Nerdy Announces Fourth Quarter and Full Year 2023 Financial Results

Nerdy delivers revenue of

Nerdy beats fourth quarter non-GAAP adjusted EBITDA guidance, and delivers substantial Adjusted EBITDA margin improvements of approximately 2,100 bps in 2023

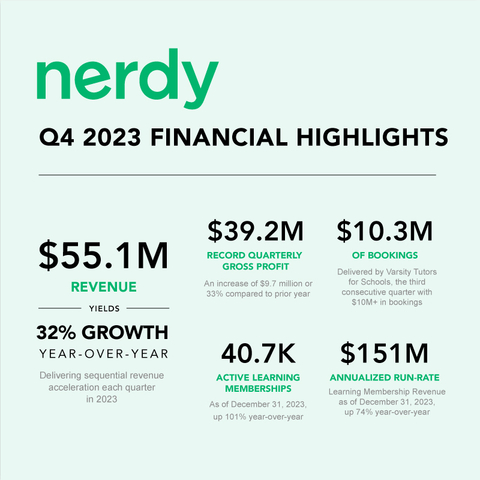

Nerdy Q4 2023 Financial Highlights (Graphic: Business Wire)

“In the fourth quarter, we completed the evolution to access-based subscription products in our Consumer and Institutional businesses, while delivering accelerating revenue growth each quarter throughout the year that culminated in

Please visit the Nerdy investor relations website https://www.nerdy.com/investors to view the Nerdy Q4 Shareholder Letter on the Quarterly Results Page.

Financial and Operating Highlights

-

Revenue Growth Accelerates Each Quarter in 2023 – In the fourth quarter, Nerdy delivered revenue of

$55.1 million 32% year-over-year from$41.8 million

-

Membership Evolution Complete – Nearly

100% of Consumer revenues were from Learning Memberships. Revenue recognized in the fourth quarter from Learning Memberships grew to$43.5 million 32% from Q3 2023) and represented79% of total Company revenue. Active Members of 40.7K as of December 31, 2023 were up101% year-over-year.

-

Institutional Business Delivers Substantial Growth – In the fourth quarter, Institutional revenue of

$11.3 million 160% year-over-year and represented21% of total revenue. Varsity Tutors for Schools executed 42 contracts, yielding$10.3 million $10.0 million

-

Record Quarterly Gross Profit – Gross profit of

$39.2 million 33% year-over-year. Gross margin of71.3% for the three months ended December 31, 2023, was 75 bps higher than gross margin of70.5% during the comparable period in 2022. Gross profit and gross margin increases were primarily driven by growth in our Consumer business as a result of the strong adoption of Learning Memberships, which has led to lifetime value expansion, and higher gross margin.

-

Business Model Changes Deliver Operating Leverage – Net loss was

$9.2 million $15.1 million $2.2 million $(6.8) million $3.0 million $5.5 million

-

Operating Cash Flow and Liquidity – Negative operating cash flow of

$5.0 million $14.5 million $9.5 million $74.8 million

-

First Quarter and Full Year 2024 Outlook – Today, we are introducing guidance for the first quarter and full year.

- Revenue Guidance: For the first quarter of 2024, we expect revenue in a range of$51 $232 $246 million 24% at the midpoint vs. our 2023 revenue of$193 million

- Non-GAAP Adjusted EBITDA Guidance: For the first quarter of 2024, we expect adjusted EBITDA in a range of negative$3 million $5 $15 million

Webcast and Earnings Conference Call

Nerdy’s management will host a conference call and webcast today, February 27, 2024 at 5:00 p.m. Eastern Time. Interested parties in the

About Nerdy Inc.

Nerdy (NYSE: NRDY) is a leading platform for live online learning, with a mission to transform the way people learn through technology. The Company’s purpose-built proprietary platform leverages technology, including AI, to connect learners of all ages to experts, delivering superior value on both sides of the network. Nerdy’s comprehensive learning destination provides learning experiences across thousands of subjects and multiple formats—including Learning Memberships, one-on-one instruction, small group tutoring, large format classes, and adaptive assessments. Nerdy’s flagship business, Varsity Tutors, is one of the nation’s largest platforms for live online tutoring and classes. Its solutions are available directly to students and consumers, as well as through schools and other institutions. Learn more about Nerdy at https://www.nerdy.com.

Forward-looking Statements

The information included herein and in any oral statements made in connection herewith may include “forward looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions, or strategies regarding the future, including our expectations with respect to: the guidance with respect to our financial performance; continued improvements in sales and marketing leverage; the growth of our Institutional business; simplifying our operations model while growing our business; and the sufficiency of our cash to fund future operations. Additionally, any statements that refer to projections, forecasts, or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “approximately,” “believes,” “contemplates,” “continues,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “outlook,” “plans,” “possible,” “potential,” “predicts,” “projects,” “should,” “seeks,” “will,” “would,” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements made herein relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements to reflect events or circumstances after the date of this press release or to reflect new information or the occurrence of unanticipated events, except as required by law. We may not actually achieve the plans, intentions, or expectations disclosed in our forward-looking statements, and you should not place undue reliance on our forward-looking statements.

There are a significant number of factors that could cause actual results to differ materially from statements made herein or in connection herewith, including but not limited to, our limited operating history, which makes it difficult to predict our future financial and operating results; our history of net losses; risks associated with our ability to acquire and retain customers in our Consumer business; risks associated with scaling up our Institutional business, risks associated with our intellectual property, including claims that we infringe on a third-party’s intellectual property rights; risks associated with our classification of some individuals and entities we contract with as independent contractors; risks associated with the liquidity and trading of our securities; risks associated with payments that we may be required to make under the tax receivable agreement; litigation, regulatory and reputational risks arising from the fact that many of our Learners are minors; changes in applicable law or regulation; the possibility of cyber-related incidents and their related impacts on our business and results of operations; the possibility that we may be adversely affected by other economic, business, and/or competitive factors; and risks associated with managing our rapid growth. Our actual results could differ materially from those stated or implied in forward-looking statements due to a number of factors, including but not limited to, risks detailed in our filings with the SEC, including our Annual Report on Form 10-K filed on February 27, 2024, as well as other filings that we may make from time to time with the SEC.

View source version on businesswire.com: https://www.businesswire.com/news/home/20240227127633/en/

Investor Relations

investors@nerdy.com

Source: Nerdy Inc.