S&P Global Market Intelligence's latest quarterly community bank report says liquidity pressures will cause community banks to record notably higher funding costs in 2023

S&P Global Market Intelligence's latest report on community banking indicates that rising funding costs and liquidity pressures will hinder net interest margin growth in 2023. The report highlights that community banks are expected to rely increasingly on wholesale funding and certificates of deposit, leading to higher deposit costs. Notably, the projected deposit beta for 2023 is 28%, significantly up from 10% in 2022. Additionally, net charge-offs are anticipated to rise to 0.19% of average loans, and provisions are set to increase to 11.8% of net revenue. The findings suggest a challenging financial landscape for community banks moving forward.

- Community banks experienced strong margins in 2022 due to healthy loan growth and higher interest rates.

- Funding costs are expected to rise significantly in 2023 due to increased reliance on more expensive funding sources.

- Projected deposit beta is expected to increase to 28% in 2023, indicating higher costs passed to depositors.

- Net charge-offs are anticipated to increase to 0.19% of average loans, up from historically low levels.

- Provisions for losses are projected to rise to 11.8% of net revenue, compared to just 6.4% in 2022.

Developed by the company's

"Healthy loan growth, higher interest rates and modest increases in deposit costs have resulted in far stronger community bank margins in 2022. However, liquidity pressures have begun to emerge and will likely cause community banks to record notably higher funding costs in 2023 as institutions increase their reliance on more expensive wholesale funding and certificates of deposit (CDs)," said

Key highlights from the report include:

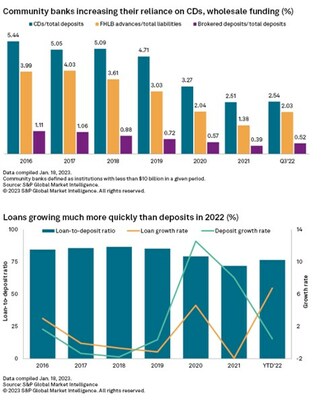

- CD balances and borrowings from the Federal Home Loan Banks (FHLB) are expected to steadily grow in 2023 as community banks seek to fulfill their liquidity needs, translating into notably higher deposit costs for the group. Earning-asset yields will also reprice higher but will fail to expand at the same rate as funding costs in 2023, causing margin expansion to stall for community banks.

- Community banks are projected to record a deposit beta, or the percentage change that banks pass on to all depositors, of

10% for the full year 2022, up from6% through the first nine months of 2022. We expect the group to record a beta of28% in 2023, leading to a cumulative beta of22% by the end of 2023. - Net charge-offs are expected to jump in 2023 off a historically low base to

0.19% of average loans. - Provisions are expected to rise to

11.8% of net revenue in 2023, up from just6.4% in 2022. From 2013 to 2019, community banks' provisions equated to9.6% of net revenue on average.

To request a copy of the Liquidity pressures put funding in the crosshairs at community banks, please contact pressinquiries.mi@spglobal.com.

Scope and methodology

The outlook is based on management commentary, discussions with industry sources, regression analysis, and asset and liability repricing data disclosed in banks' quarterly call reports. While taking into consideration historical growth rates, the analysis often excludes the significant volatility experienced in the years around the credit crisis.

The outlook is subject to change, perhaps materially, based on adjustments to the consensus expectations for interest rates, unemployment and economic growth. The projections can be updated or revised at any time as developments warrant, particularly when material changes occur.

About

At

Media Contact

+1 781-301-9311

katherine.smith@spglobal.com

![]()

![]() View original content to download multimedia:https://www.prnewswire.com/news-releases/sp-global-market-intelligences-latest-quarterly-community-bank-report-says-liquidity-pressures-will-cause-community-banks-to-record-notably-higher-funding-costs-in-2023-301732482.html

View original content to download multimedia:https://www.prnewswire.com/news-releases/sp-global-market-intelligences-latest-quarterly-community-bank-report-says-liquidity-pressures-will-cause-community-banks-to-record-notably-higher-funding-costs-in-2023-301732482.html

SOURCE