Alamos Gold Provides Updated Three-Year Production, Operating and Capital Guidance

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) has provided updated three-year production and operating guidance, incorporating the recently acquired Magino mine. Key highlights include:

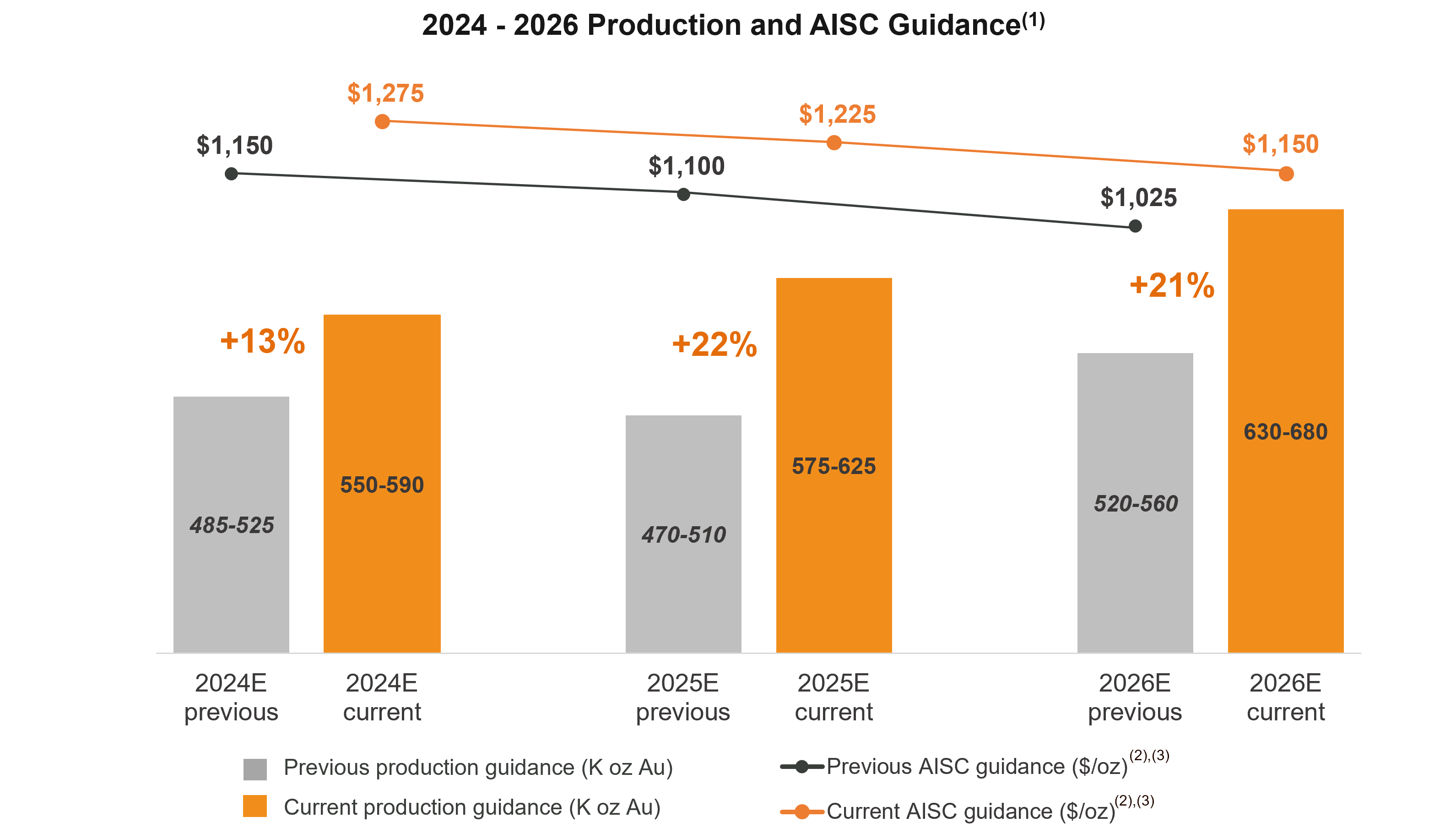

1. Increased production guidance: 13% increase in 2024 to 550,000-590,000 oz, and over 20% increase in 2025 and 2026.

2. Higher AISC guidance: 11% average increase from 2024-2026 due to Magino's inclusion, but still below industry average.

3. Long-term potential: Production capacity of 900,000+ oz per year through PDA development and Lynn Lake growth.

4. Updated capital guidance: Includes Magino, PDA development, and revised Phase 3+ Expansion at Island Gold.

5. Cost reduction: AISC expected to decrease 10% by 2026 compared to 2024, driven by low-cost growth at Island Gold and improving costs at Magino.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) ha fornito aggiornamenti sulla produzione e sulla guida operativa per i prossimi tre anni, includendo la recentemente acquisita miniera di Magino. I punti salienti includono:

1. Aumento della guida sulla produzione: incremento del 13% nel 2024 a 550.000-590.000 once, e oltre il 20% nel 2025 e 2026.

2. Maggiore guida AISC: incremento medio dell'11% dal 2024 al 2026 a causa dell'inclusione del Magino, ma comunque al di sotto della media del settore.

3. Potenziale a lungo termine: capacità produttiva di oltre 900.000 once all'anno attraverso lo sviluppo di PDA e la crescita di Lynn Lake.

4. Guida aggiornate sui capitali: comprende Magino, sviluppo di PDA e la revisione dell'espansione della fase 3+ a Island Gold.

