Skeena Establishes 21A West Zone Continuity at Eskay Creek with 2.27 g/t AuEq over 50.00 metres

Skeena Resources Limited (TSX:SKE)(NYSE:SKE) released promising drilling results from its 2022 exploration programs at the Eskay Creek gold-silver Project in British Columbia. Key findings include:

- Drill hole SK-22-1093 intersected 47.50 g/t Au and 73.4 g/t Ag over 12.12 m.

- Hole SK-22-1031 showed 2.21 g/t Au and 4.6 g/t Ag over 50.00 m.

- New mineralization discovered in the 21A West Zone is set to be included in future resource updates.

- Ongoing drilling aims to increase open pittable resources and convert to Probable Reserves.

- High-grade gold and silver mineralization discovered in drill holes SK-22-1093 and SK-22-1031.

- Expansion of the 21A West Zone leads to anticipated increases in resource estimates.

- Continued drilling campaign with six rigs focused on growing and infilling mineralized zones.

- None.

Insights

Analyzing...

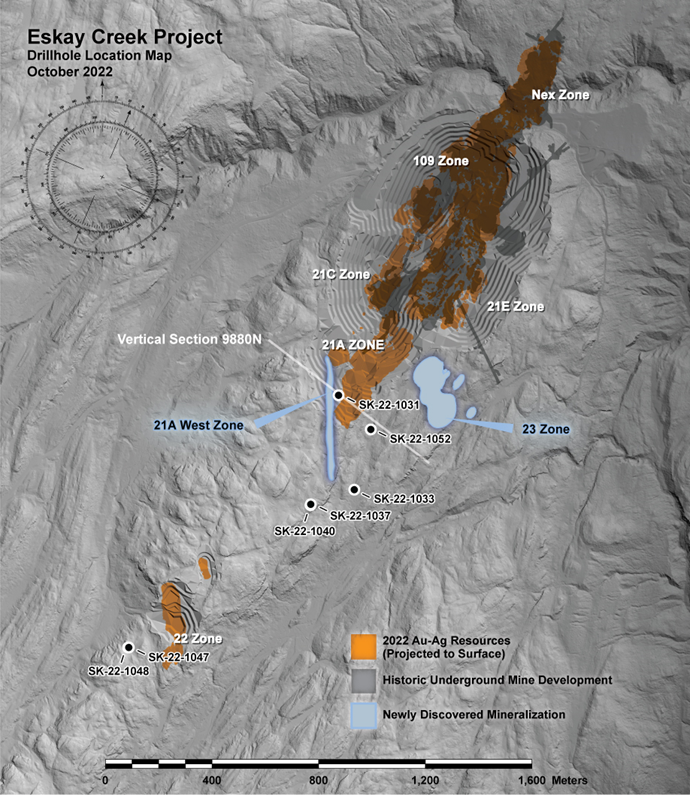

VANCOUVER, BC / ACCESSWIRE / October 18, 2022 / Skeena Resources Limited (TSX:SKE)(NYSE:SKE) ("Skeena" or the "Company") is pleased to announce drilling results from the 2022 regional and near mine exploration programs at the Eskay Creek gold-silver Project ("Eskay Creek" or the "Project") in the Golden Triangle of British Columbia. Analytical results and reference images from the recently completed drill holes are presented at the end of this release as well as on the Company's website. Additional results will be reported once available.

