six-month period ended June 30, 2024 was 19.9% as compared to 18.7% for the same period in 2023.

Financial Condition

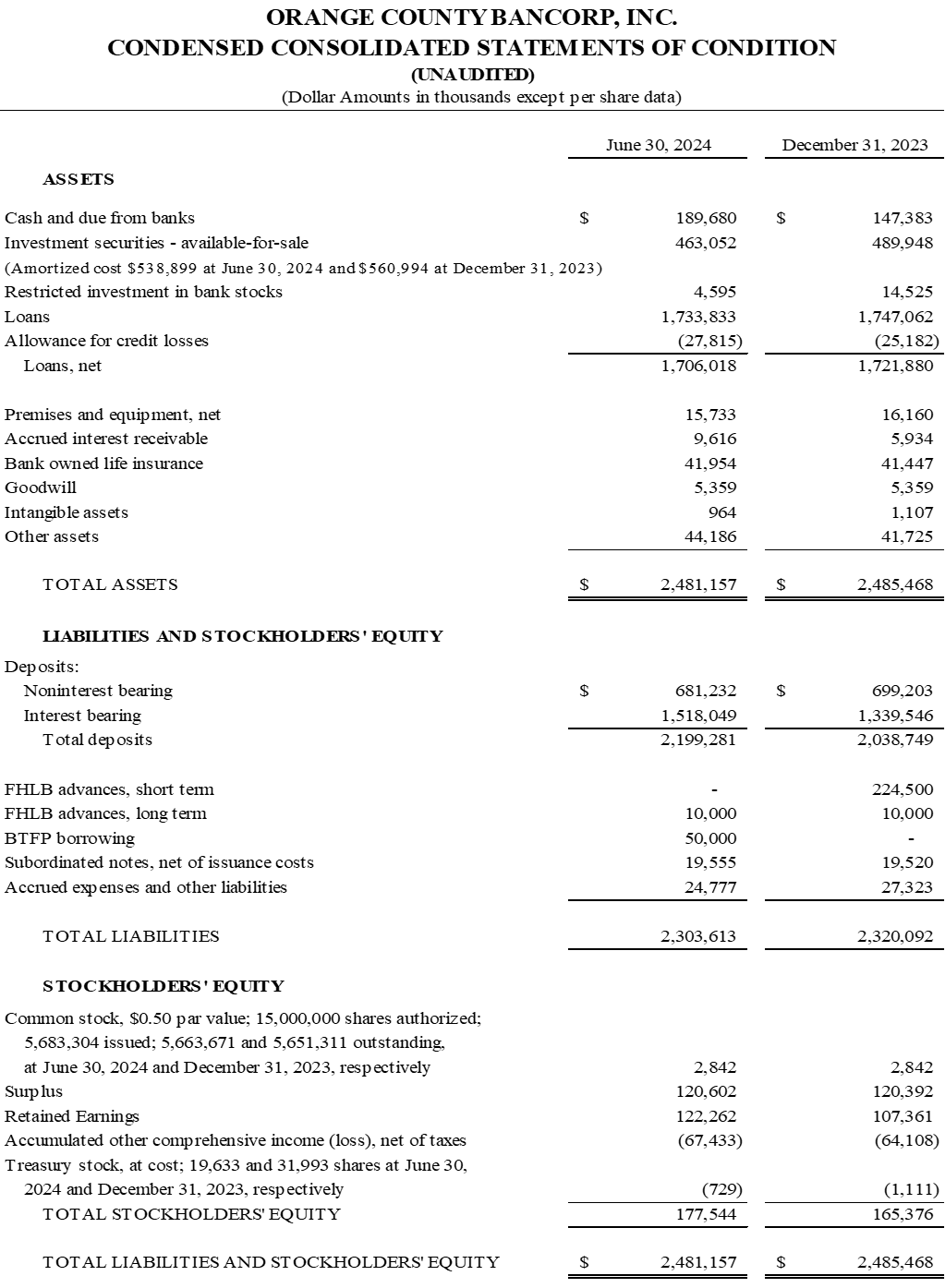

Total consolidated assets decreased $4.3 million, or 0.2%, and remained relatively level at $2.5 billion at June 30, 2024 and December 31, 2023, respectively. The stability of the balance sheet included increases and continued growth in deposits and cash as well as paydowns of borrowings during the current six-month period.