5. Riduzione dei costi: si prevede che l'AISC diminuisca del 10% entro il 2026 rispetto al 2024, grazie alla crescita a basso costo a Island Gold e al miglioramento dei costi a Magino.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) ha proporcionado una actualización sobre la producción y la orientación operativa para los próximos tres años, incorporando la recientemente adquirida mina Magino. Los aspectos destacados incluyen:

1. Aumento de la guía de producción: incremento del 13% en 2024 a 550,000-590,000 onzas, y más del 20% en 2025 y 2026.

2. Mayor guía de AISC: incremento promedio del 11% de 2024 a 2026 debido a la inclusión de Magino, pero aún por debajo del promedio de la industria.

3. Potencial a largo plazo: capacidad de producción de más de 900,000 onzas por año a través del desarrollo de PDA y el crecimiento de Lynn Lake.

4. Guía de capital actualizada: incluye Magino, desarrollo de PDA y revisión de la Fase 3+ de expansión en Island Gold.

5. Reducción de costos: se espera que el AISC disminuya un 10% para 2026 en comparación con 2024, impulsado por el crecimiento de bajo costo en Island Gold y la mejora de los costos en Magino.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI)는 최근 인수한 마지노 광산을 포함하여 향후 3년간의 생산 및 운영 가이드를 업데이트하였습니다. 주요 내용은 다음과 같습니다:

1. 생산 가이드 증가: 2024년에 13% 증가하여 550,000-590,000 온스에 도달하며, 2025년과 2026년에 20% 이상 증가할 것으로 예상됩니다.

2. AISC 가이드 상향: 마지노 포함으로 인해 2024-2026년 평균 11% 증가하나, 여전히 업계 평균 아래입니다.

3. 장기 잠재력: PDA 개발 및 린 레이크 성장을 통해 연간 900,000 온스 이상의 생산 능력을 갖추고 있습니다.

4. 업데이트된 자본 가이드: 마지노, PDA 개발 및 아일랜드 골드의 3단계 이상의 확장 수정이 포함됩니다.

5. 비용 절감: 2024년 대비 2026년까지 AISC가 10% 감소할 것으로 예상되며, 이는 아일랜드 골드의 저비용 성장과 마지노의 비용 개선에 의해 추진됩니다.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) a fourni des mises à jour sur les prévisions de production et d'exploitation pour les trois prochaines années, intégrant la récemment acquise mine de Magino. Les points clés incluent :

1. Augmentation des prévisions de production : augmentation de 13 % en 2024 à 550 000-590 000 onces, et plus de 20 % d'augmentation en 2025 et 2026.

2. Augmentation des prévisions AISC : augmentation moyenne de 11 % de 2024 à 2026 en raison de l'inclusion de Magino, mais toujours en dessous de la moyenne du secteur.

3. Potentiel à long terme : capacité de production de plus de 900 000 onces par an grâce au développement de PDA et à la croissance de Lynn Lake.

4. Mise à jour des prévisions de capital : comprend Magino, développement de PDA et révision de l'expansion de la phase 3+ à Island Gold.

5. Réduction des coûts : l'AISC devrait diminuer de 10 % d'ici 2026 par rapport à 2024, stimulée par une croissance à faible coût à Island Gold et une amélioration des coûts à Magino.

Alamos Gold Inc. (TSX:AGI; NYSE:AGI) hat aktualisierte Produktions- und Betriebsvorgaben für die nächsten drei Jahre veröffentlicht, die die kürzlich erworbene Magino-Mine berücksichtigen. Die Hauptpunkte umfassen:

1. Erhöhung der Produktionsprognose: Anstieg um 13% im Jahr 2024 auf 550.000-590.000 Unzen und über 20% Anstieg in den Jahren 2025 und 2026.

2. Höhere AISC-Prognose: Durchschnittlicher Anstieg um 11% von 2024 bis 2026 aufgrund der Einbeziehung von Magino, jedoch weiterhin unter dem Branchendurchschnitt.

3. Langfristiges Potenzial: Produktionskapazität von über 900.000 Unzen pro Jahr durch die Entwicklung von PDA und das Wachstum des Lynn Lake.

4. Aktualisierte Kapitalprognose: Enthält Magino, PDA-Entwicklung und überarbeitete Phase 3+ Expansion in Island Gold.

5. Kostensenkung: AISC wird bis 2026 voraussichtlich um 10% im Vergleich zu 2024 sinken, angetrieben durch kostengünstiges Wachstum bei Island Gold und verbesserte Kosten bei Magino.

- Production guidance increased 13% in 2024 and over 20% in 2025-2026

- Long-term production potential of 900,000+ oz per year

- AISC expected to decrease 10% by 2026 compared to 2024

- Strong free cash flow generation expected while funding growth initiatives

- Phase 3+ Expansion at Island Gold on track for completion in H1 2026

- AISC guidance increased 11% on average between 2024-2026 due to Magino inclusion

