The FICO UK Credit Card Market Report for February 2024 shows a mixed picture on consumer confidence and financial pressures. While there was an increase in spending post-seasonal dip in January, payments to balance fell by 3.6% compared to the previous year. Average credit card balance increased by 6.6% year-on-year, with inflation impacting spend patterns. Despite improvements in missed payments, credit card providers need to monitor payment percentages closely.

Il Rapporto sul Mercato delle Carte di Credito del Regno Unito di FICO per febbraio 2024 presenta un quadro variegato riguardo la fiducia dei consumatori e le pressioni finanziarie. Sebbene si sia registrato un aumento della spesa dopo il calo stagionale di gennaio, i pagamenti per saldare i debiti sono diminuiti del 3,6% rispetto all'anno precedente. Il saldo medio delle carte di credito è aumentato del 6,6% su base annua, con l'inflazione che ha influenzato i modelli di spesa. Nonostante i miglioramenti nei pagamenti mancati, i fornitori di carte di credito devono monitorare attentamente le percentuali di pagamento.

El Informe del Mercado de Tarjetas de Crédito del Reino Unido de FICO para febrero de 2024 muestra un panorama mixto en cuanto a la confianza del consumidor y las presiones financieras. Aunque hubo un incremento en los gastos después de la baja post-temporada en enero, los pagos para equilibrar caídas disminuyeron un 3.6% comparado con el año anterior. El saldo promedio de las tarjetas de crédito aumentó un 6.6% interanual, siendo la inflación un factor que afectó los patrones de gasto. A pesar de las mejoras en los pagos perdidos, los proveedores de tarjetas de crédito necesitan monitorear de cerca los porcentajes de pago.

2024년 2월 FICO 영국 신용카드 시장 보고서는 소비자 신뢰도와 재정 압박에 대해 혼합된 그림을 보여줍니다. 1월의 계절적 저조 이후 지출이 증가했지만, 이전 년도에 비해 잔액을 맞추기 위한 지불이 3.6% 감소했습니다. 평균 신용카드 잔액은 연간 6.6% 증가했으며, 인플레이션이 지출 패턴에 영향을 미쳤습니다. 누락된 지불의 개선에도 불구하고 신용카드 제공자는 지불 비율을 면밀히 모니터링해야 합니다.

Le rapport sur le marché des cartes de crédit au Royaume-Uni de FICO pour février 2024 présente une image mitigée concernant la confiance des consommateurs et les pressions financières. Bien qu'il y ait eu une augmentation des dépenses après la baisse saisonnière en janvier, les paiements pour équilibrer les soldes ont diminué de 3,6% par rapport à l'année précédente. Le solde moyen des cartes de crédit a augmenté de 6,6% sur un an, l'inflation influençant les modèles de dépenses. Malgré les améliorations dans les paiements manqués, les fournisseurs de cartes de crédit doivent surveiller de près les pourcentages de paiement.

Der FICO Kreditkartenmarktbericht für das Vereinigte Königreich für Februar 2024 zeigt ein gemischtes Bild bezüglich des Verbrauchervertrauens und der finanziellen Belastungen. Obwohl die Ausgaben nach dem saisonalen Rückgang im Januar gestiegen sind, fielen die Zahlungen zur Kontenausgleichung im Vergleich zum Vorjahr um 3,6%. Der durchschnittliche Kreditkartensaldo stieg im Jahresvergleich um 6,6%, wobei die Inflation die Ausgabemuster beeinflusste. Trotz Verbesserungen bei versäumten Zahlungen müssen Kreditkartenanbieter die Zahlungsquoten genau überwachen.

Positive

Average credit card spend increased by 1.6% to £785 in February 2024 compared to the previous month.

Payments to balance fell by 3.1% from January to February 2024, with 36.5% of outstanding balances paid.

Average credit card balance rose by 6.6% year-on-year to £1,770 in February 2024.

The number of customers missing one or two payments decreased in February 2024 compared to the previous month.

Cash sales as a percentage of total sales decreased by 0.2% in February 2024.

Credit card providers are encouraged by the stabilization in missed payments in February 2024.

Negative

The percentage of payments to balance dropped by 3.6% compared to February 2023.

The average balance on accounts with missed payments is increasing, indicating potential risks.

The trend of customers missing payments has been generally increasing since April 2022.

The average balance of accounts with missed payments is higher than the previous year, pointing to potential financial strain.

The percentage of customers taking out cash on their credit card remains relatively high, impacting overall spending patterns.

Continued signs of financial pressures: credit card balances creep up and payments to balance fall

LONDON--(BUSINESS WIRE)--

The FICO UK Credit Card Market Report for February 2024 presents a mixed picture on consumer confidence and financial pressures. There was an uptick in spending after the usual seasonal dip in January and the number of people missing one and two payments fell. However, payments to balance fell by 3.6% compared to February 2023 and the average balance is higher than the previous month and previous year.

