Ceragon's Board Unanimously Rejects Aviat's Revised Indication of Interest

Ceragon Networks (NASDAQ: CRNT) has rejected Aviat Networks' (NASDAQ: AVNW) revised offer of $3.08 per share, deeming it significantly undervaluing the company. Ceragon's Board, supported by independent advisors, insists the offer fails to reflect their strong business momentum, which includes a 30.3% gross margin and $179 million in bookings for H1 2022. The company urges shareholders to vote against Aviat's proxy card to prevent control of the Board by unqualified nominees, emphasizing they remain open to fair transaction proposals while prioritizing shareholder value.

- None.

- None.

Insights

Analyzing...

Revised IOI Continues to Significantly Undervalue Ceragon and Remains Highly Conditional

Ceragon Urges its Shareholders to Protect Their Investment by Voting the WHITE Proxy Card AGAINST Aviat's Attempt to Take Control of the Board

ROSH HA'AIN, Israel, Aug. 8, 2022 /PRNewswire/ -- Ceragon Networks Ltd. (NASDAQ: CRNT) (the "Company", "Ceragon", "we", "us", or "our") today issued the following letter to shareholders concerning the response of Ceragon's Board of Directors (the "Board") to the revised unsolicited, highly conditional, non-binding indication of interest from Aviat Networks, Inc. (NASDAQ: AVNW), a competitor of Ceragon.

The letter to shareholders and other supplemental information will be posted to Ceragon's investor relations website here.

The full text of the letter to shareholders follows:

8 August 2022

Dear Fellow Shareholder,

A few days ago, Ceragon received a revised indication of interest ("Revised IOI") from its competitor, Aviat Networks, Inc. ("Aviat"), to acquire Ceragon at a price of

To be clear, Ceragon is focused on maximizing value for all shareholders and we remain open to exploring a transaction with Aviat or anyone else, but only if such combination delivers full, fair and certain value to Ceragon shareholders. We have met with Aviat multiple times (including with directors from our respective boards) to explore a transaction. However, Aviat's Revised IOI continues to fall far short.

Aviat's slightly improved Revised IOI continues to significantly undervalue the Company on a variety of financial metrics – its implied multiples are below precedent transaction and public company trading multiples, and the indicative price is well below every research analyst price target. It also does not take into account the Company's strong business momentum, as reflected in our growing backlog, market share gains and gross margin enhancement.

Aviat has launched its proxy campaign to advance its low-ball, highly conditional bid. They are attempting to replace our highly qualified directors with their unqualified, hand-picked nominees to take control of the Board and be entrusted with leading negotiations on your behalf for a potential transaction with Aviat. We urge shareholders to protect their investment by voting only on the WHITE proxy card AGAINST Aviat's attempt to take control of the Board and ignoring Aviat's gold proxy card.

Ceragon Has Strong Business Momentum that We Expect Will Create Shareholder Value

Last week, Ceragon announced its second quarter financial results. We are demonstrating continued momentum across a variety of key financial metrics in growing market share, revenue and margins, including:

- #1 global provider of best-of-breed solutions, now with

25% market share $179 million of bookings in 1H'22 driven by the continued rollout of 5G across the globe$39 million of North American bookings (Aviat's backyard) in 1H'22, now Ceragon's largest market at26% of total bookings in 2Q'22 (tied with India)30.3% gross margin in 2Q'22, reflecting a 280 basis point increase versus 1Q'22, driven by a mix shift to higher software sales, actions taken to reduce shipping costs and other measures taken to reduce production costs

Don't just take our word for it – independent third-party research analysts agree1:

- "We're encouraged by Ceragon's steady execution and gross margin improvement, and see potential for stronger results/upside as supply chain/shipping constraints ease and newer demand drivers ramp" – Oppenheimer (1 August 2022)

- "We expect revenues to accelerate as supply chains improve enabling Ceragon to start to ship to its massive backlog and new orders should remain healthy as the new products and 5G demand start to take hold. Based on this, we think revenue growth will accelerate, profitability will improve, and the multiple will appreciate" – Needham (1 August 2022)

- "We continue to believe that positive mix shift to 5G bookings will represent a key driver for both top line growth as well as margin expansion opportunity for Ceragon longer term" – Aegis (1 August 2022)

While there is more work to be done, we are excited about the progress we are making and our outlook for the future. With the strength of our core business, combined with our new growth initiatives and supply chain normalization, we expect to drive revenue of

Aviat's Revised IOI Continues to Significantly Undervalue Ceragon and Remains Highly Conditional

Our Board has unanimously concluded, with the assistance of independent financial and legal advisors, that the slightly improved Revised IOI of

Many of our shareholders that we have spoken with, including our largest shareholder, believe that Aviat's Revised IOI is well below the value of Ceragon.