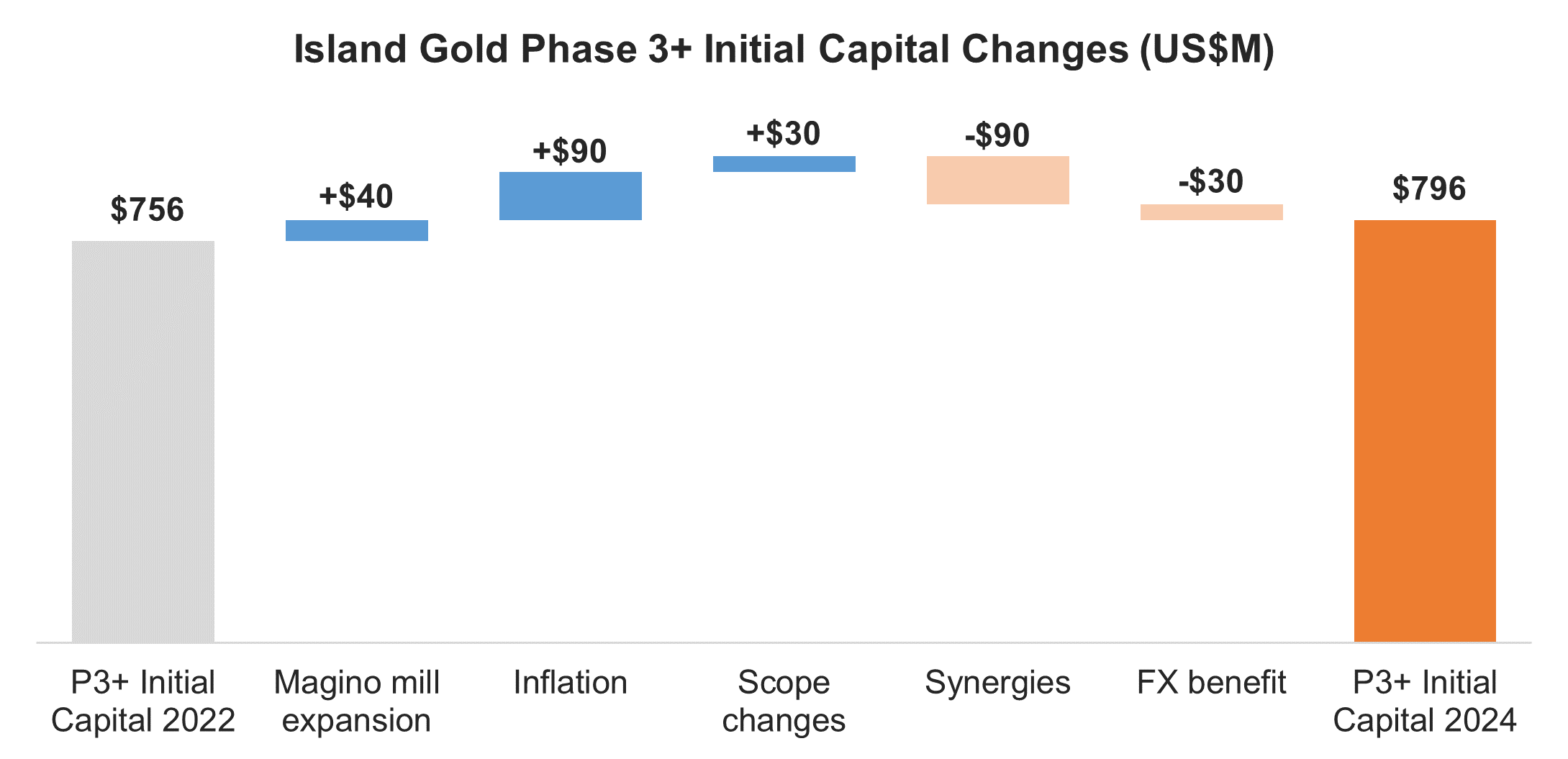

- Phase 3+ Expansion initial capital increased by $40 million (5% increase)

- Increased capital spending in 2025 and 2026 for Magino and PDA development

Insights

This guidance update from Alamos Gold is highly impactful for investors. The company has significantly increased its production outlook, with a

However, the increased production comes at a cost. All-in sustaining costs (AISC) are projected to rise by

The company's capital expenditure guidance has also increased significantly, particularly in 2025-2026, to fund growth projects. While this may impact short-term free cash flow, it sets the stage for long-term production growth and potential cost reductions.

Investors should closely monitor the execution of these growth projects, particularly the integration of Magino and the Phase 3+ Expansion at Island Gold, as they are critical to realizing the projected benefits.

The updated guidance reveals Alamos Gold's ambitious growth strategy, leveraging both organic growth and strategic acquisitions. The Magino acquisition is a game-changer, boosting production significantly while opening up synergies with the existing Island Gold operation.

The company's focus on the high-grade, low-cost Island Gold mine is noteworthy. The Phase 3+ Expansion, despite a

The development of the Puerto Del Aire (PDA) project adds another layer to the growth story, potentially pushing production towards 900,000 ounces annually. However, investors should be aware that executing multiple large projects simultaneously carries operational risks.

Overall, Alamos is positioning itself as a mid-tier gold producer with a strong growth trajectory, which could attract increased investor interest in the sector.

Alamos Gold's updated guidance positions the company favorably in the gold mining sector. The projected

The company's cost profile, while increasing in the short term, remains competitive. The projected AISC of

Investors should note the potential for free cash flow growth post-2026 as major capital projects are completed. This could lead to increased returns to shareholders through dividends or buybacks.

However, the market will likely scrutinize Alamos's ability to execute multiple large projects simultaneously. Any delays or cost overruns could negatively impact investor sentiment. The company's track record of project delivery and operational performance will be important in maintaining market confidence during this growth phase.

Production guidance increased over

All amounts are in United States dollars, unless otherwise stated.

TORONTO, Sept. 12, 2024 (GLOBE NEWSWIRE) -- Alamos Gold Inc. (TSX:AGI; NYSE:AGI) (“Alamos” or the “Company”) today provided updated three-year production and operating guidance incorporating the recently completed acquisition of the Magino mine, as well as increased 2024 production guidance for the Mulatos District. Capital guidance has also been updated to include the development of the Puerto Del Aire (“PDA”) project and a revised initial capital estimate for the Phase 3+ Expansion at Island Gold.