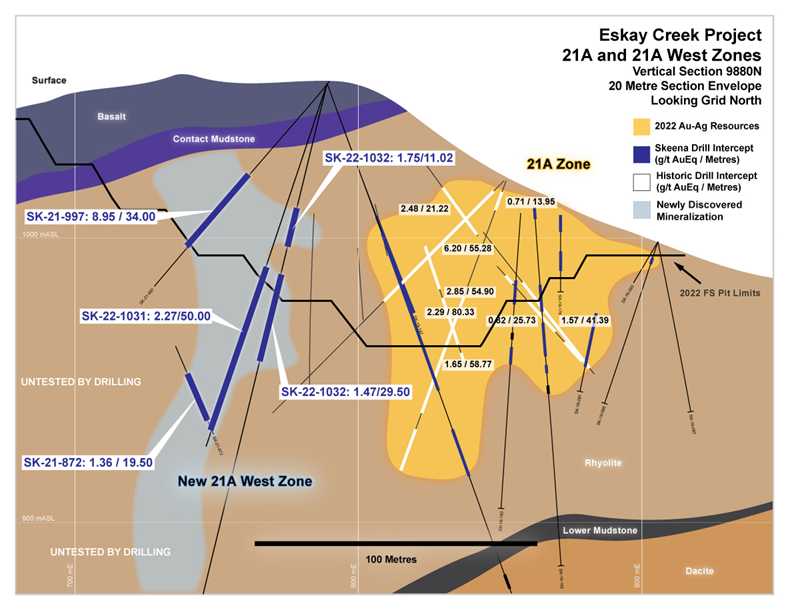

21A West Zone Continuity Develops

Building upon the in-pit mineralization discovered in 2021 by drill hole SK-21-997 which intersected high-tenor gold mineralization averaging 8.78 g/t Au, 13 g/t Ag (8.95 g/t AuEq) over 34.00 m and recently expanded by 2022 drill hole SK-22-1093 47.50 g/t Au, 73.4 g/t Ag (48.48 g/t AuEq) over 12.12 m, drillhole SK-22-1031 has intersected 2.21 g/t Au, 4.6 g/t Ag (2.27 g/t AuEq) over 50.00 m. Due to the lack of historical drilling in this portion of the 21A Zone, the area was considered as barren waste rock for both the 2022 Resource Estimate and Feasibility Study. This recently discovered feeder-style mineralization occurs within the footwall Rhyolite sequence immediately below the Contact Mudstone and will be incorporated into the future resource and economic updates for the Eskay Creek Project. The limited drilling to date in the 21A West Zone indicates that precious metal tenor typically increases vertically up stratigraphy with closer proximity to the Contact Mudstone.

The ongoing 2022 exploration program has not yet fully defined the extents of the 21A West Zone. As is the case with similar feeder style mineralization in other portions of the Eskay Creek deposit, zone geometry is well established and hole to hole continuity of mineralization is very predictable to date. The new intersection in hole SK-22-1031 highlighting 2.27 g/t AuEq over 50.00 m is 75 metres south along strike of the previously reported 48.48 g/t AuEq over 12.12 m in hole SK-22-1093.

23 Zone Expanded to South

Situated 500 metres south of the currently defined mineralization in the 23 Zone, recently competed exploratory drill hole SK-22-1040 has intersected 0.78 g/t Au, 0.8 g/t Ag (0.79 g/t AuEq) over 95.75 m hosted entirely within the dacite package and Even Lower Mudstone, which is consistent with the 23 Zone mineralization. This new discovery begins only 25 metres below surface and is open for expansion.

Exploration Status Update

The Company is currently performing expansion and infill drilling with six helicopter supported drill rigs at the Eskay Creek Project. The focus is to expedite not only the organic growth of open pittable resources in the 23, 21A West and 22 Zones, but to infill these new zones for ultimate conversion to Probable Reserves.

About Skeena

Skeena Resources Limited is a Canadian mining exploration and development company focused on revitalizing the past-producing Eskay Creek gold-silver mine located in Tahltan Territory in the Golden Triangle of northwest British Columbia, Canada. The Company released a Feasibility Study for Eskay Creek in September 2022 which highlights an open-pit average grade of 4.00 g/t AuEq, an after-tax NPV5% of C

On behalf of the Board of Directors of Skeena Resources Limited,

Walter Coles Jr.

CEO & Director

Contact Information

Investor Inquiries: info@skeenaresources.com

Office Phone: +1 604 684 8725

Company Website: www.skeenaresources.com

Qualified Persons

Exploration activities at the Eskay Creek Project are administered on site by the Company's Exploration Managers, Raegan Markel, P.Geo. and Director of Exploration, Adrian Newton P.Geo. In accordance with National Instrument 43-101 Standards of Disclosure for Mineral Projects, Paul Geddes, P.Geo. Senior Vice President Exploration and Resource Development, is the Qualified Person for the Company and has prepared, validated and approved the technical and scientific content of this news release. The Company strictly adheres to CIM Best Practices Guidelines in conducting, documenting, and reporting the exploration activities on its projects.

Quality Assurance - Quality Control

Once received from the drill and processed, all drill core samples are sawn in half, labelled and bagged. The remaining drill core is subsequently securely stored on site. Numbered security tags are applied to lab shipments for chain of custody requirements. The Company inserts quality control (QC) samples at regular intervals in the sample stream, including blanks and reference materials with all sample shipments to monitor laboratory performance. The QAQC program was designed and approved by Lynda Bloom, P.Geo. of Analytical Solutions Ltd., and is overseen by the Company's Qualified Person, Paul Geddes, P.Geo, Vice President Exploration and Resource Development.