Total cash and due from banks increased from $147.4 million at December 31, 2023, to $189.7 million at June 30, 2024, an increase of approximately $42.3 million, or 28.7%. This increase resulted primarily from increases in deposit balances and slower loan growth which increased cash levels while reducing short-term borrowings.

Total investment securities fell $36.8 million, or 7.3%, from $504.5 million at December 31, 2023 to $467.7 million at June 30, 2024. The decrease continues to be driven primarily by investment maturities during the first six months of 2024.

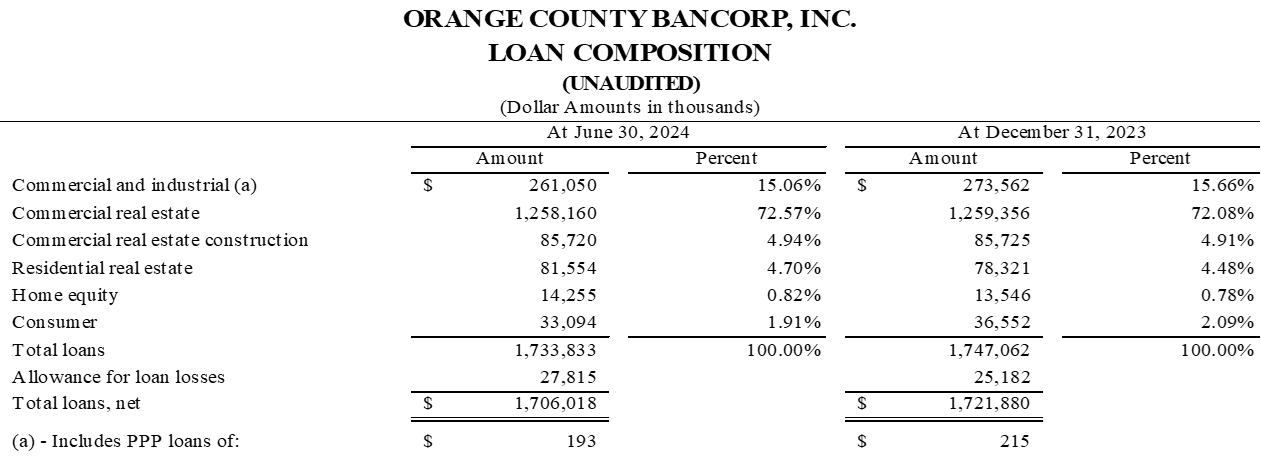

Total loans decreased $13.2 million, or 0.8%, from $1.7 billion at December 31, 2023 to $1.7 billion at June 30, 2024. The decrease was primarily driven by a decrease of $12.5 million related to commercial and industrial loans as well as a $3.5 million decrease in consumer loans offset by an increase of $3.2 million in residential real estate. All other loan categories were relatively stable during 2024.

Total deposits increased $160.5 million, to $2.2 billion at June 30, 2024, from $2.0 billion at December 31, 2023. This increase was due primarily to $113.2 million of growth in interest bearing demand accounts; $99.2 million of growth in money market accounts; and $29.9 million of growth in savings accounts. The increases in deposit accounts were offset by an $18.0 million decrease in noninterest-bearing demand accounts and a $63.8 million decrease in certificates of deposit, mainly associated with brokered deposits utilized by the Bank for short term funding purposes. Deposit composition at June 30, 2024 included 50.0% in demand deposit accounts (including NOW accounts) as a percentage of total deposits. Uninsured deposits, net of fully collateralized municipal relationships, remain stable and represent approximately 40% of total deposits at June 30, 2024 as compared to 37% of total deposits at December 31, 2023.