Consolidated 2024 production guidance for existing operations (pre-Magino acquisition) has increased

The inclusion of Magino contributed to a

“The addition of Magino has enhanced our already strong growth profile, and its integration with Island Gold is expected to drive significant synergies and open up longer-term opportunities. Our near-term rate of production has increased by more than

Three Year Guidance Overview: Operating Mines

| 2024 | 2025 | 2026 | ||||

| Current | Previous(1) | Current | Previous(1) | Current | Previous(1) | |

| Gold Production - ex Magino (000 oz) | 510 - 540 | 485 - 525 | 470 - 510 | 470 - 510 | 520 - 560 | 520 - 560 |

| Consolidated Gold Production (000 oz) | 550 - 590 | 485 - 525 | 575 - 625 | 470 - 510 | 630 - 680 | 520 - 560 |

| Total Cash Costs(2) - ex Magino ($/oz) | ||||||

| Consolidated Total Cash Costs ($/oz) | ||||||

| All-in Sustaining Costs(2),(3) - ex Magino ($/oz) | ||||||

| Consolidated All-in Sustaining Costs(2),(3) ($/oz) | ||||||

(1) Previous guidance was issued on January 10, 2024 and related to Young-Davidson, Island Gold and Mulatos District only.

(2) Refer to the “Non-GAAP Measures and Additional GAAP” disclosure at the end of this press release for a description of these measures.

(3) All-in sustaining cost guidance for 2025 and 2026 includes similar assumptions for G&A and stock based compensation as included in 2024.

- 2024 production guidance increased

13% : to between 550,000 and 590,000 ounces. This reflects increased production guidance from the Mulatos District driven by the outperformance of La Yaqui Grande (relative to previous guidance issued in January 2024), and the inclusion of Magino. Production from Magino has been included post completion of the Argonaut Gold acquisition on July 12, 2024, representing slightly less than half a year of production - 2025 and 2026 production guidance increased by over

20% : reflecting the inclusion of Magino for full years and the operation at planned capacity. This includes a22% increase in 2025 production guidance, and21% increase in 2026 guidance to between 630,000 and 680,000 ounces. This represents30% production growth relative to the mid-point of previous 2024 guidance issued at the start of the year - Longer-term production potential of 900,000+ oz per year: through the development of PDA, with initial production expected mid-2027, and growth from Lynn Lake with first production as early as the second half of 2027. An evaluation of a longer-term expansion of the Magino mill to 15,000 to 20,000 tonnes per day (“tpd”) is also underway which could support additional growth bringing production closer to one million ounces per year

- AISC guidance increased

11% on average between 2024 and 2026: reflecting the inclusion of relatively higher cost Magino production. Costs remain well below the industry average with steady improvements expected through 2026 driven by low-cost production growth - Declining cost profile with AISC expected to decrease

10% by 2026 compared to 2024: AISC is expected to decrease to between$1,100 and$1,200 per ounce in 2026 driven by low-cost growth at Island Gold and improving costs at Magino. Beyond 2026, AISC is expected to decrease below$1,100 per ounce, reflecting additional low-cost growth from Island Gold and Lynn Lake

Three Year Guidance Overview: Capital

| 2024 | 2025 | 2026 | ||||

| ($ millions) | Current | Previous(2) | Current | Previous(2) | Current | Previous(2) |

| Sustaining & Growth Capital (operating mines, ex. Exploration & Lynn Lake)(1) | ||||||

| Addition of PDA | - | |||||

| Addition of Magino | ||||||

| Changes to Phase 3+ Expansion | ( | |||||

| Total Capital (operating mines, ex. Exploration & Lynn Lake)(1) | ||||||

(1) Refer to the "Non-GAAP Measures and Additional GAAP" disclosure at the end of this press release for a description of these measures.

(2) Previous guidance was issued on January 10, 2024 and related to Young-Davidson, Island Gold and Mulatos District only.

- Capital spending increased in 2025 and 2026 reflecting inclusion of Magino, PDA development, and updated Phase 3+ Expansion capital:

- The main driver of the increase in capital spending over the next three years is the inclusion of growth and sustaining capital for the newly acquired Magino operation, as well as growth capital for the development of PDA. Both are in support of high-return, lower-risk organic growth initiatives

- 2024 capital guidance range was increased slightly to between

$330 and$375 million (excluding capitalized exploration), reflecting the inclusion of Magino from July 2024 onward, largely offset by a reduction at Island Gold with the mill expansion and tailings lifts no longer required with the Magino acquisition - 2025 and 2026 capital guidance was revised to include:

- initial capital for the high-return, PDA project as per the recently announced development plan (see September 4, 2024 press release)

- the inclusion of Magino growth and sustaining capital for the normal course operation, as well as for the completion of the mill optimization and other projects that were deferred by the previous operator

- additional capital for the completion of the Phase 3+ Expansion

- Phase 3+ Expansion initial capital has been increased by approximately

$40 million with expected completion on track for the first half of 2026. This represents a5% increase from the initial capital estimate of$756 million provided in the first half of 2022. Updated capital is now expected to total$796 million , with$415 million remaining to be spent as of June 30, 2024. The increase was driven by ongoing inflationary pressures since 2022, and scope changes to the project, partly offset by synergies from the Magino acquisition and the weaker Canadian dollar

- Strong ongoing free cash flow while funding high-return growth initiatives: the Company generated

$131 million in free cash flow in the first half of 2024 and expects to continue generating strong free cash flow at current gold prices while funding the Phase 3+ Expansion at Island Gold, and development of PDA. The completion of Phase 3+ Expansion in 2026 and PDA development in 2027 are expected to drive growing free cash flow generation through higher production, lower costs, and lower capital spending

Guidance statements in this release are forward-looking information. See the Assumptions section of this release along with the cautionary note at the end of this release.