Drill core samples are submitted to ALS Geochemistry's analytical facility in North Vancouver, British Columbia for preparation and analysis. The ALS facility is accredited to the ISO/IEC 17025 standard for gold assays and all analytical methods include quality control materials at set frequencies with established data acceptance criteria. The entire sample is crushed and 1 kg is pulverized. Analysis for gold is by 50 g fire assay fusion with atomic absorption (AAS) finish with a lower limit of 0.01 ppm and upper limit of 100 ppm. Samples with gold assays greater than 100 ppm are re-analyzed using a 50 g fire assay fusion with gravimetric finish. Analysis for silver is by 50 g fire assay fusion with gravimetric finish with a lower limit of 5ppm and upper limit of 10,000 ppm. Samples with silver assays greater than 10,000 ppm are re-analyzed using a gravimetric silver concentrate method. A selected number of samples are also analyzed using a 48 multi-element geochemical package by a 4-acid digestion, followed by Inductively Coupled Plasma Atomic Emission Spectroscopy (ICP-AES) and Inductively Coupled Plasma Mass Spectroscopy (ICP-MS) and also for mercury using an aqua regia digest with Inductively Coupled Plasma Atomic Emission Spectroscopy (ICP-AES) finish. Samples with sulfur reporting greater than

Cautionary note regarding forward-looking statements

Certain statements and information contained or incorporated by reference in this news release constitute "forward-looking information" and "forward-looking statements" within the meaning of applicable Canadian and United States securities legislation (collectively, "forward-looking statements"). These statements relate to future events or our future performance. The use of words such as "anticipates", "believes", "proposes", "contemplates", "generates", "targets", "is projected", "is planned", "considers", "estimates", "expects", "is expected", "potential" and similar expressions, or statements that certain actions, events or results "may", "might", "will", "could", or "would" be taken, achieved, or occur, may identify forward-looking statements. All statements other than statements of historical fact are forward-looking statements. Specific forward-looking statements contained herein include, but are not limited to, statements regarding the results of the Feasibility Study, processing capacity of the mine, anticipated mine life, probable reserves, estimated project capital and operating costs, sustaining costs, results of test work and studies, planned environmental assessments, the future price of metals, metal concentrate, and future exploration and development. Such forward-looking statements are based on material factors and/or assumptions which include, but are not limited to, the estimation of mineral resources and reserves, the realization of resource and reserve estimates, metal prices, taxation, the estimation, timing and amount of future exploration and development, capital and operating costs, the availability of financing, the receipt of regulatory approvals, environmental risks, title disputes and the assumptions set forth herein and in the Company's MD&A for the year ended December 31, 2021, its most recently filed interim MD&A, and the Company's Annual Information Form ("AIF") dated March 31, 2022. Such forward-looking statements represent the Company's management expectations, estimates and projections regarding future events or circumstances on the date the statements are made, and are necessarily based on several estimates and assumptions that, while considered reasonable by the Company as of the date hereof, are not guarantees of future performance. Actual events and results may differ materially from those described herein, and are subject to significant operational, business, economic, and regulatory risks and uncertainties. The risks and uncertainties that may affect the forward-looking statements in this news release include, among others: the inherent risks involved in exploration and development of mineral properties, including permitting and other government approvals; changes in economic conditions, including changes in the price of gold and other key variables; changes in mine plans and other factors, including accidents, equipment breakdown, bad weather and other project execution delays, many of which are beyond the control of the Company; environmental risks and unanticipated reclamation expenses; and other risk factors identified in the Company's MD&A for the year ended December 31, 2021, its most recently filed interim MD&A, the AIF dated March 31, 2022, and in the Company's other periodic filings with securities and regulatory authorities in Canada and the United States that are available on SEDAR at www.sedar.com or on EDGAR at www.sec.gov.

Readers should not place undue reliance on such forward-looking statements. Any forward-looking statement speaks only as of the date on which it is made and Company does not undertake any obligations to update and/or revise any forward-looking statements except as required by applicable securities laws.