Aviat has also failed to demonstrate that they can provide deal certainty and has a track record of abandoning late-stage negotiations:

- On multiple occasions, including with Ceragon as well as another company with which our directors are involved, Aviat abandoned negotiations after the companies had exchanged confidential and sensitive information and had drafted a near-final agreement

- When we last met with Aviat in June, they had proposed a reverse termination fee2 that was well below market precedents, particularly as compared to transactions involving close competitors

- We communicated that we needed appropriate deal protections to ensure Ceragon's shareholders would be protected in the event Aviat were to try to walk away from an agreement, but we indicated that we would be willing to further negotiate deal protection matters as we continued our discussions

- Aviat also agreed at that June meeting to provide a due diligence list – instead of providing that list and continuing negotiations, Aviat responded with a public hostile campaign without warning six days later

Given their low-ball Revised IOI and unwillingness to provide deal certainty, it is clear why Aviat's nominees should not be put in charge of negotiating a deal with Aviat on behalf of Ceragon shareholders.

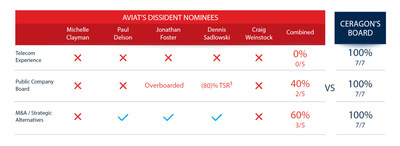

Aviat's Nominees Are Unqualified to Serve Ceragon Shareholders

Aviat is proposing that Ceragon's shareholders approve director nominees hand-picked by Aviat to control Ceragon's Board with little regard to Ceragon's business. Their slate of director candidates does not satisfy the criteria established by our Nomination Committee or that an objective third-party would deem relevant for a telecom company. None of Aviat's nominees have telecom experience and all of Aviat's nominees have either no or problematic board experience.

Given that Aviat's nominees do not have the requisite expertise to lead a sophisticated, market-leading telecom company, we can only infer that they were nominated solely to force a low-ball sale to Aviat. This is particularly troubling because if Aviat's nominees take control of the Ceragon Board, Aviat can reduce their price (again), execute a transaction that allows Aviat to walk away without serious consequence, or destroy Ceragon from inside the Boardroom.

This further proves that electing Aviat's director nominees and putting them in charge of deal negotiations for Ceragon is not in the interest of Ceragon shareholders.

Aviat has Also Launched a Campaign that Violates our Articles and Without Legal Basis

Aviat has launched its proxy fight in a way that violates our shareholder-approved Articles, which only allow the appointment of up to three director nominees rather than the five Aviat proposed at the upcoming Extraordinary General Meeting of shareholders ("EGM") – and only in the event that all three Ceragon directors that they propose to remove are indeed removed. In support of their proxy fight, Aviat has also issued a proxy statement and a gold proxy card that have no legal basis. Please disregard any gold proxy card that you may receive from Aviat.

Ceragon's Directors are Highly Qualified and Proven Value Creators with Decades of Experience Supporting M&A Transactions

Ceragon's Board is singularly focused on the best interests of the Company and on maximizing value for Ceragon's shareholders. Our Board is comprised of leaders with substantial telecom and public company board experience. In addition, our Board continues to refresh itself, including the addition of three new independent directors at last year's AGM.

Furthermore, the attacks on our directors that Aviat has specifically targeted have no merit. How is the association with our Chairman, Zohar Zisapel, one of the prominent leaders of Israeli telecom with substantial experience in creating value for shareholders, a negative? His track record of founding and successfully leading numerous companies has significantly benefited our Board and company.