Upcoming catalysts

- Burnt Timber and Linkwood study (satellite deposits to Lynn Lake): Q4 2024

- 2024 year-end Mineral Reserve and Resource update: February 2025

- Island Gold District Life of Mine Plan: mid-2025

- Island Gold District Expansion Study: Q4 2025

- Island Gold District, Mulatos District & Young-Davidson exploration updates: ongoing

2024 Guidance

| 2024 Guidance | |||||||||||||

| Young- Davidson | Island Gold | Magino Mine(1) | Mulatos District | Lynn Lake | Total Current | Total Previous (2) | |||||||

| Gold production (000 oz) | 180 - 190 | 145 - 155 | 40 - 50 | 185 - 195 | 550 - 590 | 485 - 525 | |||||||

| Total cash costs(3) ($/oz) | - | ||||||||||||

| All-in sustaining costs(3) ($/oz) | |||||||||||||

| Mine-site all-in sustaining costs(3)(4) ($/oz) | - | ||||||||||||

| Capital expenditures ($ millions) | |||||||||||||

| Sustaining capital(3) | - | ||||||||||||

| Growth capital(3) | - | - | |||||||||||

| Total Sustaining and Growth Capital(3) - producing mines ($ millions) | - | ||||||||||||

| Growth capital(3) – development projects ($ millions) | $25 | $25 | |||||||||||

| Capitalized exploration(3) ($ millions) | $43 | $41 | |||||||||||

| Total capital expenditures and capitalized exploration(3) ($ millions) | $34 | ||||||||||||

(1) The guidance for the Magino Mine is for Alamos’ ownership period from July 12, 2024 to December 31, 2024.

(2) Previous guidance was issued on January 10, 2024 and related to Young-Davidson, Island Gold and Mulatos District only.

(3) Refer to the "Non-GAAP Measures and Additional GAAP" disclosure at the end of this press release for a description of these measures.

(4) For the purposes of calculating mine-site all-in sustaining costs at individual mine sites, the Company does not include an allocation of corporate and administrative and share based compensation expenses to the mine sites.

Gold production in 2024 is expected to range between 550,000 and 590,000 ounces, a

With the closing of the Argonaut Gold acquisition on July 12, 2024, less than half a year of production from Magino is being incorporated into 2024 estimates. Magino is expected to produce 40,000 to 50,000 ounces in the second half of 2024. As previously outlined, the third quarter is expected to be impacted by downtime to implement various improvements to the crushing and conveying circuit. Combined with the partial reporting period, third quarter Magino production is expected to be slightly less than the second quarter. Production rates at Magino are expected to improve in the fourth quarter and into 2025 reflecting various improvements to the Magino mill that are being implemented in the third quarter.

Reflecting the strong outperformance of La Yaqui Grande during the first half of the year, Mulatos District production guidance has been increased by

AISC guidance has increased

Young-Davidson’s AISC guidance was increased by

Capital guidance for 2024 has increased by

Capital spending at Magino during the second half of 2024 will be comprised of capitalized stripping and equipment leases, as well as ongoing work on the mill optimization.

2024 – 2026 Guidance: Operating Mines

| 2024 | 2025 | 2026 | ||||

| Current | Previous(1) | Current | Previous(1) | Current | Previous(1) | |

| Gold Production (000 oz) | ||||||

| Young-Davidson | 180 - 190 | 180 - 195 | 180 - 195 | 180 - 195 | 180 - 195 | 180 - 195 |

| Island Gold District(2) | 145 - 155 | 145 - 160 | 275 - 300 | 170 - 185(1) | 330 - 355 | 220 - 235(1) |

| Magino Mine(2) | 40 - 50 | n/a | n/a | n/a | ||

| Mulatos District | 185 - 195 | 160 - 170 | 120 - 130 | 120 - 130 | 120 - 130 | 120 - 130 |

| Total Gold Production (000 oz) | 550 - 590 | 485 - 525 | 575 - 625 | 470 - 510 | 630 - 680 | 520 - 560 |

| Total Cash Costs(3) ($/oz) | ||||||

| All-in Sustaining Costs(3),(4) ($/oz) | ||||||

| Sustaining capital(3),(5) ($ millions) | ||||||

| Growth capital(3),(5) ($ millions) | ||||||

| Total sustaining & growth capital(3),(5) (Operating mines; ex. Exploration) ($ millions) | ||||||

(1) Previous guidance was issued on January 10, 2024 and related to Young-Davidson, Island Gold and Mulatos District only.

(2) 2024 production and cost estimates are for the Island Gold Mine, for 2025 and 2026 the Island Gold District includes both the Island Gold and Magino mines.

(3) Refer to the “Non-GAAP Measures and Additional GAAP” disclosure at the end of this press release for a description of these measures.

(4) All-in sustaining cost guidance for 2025 and 2026 includes similar assumptions for G&A and stock based compensation as included in 2024.

(5) Sustaining and growth capital guidance is for producing mines and PDA development, but excludes capital for Lynn Lake and capitalized exploration.