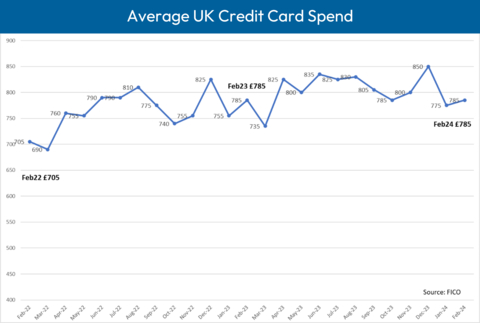

UK credit card spending has started to pick up, after the usual seasonal dip in January, increasing by 1.6% on the previous month to an average of £785, an increase of 0.3% on 2023. (Graphic: FICO)

Highlights

Average spend increased 1.55% over January 2024, reaching an average of £785

With inflation still higher than the same period in 2023, spend remains higher year-on-year

Payments to balance fell by 3.1% from January, with just 36.5% of outstanding balances paid in February and balances increasing 0.1% to £1770

Fewer customers missed one or two payments compared to the previous month, but figures remain higher than 2023

There was a slight year-on-year and month-on-month increase in the number of customers missing three payments

Key Trend Indicators – UK Cards February 2024

Metric

Amount

Month-on-Month Change

Year-on-Year Change

Average UK Credit Card Spend

£785

+1.6%

+0.3%

Average Card Balance

£1,770

+0.1%

+6.6%

Percentage of Payments to Balance

36.47%

-3.1%

-3.6%

Accounts with One Missed Payment

1.5%

-10.9%

+5.5%

Accounts with Two Missed Payments

0.33%

-10.3%

+3.6%

Accounts with Three Missed Payments

0.22%

+1.8%

+2.2%

Average Credit Limit

£5,645

+0.2%

+1.7%

Average Overlimit Spend

£85

0%

-6.5%

Cash Sales as a % of Total Sales

0.86%

-0.2%

-0.1

Source: FICO

FICO Comment

UK credit card spending has started to pick up, after the usual seasonal dip in January, increasing by 1.6% on the previous month to an average of £785, an increase of 0.3% on 2023. Although inflation is now stabilising, inflation does remain higher than last year; spend patterns are, therefore, likely to remain high. Higher inflation rates also continue to impact the average credit card balance, which is now £1,770 – 6.6% higher than February 2023.

Credit card providers will also want to monitor the percentage of the total balance being paid. In February this dropped to 36.5%; a 3.1% decrease compared to January and 3.6% lower year-on-year. This has been trending down since May 2022, with reduced pandemic savings no longer helping to pay down balances as much as they were previously.

Lenders will, however, be encouraged that the pattern of missed payments stabilised in February. The number of customers missing one credit card payment decreased by 10.9% month-on-month, to 1.5%. This measure has been erratic for many months, although it has been trending upwards since April 2022. There is also a more obvious overall upward trend for customers missing two payments; especially for those who have had their credit card for less than five years. However, following the usual Christmas spike, this decreased by 10.3% month-on-month in February to 0.3%, while remaining 3.6% higher than the same month in 2023.

Another important data point is the average balance on accounts with one missed payment. This has increased for the second consecutive month and now stands at an average of £2,255. This is also 5.7% higher than the same period in 2023. For customers missing two payments, this has increased by 4.7% month-on-month to £2,705, with a larger number of accounts and balances missing payments rolling forwards in their delinquency.

Although the number and average balance of one, two and three missed payments is trending upwards, the balance of customers not missing payments has also been trending upwards. The rate of missed payment balances to the overall up-to-date balance has remained flat since the start of 2023; this suggests that collections and limit management risk strategies are effective at controlling customers spending capabilities.

One other measure that credit card providers continue to monitor closely is the percentage of customers taking out cash on their credit card. This continues to decrease; it’s down 2.2% on the previous month, although it remains 3% higher than the previous year, now standing at 3.3%. This has been trending down since September 2023 but if it follows the same trend as 2023, it is likely to stabilise within the next couple of months.

These card performance figures are part of the data shared with subscribers of the FICO® Benchmark Reporting Service. The data sample comes from client reports generated by the FICO® TRIAD® Customer Manager solution in use by some 80% of UK card issuers. For more information on these trends, contact FICO.

About FICO

FICO (NYSE: FICO) powers decisions that help people and businesses around the world prosper. Founded in 1956, the company is a pioneer in the use of predictive analytics and data science to improve operational decisions. FICO holds more than 200 US and foreign patents on technologies that increase profitability, customer satisfaction and growth for businesses in financial services, insurance, telecommunications, health care, retail and many other industries. Using FICO solutions, businesses in more than 100 countries do everything from protecting 4 billion payment cards from fraud, to improving financial inclusion, to increasing supply chain resiliency. The FICO® Score, used by 90% of top US lenders, is the standard measure of consumer credit risk in the US and other countries, improving risk management, credit access and transparency. Learn more at www.fico.com.

FICO and TRIAD are registered trademarks of Fair Isaac Corporation in the U.S. and other countries.

An email has been sent to your address with instructions for changing your password.

There is no user registered with this email.

Sign Up

To create a free account, please fill out the form below.

Thank you for signing up!

A confirmation email has been sent to your email address. Please check your email and follow the instructions in the message to complete the registration process. If you do not receive the email, please check your spam folder or contact us for assistance.

Welcome to our platform!

Oops!

Something went wrong while trying to create your new account. Please try again and if the problem persist, Email Us to receive support.