Cautionary note to U.S. Investors concerning estimates of mineral reserves and mineral resources

Skeena's mineral reserves and mineral resources included or incorporated by reference herein have been estimated in accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects ("NI 43-101") as required by Canadian securities regulatory authorities, which differ from the requirements of U.S. securities laws. The terms "mineral reserve", "proven mineral reserve", "probable mineral reserve", "mineral resource", "measured mineral resource", "indicated mineral resource" and "inferred mineral resource" are Canadian mining terms as defined in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum ("CIM") "CIM Definition Standards - For Mineral Resources and Mineral Reserves" adopted by the CIM Council (as amended, the "CIM Definition Standards"). These standards differ significantly from the mineral property disclosure requirements of the U.S. Securities and Exchange Commission in Regulation S-K Subpart 1300 (the "SEC Modernization Rules"). Skeena is not currently subject to the SEC Modernization Rules. Accordingly, Skeena's disclosure of mineralization and other technical information may differ significantly from the information that would be disclosed had Skeena prepared the information under the standards adopted under the SEC Modernization Rules.

In addition, investors are cautioned not to assume that any part or all of Skeena's mineral resources constitute or will be converted into reserves. These terms have a great amount of uncertainty as to their economic and legal feasibility. Accordingly, investors are cautioned not to assume that any "measured", "indicated", or "inferred" mineral resources that Skeena reports are or will be economically or legally mineable. Further, "inferred mineral resources" have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. It cannot be assumed that all or any part of an "inferred mineral resource" will ever be upgraded to a higher category. Under Canadian securities laws, estimates of "inferred mineral resources" may not form the basis of feasibility or prefeasibility studies, except in rare cases where permitted under NI 43-101.

For these reasons, the mineral reserve and mineral resource estimates and related information presented herein may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the U.S. federal securities laws and the rules and regulations thereunder.

Table 1: Eskay Creek Project 2022 Exploratory Drilling Campaign Length-Weighted Drill Hole Composites:

| Hole-ID | From (m) | To (m) | Sample Length (m) | Au (g/t) | Ag (g/t) | AuEq (g/t) |