Production guidance for 2025 has increased

At that point, the Island Gold mill will be shut down and Island Gold ore will be processed through the Magino mill at significantly lower processing costs. An expansion of the mill to 12,400 tpd is expected to be completed in 2026 and coincide with the completion of the Phase 3+ Expansion. This is expected to accommodate 10,000 tpd of ore from Magino and 2,400 tpd from Island Gold.

Production guidance for 2026 has increased

This growth is expected to continue into 2027 driven by a full year of production following the completion of the Phase 3+ Expansion, as well as initial production from PDA in the second half of the year. The Lynn Lake project represents further growth potential with initial production as early as the latter part of 2027.

AISC guidance for 2025 and 2026 has increased

Capital spending in 2025 and 2026 was revised higher from the previous guidance to reflect:

- capital for the construction of the high-return PDA project, as outlined in the development plan announced on September 4, 2024

- the inclusion of Magino and associated capital for tailings, equipment leases, normal-course maintenance, as well as projects that were deferred by the previous operator, including the construction of a truck shop and fish habitat

- capital to connect Magino to the electric grid by 2026. This is expected to drive significant operating cost savings with power to Magino currently generated by a Compressed Natural Gas (“CNG”) plant

- a

5% increase in capital to complete the Phase 3+ Expansion reflecting ongoing inflation since the first half of 2022, and scope changes. This was largely offset by synergies through the integration of Magino and Island Gold, as well as the weaker Canadian dollar

(1) Production and AISC are based on mid-point of guidance; previous guidance was issued on January 10, 2024 and related to Young-Davidson, Island Gold and Mulatos District only.

(2) Refer to the “Non-GAAP Measures and Additional GAAP” disclosure at the end of this press release for a description of these measures.

(3) Total consolidated all-in sustaining costs include corporate and administrative and share based compensation expenses.

Updated Phase 3+ Expansion Capital

The Phase 3+ Expansion initial capital estimate has been updated to reflect inflation and scope changes since the Phase 3+ Expansion Study was completed in the first half of 2022, as well as synergies from the acquisition of Magino.

Initial capital for the Phase 3+ Expansion has been increased by approximately

The increase was driven by ongoing inflationary pressures since 2022, and scope changes to the project, partly offset by synergies from the Magino acquisition, and the weaker Canadian dollar. The key changes within the updated capital estimate are as follows:

- Magino mill expansion:

$40 million increase for the expansion of the Magino mill to 12,400 tpd by 2026. This will accommodate ore from both Magino and the increased production from Island Gold following the completion of the Phase 3+ Expansion - Inflation:

$90 million increase in capital driven by more than two years of labour and material inflation representing a12% increase on the total capital spend between 2022 and 2026. Since the Phase 3+ Expansion Study was completed in the first half of 2022, company-wide inflation has averaged5% per year - Scope changes:

$30 million increase reflecting the following changes to the project:- Relocation of crushing facility from surface to underground. This will further optimize the flow of ore handling from the underground to the mill, and reduce required maintenance of the hoisting plant

- Construction of a larger and modern administrative building at the shaft site, replacing the existing buildings located near the soon-to-be decommissioned Island Gold mill

- Construction of a new haul road from the underground portal at Island Gold to the Magino mill, allowing ore to be transported to the larger Magino mill for processing starting early 2025

- Synergies:

$90 million decrease in capital with the mill expansion at Island Gold no longer required. Ore from Island Gold is expected to be processed through the significantly larger Magino mill starting in 2025 - Weaker Canadian dollar:

$30 million decrease in capital based on updated USD/CAD assumption of$0.75 :1 to reflect more current exchanges rates. The initial capital estimate prepared in 2022 was based on a USD/CAD exchange rate of$0.78 :1

In addition to the initial capital savings to be realized through the cancellation of the Island Gold mill expansion, the Company expects to benefit from additional life of mine capital savings with no further expansions of the Island Gold tailings facility required. The operation is also expected to realize approximately

As of June 30, 2024,

Assumptions

The 2024 to 2026 production forecast, operating cost and capital estimates remain based on a USD/CAD foreign exchange rate of

Qualified Persons

Chris Bostwick, Alamos’ Senior Vice President, Technical Services, who is a qualified person within the meaning of National Instrument 43-101 Standards of Disclosure for Mineral Projects, has reviewed and approved the scientific and technical information contained in this press release.

About Alamos

Alamos is a Canadian-based intermediate gold producer with diversified production from three operations in North America. This includes the Young-Davidson mine and Island Gold District in northern Ontario, Canada, and the Mulatos District in Sonora State, Mexico. Additionally, the Company has a strong portfolio of growth projects, including the Phase 3+ Expansion at Island Gold, and the Lynn Lake project in Manitoba, Canada. Alamos employs more than 2,400 people and is committed to the highest standards of sustainable development. The Company’s shares are traded on the TSX and NYSE under the symbol “AGI”.

FOR FURTHER INFORMATION, PLEASE CONTACT:

| Scott K. Parsons | |

| Senior Vice President, Corporate Development & Investor Relations | |

| (416) 368-9932 x 5439 | |

| Khalid Elhaj | |

| Vice President, Business Development & Investor Relations | |

| (416) 368-9932 x 5427 | |

| ir@alamosgold.com | |

The TSX and NYSE have not reviewed and do not accept responsibility for the adequacy or accuracy of this release.