Moreover, our directors have served as executives and directors of many companies that have created meaningful shareholder value, and have a robust track record of supporting M&A that deliver fair value to shareholders:

- Zohar Zisapel: One of the prominent leaders of Israeli telecom with substantial experience in creating value for shareholders (>

100% TSRs at Amdocs and Silicom) - Ira Palti: Has successfully helped transition CEO role to Doron

- Yael Langer: Oversaw sales of companies on 5 separate occasions (Radlan, RND, Sanrad, RiT, Radvision);

481% TSR while on the board of Radware - David Ripstein:

311% TSR while in role at Radcom - Ilan Rosen:

39% during his tenure at VocalTec, culminating in the merger with Tdsoft - Shlomo Liran:

118% TSR at Maytronics,68% TSR at Minrav - Rami Hadar: Extensive M&A experience as the co-founder, CEO and/or C-level exec of three different Telecom companies

Indeed, our Board has been open to exploring a potential transaction with Aviat, having met with its representatives many times since 2017. We remain willing to consider a potential combination with Aviat, but only if such combination delivers full, fair and certain value to Ceragon shareholders. We will not, however, sell the Company at an inadequate price or enter into a sale transaction that has a high degree of uncertainty.

Our Commitment to Ceragon Shareholders

We have spoken with many of our shareholders, and appreciate the valuable input and support received from them to date and look forward to continued dialogue. Our Board continues to be focused on maximizing the value of the Company for our shareholders. We have substantial momentum in our business, and we remain open to exploring a transaction with Aviat (or anyone else) if they propose a full and fair transaction for Ceragon shareholders. However, we sincerely believe Aviat's highly conditional and low-ball Revised IOI is not in the best interest of Ceragon's shareholders.

We urge Ceragon's shareholders to protect their investment by voting the WHITE proxy card "AGAINST" Aviat's attempt to take control of the Board and ignoring Aviat's gold proxy card.

If you have any questions or require any assistance with voting your shares, please contact the Company's proxy solicitor, Morrow Sodali LLC at 800-662-5200 (toll-free in North America) or +1 203-658-9400 or email at CRNT@info.morrowsodali.com.

Best regards,

The Ceragon Board

About Ceragon Networks

Ceragon Networks Ltd. (NASDAQ: CRNT) is the global innovator and leading solutions provider of 5G wireless transport. We help operators and other service providers worldwide increase operational efficiency and enhance end customers' quality of experience with innovative wireless backhaul and fronthaul solutions. Our customers include service providers, public safety organizations, government agencies and utility companies, which use our solutions to deliver 5G & 4G broadband wireless connectivity, mission-critical multimedia services, stabilized communications, and other applications at high reliability and speed.

Ceragon's unique multicore technology and disaggregated approach to wireless transport provides highly reliable, fast to deploy, high-capacity wireless transport for 5G and 4G networks with minimal use of spectrum, power, real estate, and labor resources. It enables increased productivity, as well as simple and quick network modernization, positioning Ceragon as a leading solutions provider for the 5G era. We deliver a complete portfolio of turnkey end-to-end AI-based managed and professional services that ensure efficient network rollout and optimization to achieve the highest value for our customers. Our solutions are deployed by more than 400 service providers, as well as more than 800 private network owners, in more than 150 countries. For more information please visit: www.ceragon.com.

Ceragon Networks® and FibeAir® are registered trademarks of Ceragon Networks Ltd. in the United States and other countries. CERAGON ® is a trademark of Ceragon Networks Ltd., registered in various countries. Other names mentioned are owned by their respective holders.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This document contains statements that constitute "forward-looking statements" within the meaning of the Securities Act of 1933, as amended and the Securities Exchange Act of 1934, as amended, and the safe-harbor provisions of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are based on the current beliefs, expectations and assumptions of Ceragon's management about Ceragon's business, financial condition, results of operations, micro and macro market trends and other issues addressed or reflected therein. Examples of forward-looking statements include, but are not limited to, statements regarding: projections of demand, revenues, net income, gross margin, capital expenditures and liquidity, competitive pressures, order timing, supply chain and shipping, components availability, growth prospects, product development, financial resources, cost savings and other financial and market matters. You may identify these and other forward-looking statements by the use of words such as "may", "plans", "anticipates", "believes", "estimates", "targets", "expects", "intends", "potential" or the negative of such terms, or other comparable terminology, although not all forward-looking statements contain these identifying words.