|---|---|---|---|---|---|---|

SK-22-1031 | 10.50 | 11.90 | 1.40 | 0.36 | 17.9 | 0.56 |

SK-22-1031 | 63.50 | 68.00 | 4.50 | 0.28 | 11.7 | 0.41 |

SK-22-1031 | 78.00 | 128.00 | 50.00 | 2.21 | 4.6 | 2.27 |

SK-22-1031 | 137.00 | 162.00 | 25.00 | 0.43 | 16.7 | 0.62 |

SK-22-1031 | 187.50 | 190.50 | 3.00 | 0.30 | 1.4 | 0.32 |

SK-22-1033 | 16.00 | 17.04 | 1.04 | 0.39 | 8.6 | 0.49 |

SK-22-1033 | 45.68 | 56.83 | 11.15 | 0.27 | 6.4 | 0.34 |

SK-22-1033 | 69.72 | 77.50 | 7.78 | 0.39 | 6.4 | 0.47 |

SK-22-1033 | 85.10 | 89.50 | 4.40 | 1.81 | 27.7 | 2.12 |

SK-22-1033 | 108.62 | 116.00 | 7.38 | 0.42 | 1.7 | 0.44 |

SK-22-1033 | 128.00 | 129.50 | 1.50 | 0.68 | 0.5 | 0.68 |

SK-22-1037 | 60.42 | 61.50 | 1.08 | 0.47 | 1.0 | 0.48 |

SK-22-1037 | 67.15 | 80.50 | 13.35 | 0.47 | 2.7 | 0.50 |

SK-22-1037 | 93.50 | 100.50 | 7.00 | 0.30 | 3.5 | 0.34 |

SK-22-1037 | 107.73 | 138.00 | 30.27 | 0.45 | 1.0 | 0.45 |

SK-22-1037 | 145.00 | 160.00 | 15.00 | 0.37 | 0.8 | 0.37 |

SK-22-1037 | 167.00 | 177.50 | 10.50 | 0.35 | 0.6 | 0.35 |

SK-22-1037 | 219.00 | 226.50 | 7.50 | 0.30 | 17.2 | 0.49 |

SK-22-1037 | 251.00 | 252.00 | 1.00 | 0.30 | 0.5 | 0.30 |

SK-22-1040 | 46.15 | 141.90 | 95.75 | 0.78 | 0.8 | 0.79 |

SK-22-1040 | 180.50 | 183.50 | 3.00 | 0.33 | 0.3 | 0.33 |

SK-22-1040 | 203.00 | 204.00 | 1.00 | 0.35 | 0.4 | 0.35 |

SK-22-1045 | PENDING | |||||

SK-22-1046 | PENDING | |||||

SK-22-1047 | 82.00 | 82.80 | 0.80 | 0.40 | 5.7 | 0.46 |

SK-22-1047 | 155.50 | 195.06 | 39.56 | 0.90 | 1.0 | 0.91 |

SK-22-1047 | 209.50 | 211.00 | 1.50 | 0.31 | 0.3 | 0.31 |

SK-22-1047 | 232.00 | 238.00 | 6.00 | 0.45 | 0.4 | 0.45 |

SK-22-1047 | 244.00 | 248.50 | 4.50 | 0.88 | 0.9 | 0.89 |

SK-22-1047 | 289.00 | 327.00 | 38.00 | 0.32 | 9.3 | 0.43 |

SK-22-1047 | 337.50 | 343.50 | 6.00 | 0.57 | 4.1 | 0.61 |

SK-22-1048 | 100.00 | 100.97 | 0.97 | 0.88 | 14.5 | 1.04 |

SK-22-1048 | 140.00 | 141.30 | 1.30 | 0.84 | 9.0 | 0.94 |

SK-22-1048 | 257.50 | 269.00 | 11.50 | 0.26 | 16.7 | 0.44 |

SK-22-1048 | 279.50 | 298.00 | 18.50 | 0.48 | 43.1 | 0.96 |

SK-22-1048 | 334.50 | 335.50 | 1.00 | 0.27 | 6.7 | 0.35 |

SK-22-1048 | 341.92 | 343.10 | 1.18 | 0.29 | 3.4 | 0.33 |

SK-22-1048 | 355.00 | 360.21 | 5.21 | 2.29 | 135.8 | 3.82 |

INCLUDING | 359.00 | 359.50 | 0.50 | 12.25 | 1020.0 | 23.71 |

SK-22-1049 | PENDING | |||||

SK-22-1052 | 67.50 | 75.00 | 7.50 | 1.11 | 4.3 | 1.15 |

SK-22-1052 | 92.70 | 147.00 | 54.30 | 0.35 | 6.2 | 0.42 |

SK-22-1052 | 156.78 | 193.70 | 36.92 | 0.35 | 1.6 | 0.37 |

SK-22-1052 | 205.25 | 205.85 | 0.60 | 1.09 | 9.6 | 1.20 |

SK-22-1052 | 213.10 | 213.66 | 0.56 | 0.29 | 0.9 | 0.30 |

Gold Equivalent (AuEq) calculated via the formula: Au (g/t) + [Ag (g/t) / 90]. True widths and zone geometries cannot be definitively determined at this time. Grade-capping of individual assays has not been applied to the Au and Ag assays informing the length-weighted AuEq composites. Metallurgical processing recoveries have not been applied to the AuEq calculation and are taken at

Table 2: Mine Grid Drill Hole Locations and Orientations:

| Hole-ID | Easting (m) | Northing (m) | Elevation (m) | Length (m) | Azimuth (°) | Dip (°) |

|---|---|---|---|---|---|---|

SK-22-1031 | 9787.5 | 9878.3 | 1056.8 | 275.0 | 297.0 | -70.0 |

SK-22-1033 | 9986.7 | 9579.4 | 1013.0 | 150.6 | 106.6 | -49.9 |

SK-22-1037 | 9860.4 | 9462.3 | 1078.7 | 252.0 | 57.2 | -54.9 |

SK-22-1040 | 9861.0 | 9459.1 | 1078.3 | 205.0 | 142.4 | -50.0 |

SK-22-1047 | 9458.5 | 8691.9 | 1081.0 | 375.8 | 62.3 | -50.3 |

SK-22-1048 | 9456.5 | 8691.1 | 1081.3 | 401.4 | 70.4 | -63.3 |

SK-22-1052 | 9950.4 | 9811.1 | 984.8 | 220.5 | 129.2 | -59.9 |

SOURCE: Skeena Resources Limited

View source version on accesswire.com:

https://www.accesswire.com/720755/Skeena-Establishes-21A-West-Zone-Continuity-at-Eskay-Creek-with-227-gt-AuEq-over-5000-metres