Cautionary Note

This press release contains or incorporates by reference “forward-looking statements” and “forward-looking information” as defined under applicable Canadian and U.S. securities laws. All statements, other than statements of historical fact, which address events, results, outcomes or developments that the Company expects to occur are, or may be deemed to be, forward-looking statements and are generally, but not always, identified by the use of forward-looking terminology such as "expect", “assume”, “estimate”, “potential”, “outlook”, “on track”, “continue”, “ongoing”, "will", “believe”, “anticipate”, "intend", "estimate", "forecast", "budget", “target”, “plan” or variations of such words and phrases and similar expressions or statements that certain actions, events or results “may", “could”, “would”, "might" or "will" be taken, occur or be achieved or the negative connotation of such terms. Forward-looking statements contained in this press release are based on expectations, estimates and projections as of the date of this press release.

Forward-looking statements in this press release include, but may not be limited to, information, expectations and guidance as to strategy, plans, future financial and operating performance, such as expectations and guidance regarding: costs (including cash costs, AISC, mine-site AISC, capital expenditures , exploration spending), cost structure and anticipated declining cost profile; budgets; growth capital; sustaining capital; cash flow; foreign exchange rates; gold and other metal price assumptions; anticipated gold production, production rates, timing of production, production potential and growth; returns to stakeholders; the mine plan for and expected results from the Puerto Del Aire (PDA) project as well as the Phase 3+ expansion at Island Gold and timing of its progress and completion; feasibility of, development of, and mine plan for, the Lynn Lake project and potential growth in production resulting from the Lynn Lake project; continued improvements at the Magino operation; expected synergies and long-term opportunities from the integration of Magino with Island Gold; future expansions of the Island Gold District; upcoming catalysts, including expected timing, such as the Burnt Timber and Linkwood study, 2024 Mineral Reserve and Resource update, Island Gold District Life of Mine Plan and expansion study as well as exploration updates; mining, milling and processing and rates; mined and processed gold grades and weights; mine life; Mineral Reserve life; planned exploration, drilling targets, exploration potential and results; as well as any other statements related to the Company's production forecasts and plans, expected sustaining costs, expected improvements in cash flows and margins, expectations of changes in capital expenditures, expansion plans, project timelines, and expected sustainable productivity increases, expected increases in mining activities and corresponding cost efficiencies, cost estimates, sufficiency of working capital for future commitments, Mineral Reserve and Mineral Resource estimates, and other statements or information that express management's expectations or estimates of future performance, operational, geological or financial results.

The Company cautions that forward-looking statements are necessarily based upon several factors and assumptions that, while considered reasonable by management at the time of making such statements, are inherently subject to significant business, economic, technical, legal, political and competitive uncertainties and contingencies. Known and unknown factors could cause actual results to differ materially from those projected in the forward-looking statements, and undue reliance should not be placed on such statements and information.

Such factors and assumptions underlying the forward-looking statements in this press release, include (without limitation): changes to current estimates of Mineral Reserves and Resources; changes to production estimates (which assume accuracy of projected ore grade, mining rates, recovery timing and recovery rate estimates and may be impacted by unscheduled maintenance, weather issues, labour and contractor availability and other operating or technical difficulties); operations may be exposed to new illnesses, diseases, epidemics and pandemics (and any related regulatory or government responses) and associated impact on the broader market and the trading price of the Company’s shares; provincial, state and federal orders or mandates (including with respect to mining operations generally or auxiliary businesses or services required for the Company’s operations) in Canada, Mexico, the United States and Türkiye, all of which may affect many aspects of the Company’s operations including the ability to transport personnel to and from site, contractor and supply availability and the ability to sell or deliver gold doré bars; fluctuations in the price of gold or certain other commodities such as, diesel fuel, natural gas and electricity; changes in foreign exchange rates (particularly the Canadian dollar, U.S. dollar, Mexican peso and Turkish Lira); the impact of inflation; changes in the Company’s credit rating; any decision to declare a dividend; employee and community relations; labour and contractor availability (and being able to secure the same on favourable terms); the impact of litigation and administrative proceedings (including but not limited to the investment treaty claim announced on April 20, 2021 against the Republic of Türkiye by the Company’s wholly-owned Netherlands subsidiaries, Alamos Gold Holdings Coöperatief U.A. and Alamos Gold Holdings B.V., the application for judicial review of the positive Decision Statement issued by the Ministry of Environment and Climate Change Canada commenced by the Mathias Colomb Cree Nation (MCCN) in respect of the Lynn Lake project and the MCCN’s corresponding internal appeal of the Environment Act Licences issued by the Province of Manitoba for the project) and any resulting court, arbitral and/or administrative decisions; disruptions affecting operations; availability of and increased costs associated with mining inputs and labour; risks associated with the startup of new mines; permitting, construction or other delays in or with the Phase 3+ Expansion at Island Gold, development of the PDA project, construction decisions and any development of the Lynn Lake project, and/or the development or updating of mine plans; changes with respect to the intended method of accessing, mining and processing ore from Lynn Lake and the deposit at PDA; exploration opportunities and potential in the Mulatos District, at Young Davidson, Island Gold and/or Magino mine not coming to fruition; inherent risks and hazards associated with mining and mineral processing including environmental hazards, industrial accidents, unusual or unexpected formations, pressures and cave-ins; the risk that the Company’s mines may not perform as planned; uncertainty with the Company's ability to secure additional capital to execute its business plans; the speculative nature of mineral exploration and development, including the risks of obtaining and maintaining necessary licenses, permits and authorizations, contests over title to properties; expropriation or nationalization of property; political or economic developments in Canada, Mexico, the United States, Türkiye and other jurisdictions in which the Company may carry on business in the future; increased costs and risks related to the potential impact of climate change; changes in national and local government legislation, controls or regulations (including tax and employment legislation) in jurisdictions in which the Company does or may carry on business in the future; the costs and timing of construction and development of new deposits; risk of loss due to sabotage, protests and other civil disturbances; disruptions in the maintenance or provision of required infrastructure and information technology systems, the impact of global liquidity and credit availability and the values of assets and liabilities based on projected future cash flows; risks arising from holding derivative instruments; and business opportunities that may be pursued by the Company.