FHLBNY short-term borrowings were paid off and there was no amount outstanding as of June 30, 2024 as compared to $224.5 million at December 31, 2023. The decrease in borrowings continues to be driven by increased deposits which outpaced loan growth during the first half of 2024 and allowed for paydowns of borrowings while maintaining consistent levels of cash at June 30, 2024. The decrease in borrowings reflects a strategic decision to manage liquidity sources and take advantage of opportunities to reduce funding costs.

Stockholders' equity experienced an increase of approximately $12.2 million during the first half of 2024, reaching $177.5 million at June 30, 2024 from $165.4 million at December 31, 2023. The increase was due primarily to $17.5 million of net income during the first half of 2024 partially offset by an increase in unrealized losses of approximately $3.3 million on the market value of investment securities within the Company's equity as accumulated other comprehensive income (loss) ("AOCI"), net of taxes.

At June 30, 2024, the Bank maintained capital ratios in excess of regulatory standards for well capitalized institutions. The Bank's Tier 1 capital to average assets ratio was 10.04%, both common equity and Tier 1 capital to risk weighted assets were 13.84%, and total capital to risk weighted assets was 15.09%.

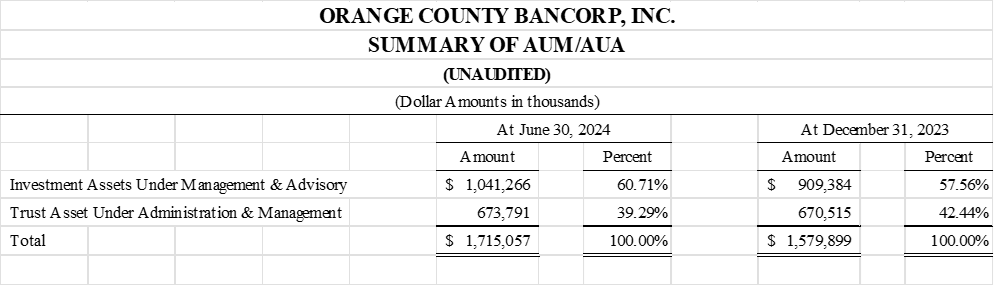

Wealth Management

At June 30, 2024, our Wealth Management Division, which includes trust and investment advisory, totaled $1.7 billion in assets under management or advisory as compared to $1.6 billion at December 31, 2023, reflecting an increase of 8.6%. Trust and investment advisory income for the quarter ended June 30, 2024 reached $3.0 million and represented an increase of 15.9%, or $405 thousand, as compared to $2.6 million for the quarter ended June 30, 2023.

The breakdown of trust and investment advisory assets as of June 30, 2024 and December 31, 2023, respectively, is as follows:

Loan Quality

At June 30, 2024, the Bank had total non-performing loans of $16.0 million, or 0.92% of total loans. Total non-accrual loans represented approximately $15.8 million of loans as of June 30, 2024 compared to $4.4 million at December 31, 2023. The increase in non-accrual loans was primarily the result of one commercial real estate participation which has experienced payment slowdowns and required classification as non-accrual at quarter end.

Liquidity

Management believes the Bank has the necessary liquidity to meet normal business needs. The Bank uses a variety of resources to manage its liquidity position. These include short term investments, cash from lending and investing activities, core-deposit growth, and non-core funding sources, such as time deposits exceeding $250,000, brokered deposits, FHLBNY advances, and other borrowings. As of June 30, 2024, the Bank's cash and due from banks totaled $189.7 million. The Bank maintains an investment portfolio of securities available for sale, comprised mainly of US Government agency and treasury securities, Small Business Administration loan pools, mortgage-backed securities, and municipal bonds. Although the portfolio generates interest income for the Bank, it also serves as an available source of liquidity and funding. As of June 30, 2024, the Bank's investment in securities available for sale was $463.1 million, of which $59.9 million was not pledged as collateral and additional $45.2 million with the Federal Reserve which is not specifically designated to any borrowings. Additionally, as of June 30, 2024, the Bank's overnight advance line capacity at the Federal Home Loan Bank of New York was $611.0 million, of which $90.0 million was used to collateralize municipal deposits and $10.0 million was utilized for long term advances. As of June 30, 2024, the Bank's unused borrowing capacity at the FHLBNY was $511.0 million. The Bank also maintains additional borrowing capacity of $20 million with other correspondent banks. Additional funding is available to the Bank through the discount window lending by the Federal Reserve. At June 30, 2024, the Bank was utilizing $50 million of funding through the Bank Term Funding Program from the Federal Reserve under a one-year facility.