Although we believe that the projections reflected in such forward-looking statements are based upon reasonable assumptions, we can give no assurance that our expectations will be obtained or that any deviations therefrom will not be material. Such forward-looking statements involve known and unknown risks and uncertainties that may cause Ceragon's future results or performance to differ materially from those anticipated, expressed or implied by such forward-looking statements. These risks and uncertainties include, but are not limited to, any ongoing actions taken and future actions that may be taken by Aviat Networks Inc. or other stockholders or others; the continuing impact of the components shortage due to the global shortage in semiconductors, chipsets, components and other commodities, on our supply chain, manufacturing capacity and ability to timely deliver our products, which have caused, and could continue to cause delays in deliveries of our products and in the deployment of projects by our customers, risk of penalties and orders cancellation created thereby, as well as profit erosion due to constant price increase, payment of expedite fees and costs of inventory pre-ordering and procurement acceleration of such inventory, and the risk of becoming a deadstock if not consumed; the continued effect of the global increase in shipping costs and decrease in shipping slots availability on us, our supply chain and customers, which have resulted, and may continue to result in, price erosion, late deliveries and the risk of penalties and orders cancellation due to late deliveries; the impact of the transition to 5G technologies on our revenues if such transition is developed differently than we anticipated; the risks relating to the concentration of a major portion of our business on large mobile operators around the world from which we derive a significant portion of our ordering, that due to their relative effect on the overall ordering coupled with inconsistent ordering pattern and volume of business directed to us, creates high volatility with respect to our financial results and results of operations; the effect of the competition from other wireless transport equipment providers and from other communication solutions that compete with our high-capacity point-to-point wireless products; the continued effect of the COVID-19 pandemic on the global economy and markets and on us and on the markets in which we operate and our and our customers, providers, business partners and contractors business and operations; the risks relating to increased breaches of network or information technology security along with increase in cyber-attack activities, growing cyber-crime threats, and changes in privacy and data protection laws, that could have an adverse effect on our business; risks associated with any failure to meet our product development timetable, including delay in the commercialization of our new chipset; imposition of additional sanctions and global trade limitations in connection with Russia's invasion to Ukraine, the effects of general economic conditions and trends on the global and local markets in which we operate and such other risks, uncertainties and other factors that could affect our results, as further detailed in Ceragon's most recent Annual Report on Form 20-F and in Ceragon's other filings with the Securities and Exchange Commission.

Such forward-looking statements, including the risks, uncertainties and other factors that could affect our results, represent our views only as of the date they are made and should not be relied upon as representing our views as of any subsequent date. Such forward-looking statements do not purport to be predictions of future events or results and there can be no assurance that it will prove to be accurate. Ceragon may elect to update these forward-looking statements at some point in the future but the company specifically disclaims any obligation to do so except as may be required by law.

Ceragon's public filings are available on the Securities and Exchange Commission's website at www.sec.gov and may also be obtained from Ceragon's website at www.ceragon.com.

ADDITIONAL INFORMATION

Ceragon has filed a definitive proxy statement and WHITE proxy card with the U.S. Securities and Exchange Commission (the "SEC") in connection with its solicitation of proxies for the 2022 Extraordinary General Meeting of Ceragon Shareholders (the "2022 Extraordinary General Meeting"). CERAGON SHAREHOLDERS ARE STRONGLY ENCOURAGED TO READ THE DEFINITIVE PROXY STATEMENT (AND ANY AMENDMENTS AND SUPPLEMENTS THERETO) AND ACCOMPANYING WHITE PROXY CARD AS THEY CONTAIN IMPORTANT INFORMATION. Shareholders may obtain the proxy statement, any amendments or supplements to the proxy statement and other documents as and when filed by Ceragon with the SEC without charge from the SEC's website at www.sec.gov.

Ceragon Investor & Media Contact:

Maya Lustig

Ceragon Networks

Tel. +972-54-677-8100

mayal@ceragon.com

1 Permission to Use Quotes Neither Sought Nor Obtained

2 A standard feature in similar transactions designed to protect selling shareholders from the acquiror simply walking away from a transaction after receiving access to confidential information

3 TSR relative to S&P 500 over the period between May 2016 and July 2020, including reinvestment of dividends

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/ceragons-board-unanimously-rejects-aviats-revised-indication-of-interest-301601382.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/ceragons-board-unanimously-rejects-aviats-revised-indication-of-interest-301601382.html

SOURCE Ceragon Networks Ltd.