For a more detailed discussion of such risks and other factors that may affect the Company's ability to achieve the expectations set forth in the forward-looking statements contained in this press release, see the Company’s latest 40-F/Annual Information Form and Management’s Discussion and Analysis, each under the heading “Risk Factors” available on the SEDAR+ website at www.sedarplus.ca or on EDGAR at www.sec.gov. The foregoing should be reviewed in conjunction with the information and risk factors and assumptions found in this press release.

The Company disclaims any intention or obligation to update or revise any forward-looking statements whether as a result of new information, future events or otherwise, except as required by applicable law.

Cautionary non-GAAP Measures and Additional GAAP Measures

Note that for purposes of this section, GAAP refers to IFRS. The Company believes that investors use certain non-GAAP and additional GAAP measures as indicators to assess gold mining companies. They are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared with GAAP.

“Cash flow from operating activities before changes in non-cash working capital” is a non-GAAP performance measure that could provide an indication of the Company’s ability to generate cash flows from operations and is calculated by adding back the change in non-cash working capital to “cash provided by (used in) operating activities” as presented on the Company’s consolidated statements of cash flows. “Cash flow per share” is calculated by dividing “cash flow from operations before changes in working capital” by the weighted average number of shares outstanding for the period. “Free cash flow” is a non-GAAP performance measure that is calculated as cash flows from operations net of cash flows invested in mineral property, plant and equipment and exploration and evaluation assets as presented on the Company’s consolidated statements of cash flows and that would provide an indication of the Company’s ability to generate cash flows from its mineral projects. “Mine site free cash flow” is a non-GAAP measure which includes cash flow from operating activities at, less capital expenditures at each mine site. “Return on equity” is defined as earnings from continuing operations divided by the average total equity for the current and previous year. “Mining cost per tonne of ore” and “cost per tonne of ore” are non-GAAP performance measures that could provide an indication of the mining and processing efficiency and effectiveness of the mine. These measures are calculated by dividing the relevant mining and processing costs and total costs by the tonnes of ore processed in the period. “Cost per tonne of ore” is usually affected by operating efficiencies and waste-to-ore ratios in the period. “Sustaining capital” are expenditures that do not increase annual gold ounce production at a mine site and excludes all expenditures at the Company’s development projects. “Growth capital” are expenditures primarily incurred at development projects and costs related to major projects at existing operations, where these projects will materially benefit the mine site. “Capitalized exploration” are expenditures that meet the IFRS definition for capitalization, and are incurred to further expand the known Mineral Reserve and Resource at existing operations or development projects. “Total capital expenditures per ounce produced” is a non-GAAP term used to assess the level of capital intensity of a project and is calculated by taking the total growth and sustaining capital of a project divided by ounces produced life of mine. “Total cash costs per ounce”, “all-in sustaining costs per ounce”, “mine-site all-in sustaining costs”, and “all-in costs per ounce” as used in this analysis are non-GAAP terms typically used by gold mining companies to assess the level of gross margin available to the Company by subtracting these costs from the unit price realized during the period. These non-GAAP terms are also used to assess the ability of a mining company to generate cash flow from operations. There may be some variation in the method of computation of these metrics as determined by the Company compared with other mining companies. In this context, “total cash costs” reflects mining and processing costs allocated from in-process and doré inventory and associated royalties with ounces of gold sold in the period. Total cash costs per ounce are exclusive of exploration costs. “All-in sustaining costs per ounce” include total cash costs, exploration, corporate and administrative, share based compensation and sustaining capital costs. “Mine-site all-in sustaining costs” include total cash costs, exploration, and sustaining capital costs for the mine-site, but exclude an allocation of corporate and administrative and share based compensation. “Adjusted net earnings” and “adjusted earnings per share” are non-GAAP financial measures with no standard meaning under IFRS. “Adjusted net earnings” excludes the following from net earnings: foreign exchange gain (loss), items included in other loss, certain non-reoccurring items and foreign exchange gain (loss) recorded in deferred tax expense. “Adjusted earnings per share” is calculated by dividing “adjusted net earnings” by the weighted average number of shares outstanding for the period. Additional GAAP measures that are presented on the face of the Company’s consolidated statements of comprehensive income and are not meant to be a substitute for other subtotals or totals presented in accordance with IFRS, but rather should be evaluated in conjunction with such IFRS measures. This includes “Earnings from operations”, which is intended to provide an indication of the Company’s operating performance, and represents the amount of earnings before net finance income/expense, foreign exchange gain/loss, other income/loss, and income tax expense. Non-GAAP and additional GAAP measures do not have a standardized meaning prescribed under IFRS and therefore may not be comparable to similar measures presented by other companies. A reconciliation of historical non-GAAP and additional GAAP measures are available in the Company’s latest Management’s Discussion and Analysis available online on the SEDAR+ website at www.sedarplus.ca or on EDGAR at www.sec.gov and at www.alamosgold.com.

Graphs accompanying this announcement are available at:

https://www.globenewswire.com/NewsRoom/AttachmentNg/42606370-bfae-4488-a3e0-023ad84da0d6

https://www.globenewswire.com/NewsRoom/AttachmentNg/d3cba6ad-8b75-47b8-b2e6-9dafe0a06ea8