The Bank also considers brokered deposits an element of its deposit strategy. As of June 30, 2024, the Bank had brokered deposit arrangements with various terms totaling $122.5 million.

About Orange County Bancorp, Inc

Orange County Bancorp, Inc. is the parent company of Orange Bank & Trust Company and Hudson Valley Investment Advisors, Inc. Orange Bank & Trust Company is an independent bank that began with the vision of 14 founders over 125 years ago. It has grown through innovation and an unwavering commitment to its community and business clientele to approximately $2.5 billion in total assets. Hudson Valley Investment Advisors, Inc. is a Registered Investment Advisor in Goshen, NY. It was founded in 1996 and acquired by the Company in 2012.

Forward Looking Statements

Certain statements contained herein are "forward looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward looking statements may be identified by reference to a future period or periods, or by the use of forward looking terminology, such as "may," "will," "believe," "expect," "estimate," "anticipate," "continue," or similar terms or variations on those terms, or the negative of those terms. Forward looking statements are subject to numerous risks and uncertainties, including, but not limited to, those related to the real estate and economic environment, particularly in the market areas in which the Company operates, competitive products and pricing, fiscal and monetary policies of the U.S. Government, inflation, changes in government regulations affecting financial institutions, including regulatory fees and capital requirements, changes in prevailing interest rates, increased levels of loan delinquencies, problem assets and foreclosures, credit risk management, asset-liability management, cybersecurity risks, geopolitical conflicts, public health issues, the financial and securities markets and the availability of and costs associated with sources of liquidity.

The Company wishes to caution readers not to place undue reliance on any such forward looking statements, which speak only as of the date made. The Company wishes to advise readers that the factors listed above could affect the Company's financial performance and could cause the Company's actual results for future periods to differ materially from any opinions or statements expressed with respect to future periods in any current statements. The Company does not undertake and specifically declines any obligation to publicly release the results of any revisions that may be made to any forward looking statements to reflect events or circumstances after the date of such statements or to reflect the occurrence of anticipated or unanticipated events.

What was Orange County Bancorp's (OBT) net income for Q2 2024?

Orange County Bancorp (OBT) reported net income of $8.2 million for Q2 2024, or $1.46 per share.

How did Orange County Bancorp's (OBT) net interest margin change in Q2 2024?

Orange County Bancorp's (OBT) net interest margin grew 29 basis points to 4.10% in Q2 2024 compared to 3.81% in Q2 2023.

What was the growth in total deposits for Orange County Bancorp (OBT) in Q2 2024?

Orange County Bancorp (OBT) reported total deposits rose 7.9% to $2.2 billion in Q2 2024 from $2.0 billion at year-end 2023.

How did Orange County Bancorp's (OBT) trust and investment advisory income perform in Q2 2024?

Orange County Bancorp's (OBT) trust and investment advisory income rose 15.9% to approximately $3.0 million in Q2 2024 compared to $2.6 million in Q2 2023.

An email has been sent to your address with instructions for changing your password.

There is no user registered with this email.

Sign Up

To create a free account, please fill out the form below.

Thank you for signing up!

A confirmation email has been sent to your email address. Please check your email and follow the instructions in the message to complete the registration process. If you do not receive the email, please check your spam folder or contact us for assistance.

Welcome to our platform!

Oops!

Something went wrong while trying to create your new account. Please try again and if the problem persist, Email Us to receive support.